Advertisement

- United States

- /

- Life Sciences

- /

- NasdaqGM:OLK

Olink Holding AB (publ) (NASDAQ:OLK) Just Reported, And Analysts Assigned A US$29.75 Price Target

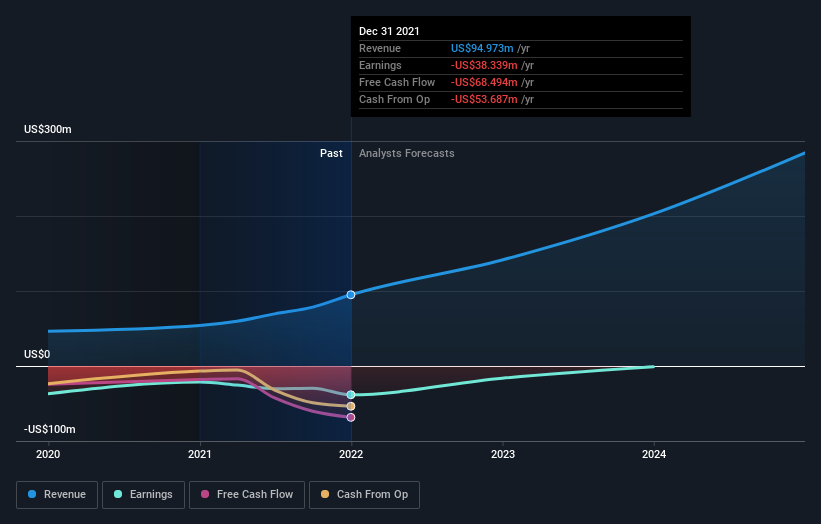

Last week, you might have seen that Olink Holding AB (publ) (NASDAQ:OLK) released its yearly result to the market. The early response was not positive, with shares down 2.8% to US$18.76 in the past week. Revenues of US$95m beat expectations by a respectable 2.5%, although statutory losses per share increased. Olink Holding lost US$0.43, which was 51% more than what the analysts had included in their models. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

See our latest analysis for Olink Holding

After the latest results, the four analysts covering Olink Holding are now predicting revenues of US$141.3m in 2022. If met, this would reflect a substantial 49% improvement in sales compared to the last 12 months. Losses are predicted to fall substantially, shrinking 41% to US$0.19. Before this earnings announcement, the analysts had been modelling revenues of US$145.2m and losses of US$0.14 per share in 2022. So it's pretty clear the analysts have mixed opinions on Olink Holding after this update; revenues were downgraded and per-share losses expected to increase.

The consensus price target fell 16% to US$29.75, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Olink Holding analyst has a price target of US$44.00 per share, while the most pessimistic values it at US$23.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that Olink Holding's revenue growth is expected to slow, with the forecast 49% annualised growth rate until the end of 2022 being well below the historical 76% growth over the last year. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 8.3% annually. Even after the forecast slowdown in growth, it seems obvious that Olink Holding is also expected to grow faster than the wider industry.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at Olink Holding. They also downgraded their revenue estimates, although industry data suggests that Olink Holding's revenues are expected to grow faster than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Olink Holding going out to 2024, and you can see them free on our platform here.

Plus, you should also learn about the 2 warning signs we've spotted with Olink Holding .

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:OLK

Olink Holding

Develops, produces, markets, and sells biotechnological products and services for the academic, government, biopharmaceutical, biotechnology, service provider, and other institutions that focuses on life science research.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative