- United States

- /

- Biotech

- /

- NasdaqCM:SLS

Is SELLAS Life Sciences Group (NASDAQ:SLS) In A Good Position To Invest In Growth?

There's no doubt that money can be made by owning shares of unprofitable businesses. Indeed, SELLAS Life Sciences Group (NASDAQ:SLS) stock is up 116% in the last year, providing strong gains for shareholders. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

In light of its strong share price run, we think now is a good time to investigate how risky SELLAS Life Sciences Group's cash burn is. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

Check out our latest analysis for SELLAS Life Sciences Group

How Long Is SELLAS Life Sciences Group's Cash Runway?

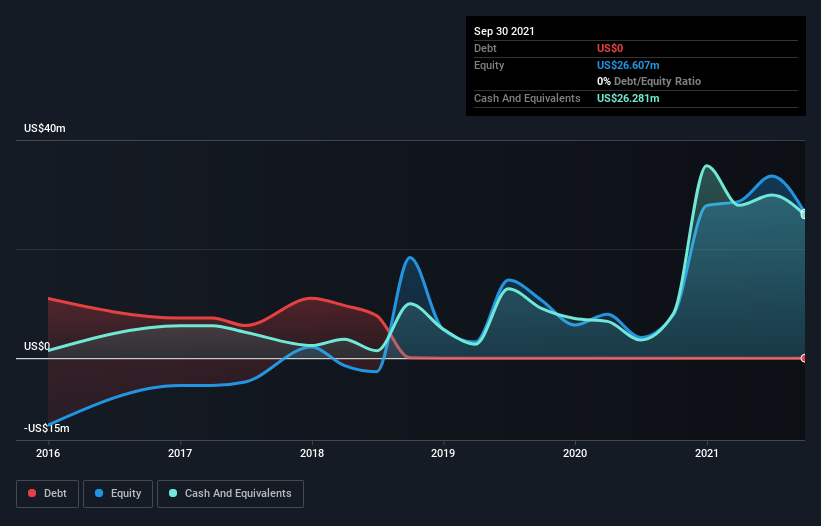

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. In September 2021, SELLAS Life Sciences Group had US$26m in cash, and was debt-free. Importantly, its cash burn was US$18m over the trailing twelve months. Therefore, from September 2021 it had roughly 18 months of cash runway. Importantly, analysts think that SELLAS Life Sciences Group will reach cashflow breakeven in 4 years. That means unless the company reduces its cash burn quickly, it may well look to raise more cash. The image below shows how its cash balance has been changing over the last few years.

How Is SELLAS Life Sciences Group's Cash Burn Changing Over Time?

In our view, SELLAS Life Sciences Group doesn't yet produce significant amounts of operating revenue, since it reported just US$9.5m in the last twelve months. Therefore, for the purposes of this analysis we'll focus on how the cash burn is tracking. As it happens, the company's cash burn reduced by 2.2% over the last year, which suggests that management are maintaining a fairly steady rate of business development, albeit with a slight decrease in spending. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Easily Can SELLAS Life Sciences Group Raise Cash?

While SELLAS Life Sciences Group is showing a solid reduction in its cash burn, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

SELLAS Life Sciences Group has a market capitalisation of US$105m and burnt through US$18m last year, which is 17% of the company's market value. As a result, we'd venture that the company could raise more cash for growth without much trouble, albeit at the cost of some dilution.

Is SELLAS Life Sciences Group's Cash Burn A Worry?

SELLAS Life Sciences Group appears to be in pretty good health when it comes to its cash burn situation. Not only was its cash burn relative to its market cap quite good, but its cash runway was a real positive. Shareholders can take heart from the fact that analysts are forecasting it will reach breakeven. We don't think its cash burn is particularly problematic, but after considering the range of factors in this article, we do think shareholders should be monitoring how it changes over time. On another note, SELLAS Life Sciences Group has 4 warning signs (and 2 which are potentially serious) we think you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:SLS

SELLAS Life Sciences Group

A late-stage clinical biopharmaceutical company, focuses on the development of novel cancer immunotherapies for various cancer indications in the United States.

Moderate with adequate balance sheet.