- United States

- /

- Biotech

- /

- NasdaqGS:PSTX

Investors Don't See Light At End Of Poseida Therapeutics, Inc.'s (NASDAQ:PSTX) Tunnel And Push Stock Down 30%

Poseida Therapeutics, Inc. (NASDAQ:PSTX) shares have had a horrible month, losing 30% after a relatively good period beforehand. The last month has meant the stock is now only up 4.3% during the last year.

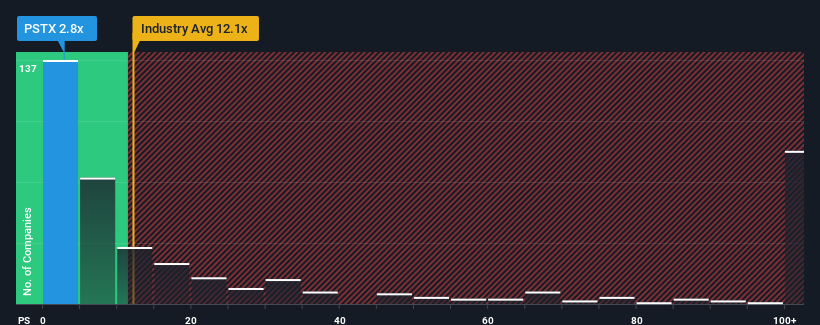

After such a large drop in price, Poseida Therapeutics' price-to-sales (or "P/S") ratio of 2.7x might make it look like a strong buy right now compared to the wider Biotechs industry in the United States, where around half of the companies have P/S ratios above 12.1x and even P/S above 73x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

Check out our latest analysis for Poseida Therapeutics

How Has Poseida Therapeutics Performed Recently?

Poseida Therapeutics hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. Perhaps the P/S remains low as investors think the prospects of strong revenue growth aren't on the horizon. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

Want the full picture on analyst estimates for the company? Then our free report on Poseida Therapeutics will help you uncover what's on the horizon.How Is Poseida Therapeutics' Revenue Growth Trending?

In order to justify its P/S ratio, Poseida Therapeutics would need to produce anemic growth that's substantially trailing the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 44%. This has erased any of its gains during the last three years, with practically no change in revenue being achieved in total. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Shifting to the future, estimates from the three analysts covering the company suggest revenue growth is heading into negative territory, declining 11% each year over the next three years. Meanwhile, the broader industry is forecast to expand by 147% per annum, which paints a poor picture.

With this in consideration, we find it intriguing that Poseida Therapeutics' P/S is closely matching its industry peers. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

What We Can Learn From Poseida Therapeutics' P/S?

Poseida Therapeutics' P/S looks about as weak as its stock price lately. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

With revenue forecasts that are inferior to the rest of the industry, it's no surprise that Poseida Therapeutics' P/S is on the lower end of the spectrum. As other companies in the industry are forecasting revenue growth, Poseida Therapeutics' poor outlook justifies its low P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

You need to take note of risks, for example - Poseida Therapeutics has 3 warning signs (and 1 which is significant) we think you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:PSTX

Poseida Therapeutics

A clinical-stage biopharmaceutical company, focuses on developing therapeutics for patients with high unmet medical needs.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Community Narratives