Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Tarsus Pharmaceuticals, Inc. (NASDAQ:TARS) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Tarsus Pharmaceuticals

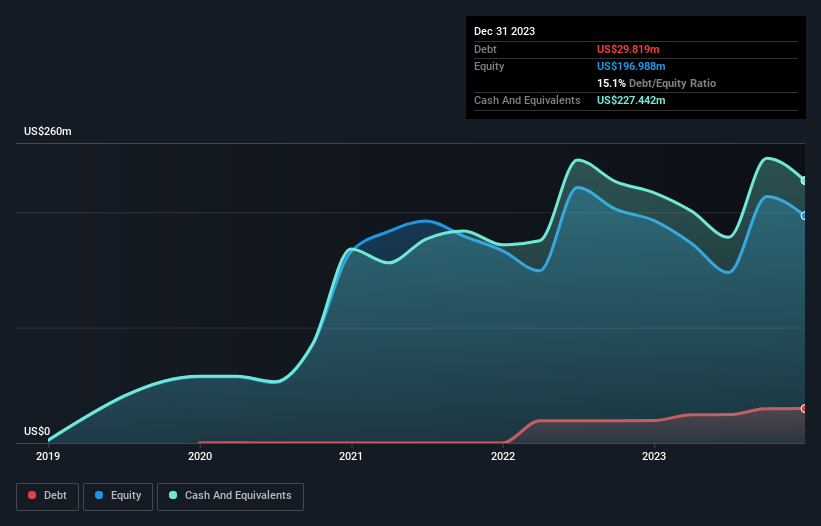

What Is Tarsus Pharmaceuticals's Net Debt?

As you can see below, at the end of December 2023, Tarsus Pharmaceuticals had US$29.8m of debt, up from US$19.4m a year ago. Click the image for more detail. However, its balance sheet shows it holds US$227.4m in cash, so it actually has US$197.6m net cash.

A Look At Tarsus Pharmaceuticals' Liabilities

According to the last reported balance sheet, Tarsus Pharmaceuticals had liabilities of US$36.9m due within 12 months, and liabilities of US$31.6m due beyond 12 months. On the other hand, it had cash of US$227.4m and US$17.7m worth of receivables due within a year. So it actually has US$176.7m more liquid assets than total liabilities.

This excess liquidity suggests that Tarsus Pharmaceuticals is taking a careful approach to debt. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Succinctly put, Tarsus Pharmaceuticals boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Tarsus Pharmaceuticals can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Tarsus Pharmaceuticals made a loss at the EBIT level, and saw its revenue drop to US$17m, which is a fall of 32%. To be frank that doesn't bode well.

So How Risky Is Tarsus Pharmaceuticals?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year Tarsus Pharmaceuticals had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of US$95m and booked a US$136m accounting loss. But at least it has US$197.6m on the balance sheet to spend on growth, near-term. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example - Tarsus Pharmaceuticals has 1 warning sign we think you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Tarsus Pharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:TARS

Tarsus Pharmaceuticals

A commercial stage biopharmaceutical company, focuses on the development and commercialization of therapeutic candidates for eye care in the United States.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.8% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|43.5% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|61.4% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.9% undervalued

UN

Community Contributor