Advertisement

- United States

- /

- Life Sciences

- /

- NasdaqGS:TECH

Bio Techne (TECH) Margin Compression To 6.7% TTM Tests Bullish Growth Narratives

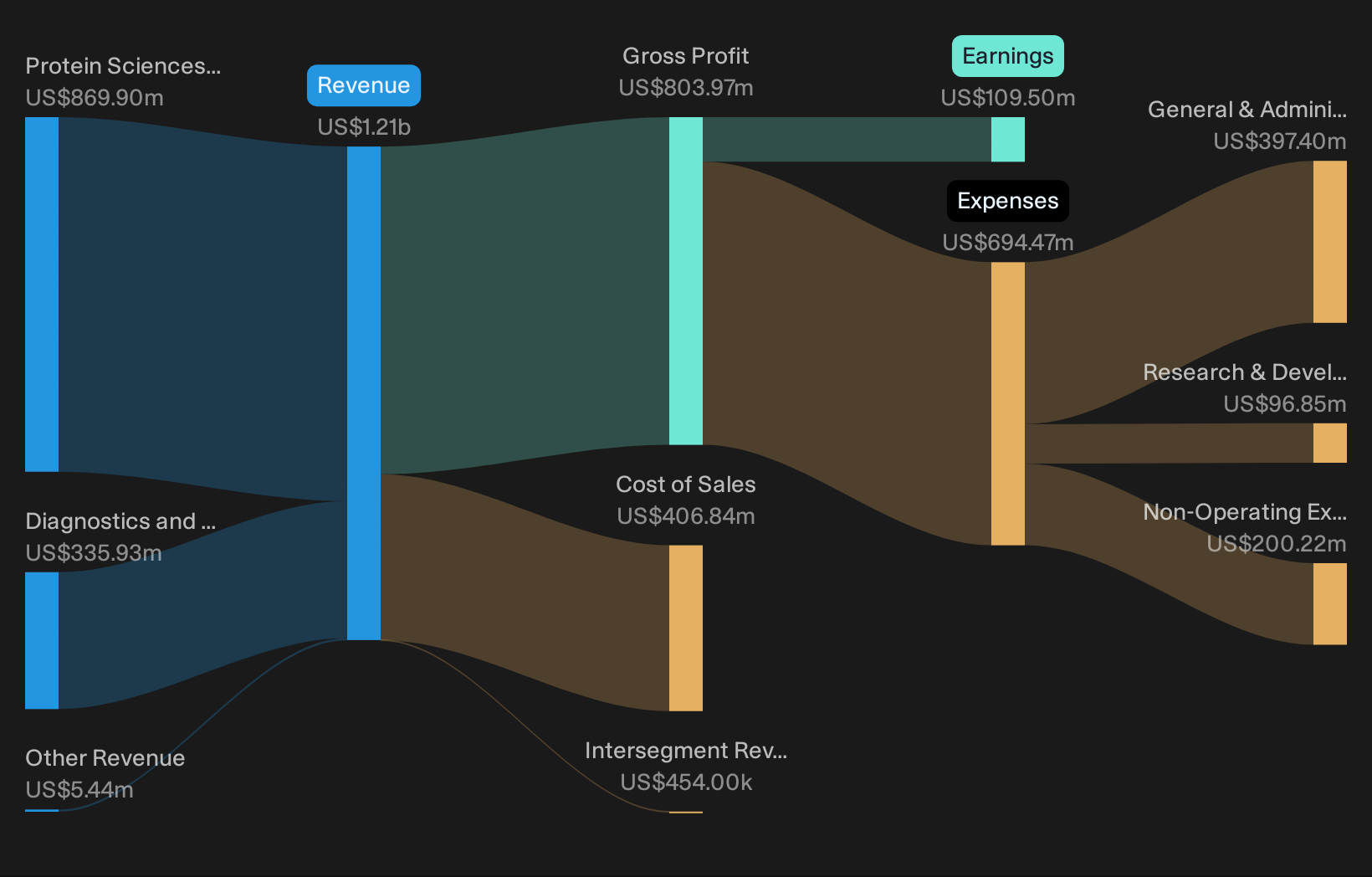

Bio-Techne (TECH) has reported Q2 2026 revenue of US$295.9 million with basic EPS of US$0.24, alongside trailing twelve month revenue of about US$1.2 billion and EPS of US$0.52, setting up a mixed picture for growth and profitability. The company has seen quarterly revenue move between US$289.5 million and US$317.0 million over the past six reported periods, while basic EPS has ranged from a loss of US$0.11 to a recent run rate just above US$0.24. This matters for investors focused on how consistently those earnings convert into margins. With TTM net income of US$81.1 million on that US$1.2 billion revenue base, the story now is less about top line scale and more about how much profit Bio-Techne can keep from each dollar of sales.

See our full analysis for Bio-Techne.With the headline numbers on the table, the next step is to set these results against the widely followed narratives around Bio-Techne's growth outlook, profitability track record, and risk profile to see which views hold up and which start to look stretched.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margins Weaken as TTM Net Income Slows

- On a trailing 12 month view, Bio Techne earned US$81.1 million of net income on US$1.2b of revenue, which equates to a 6.7% net margin compared with 13.2% a year earlier and includes a one off loss of US$148.3 million.

- What stands out for a more cautious, bearish take is that trailing earnings have declined by about 11.5% per year over the past five years while the latest four quarters together produced a 6.7% margin, a clear step down from 13.2%. That suggests recent profitability has been under pressure even before considering the US$148.3 million one off charge.

- Bears often focus on that combination of a large one time loss and lower margin as a sign that current profit levels may be less resilient than they look from a single quarter like Q2 2026, where net income was US$38.0 million on US$295.9 million of revenue.

- The fact that five year earnings have trended down while reported net income for the last 12 months sits at US$81.1 million gives them more data to question how quickly or reliably profitability can rebuild from here.

Quarterly Profit Holds Steady Around US$38 Million

- Looking just at the last two quarters, net income was US$38.0 million in Q2 2026 on US$295.9 million of revenue and US$38.2 million in Q1 2026 on US$286.6 million of revenue, with basic EPS at roughly US$0.24 in both periods after a Q4 2025 loss of US$17.7 million on US$317.0 million of revenue.

- Supporters of a more bullish view point out that this recent stretch of roughly US$38 million of net income in back to back quarters shows a return to positive profitability after that Q4 2025 loss. Yet the trailing 12 month margin of 6.7% and the inclusion of a US$148.3 million one off loss still temper how strong that rebound looks when you zoom out to the full year.

- On the one hand, Q1 and Q2 2026 net income of US$38.2 million and US$38.0 million compare quite differently to the Q4 2025 loss of US$17.7 million, which suggests the business has not stayed in loss making territory.

- On the other hand, when you combine those quarters into the US$81.1 million of trailing net income on US$1.2b of revenue, the picture is of a low single digit US$ per share TTM EPS of US$0.52, which is far from the stronger trailing margins recorded a year earlier.

Rich 126.6x P/E Versus 6.7% Margin

- The stock trades on a P/E of 126.6x based on trailing earnings, compared with 31.4x for peers and 36.6x for the wider North American Life Sciences industry, while the same trailing period shows a 6.7% net margin on US$1.2b of revenue and TTM EPS of US$0.52 at a share price of US$65.86.

- What is interesting for investors who see a more optimistic path is that earnings are presented as forecast to grow about 23.2% per year and the stock is shown as trading roughly 11.4% below a DCF fair value of US$74.32. Those positives need to be weighed against a P/E that is roughly 4x the 31.4x peer level and a net margin that has moved from 13.2% to 6.7%.

- Supportive investors may look at the gap between the current US$65.86 price and the US$74.32 DCF fair value as evidence that the market price is not fully reflecting the modelled growth path, especially with that 23.2% earnings growth figure in the data.

- Others will focus on the fact that paying 126.6x earnings for a business that currently earns US$81.1 million on US$1.2b of revenue Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Bio-Techne's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Bio-Techne's compressed 6.7% trailing net margin, one off US$148.3 million loss and rich 126.6x P/E all highlight pressure on current profitability and value.

If that mix of a high earnings multiple and softer margins makes you hesitate, compare it with our 55 high quality undervalued stocks that flag companies where price and fundamentals line up more tightly.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bio-Techne might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TECH

Bio-Techne

Develops, manufactures, and sells life science reagents, instruments, and services for the research, diagnostics, and bioprocessing markets worldwide.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

75 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

66 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Abitibi Metals ·

Abitibi Metals’ High-Grade B26 Polymetallic Deposit Trading at a Fraction of Peers, 96% Undervalued?

Fair Value:CA$1.2950.4% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

EV

everyseed on Zylox-Tonbridge Medical Technology ·

Zylox-Tonbridge: Early Signs of an Emerging Global Vascular Intervention Platform

Fair Value:HK$30.8539.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

Anthony_Lee on Geohan Corporation Berhad ·

Geohan's Growth Outlook Brightens on Expanding Order Book and Easing Cost Pressures

Fair Value:RM 0.7460.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

75 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative