- United States

- /

- Biotech

- /

- NasdaqCM:IRD

Ocuphire Pharma, Inc. (NASDAQ:OCUP) Shares May Have Slumped 26% But Getting In Cheap Is Still Unlikely

Ocuphire Pharma, Inc. (NASDAQ:OCUP) shareholders that were waiting for something to happen have been dealt a blow with a 26% share price drop in the last month. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 51% loss during that time.

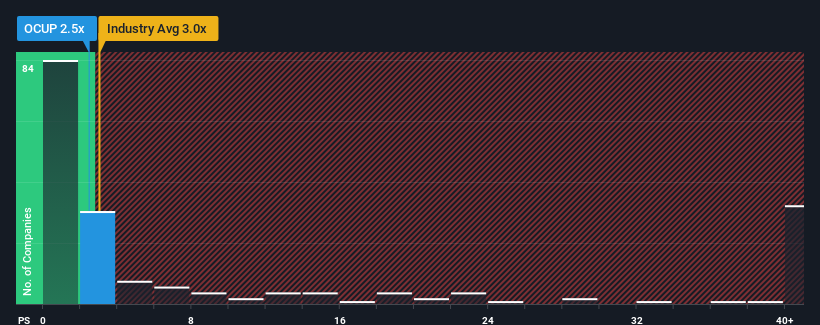

In spite of the heavy fall in price, you could still be forgiven for feeling indifferent about Ocuphire Pharma's P/S ratio of 2.5x, since the median price-to-sales (or "P/S") ratio for the Pharmaceuticals industry in the United States is also close to 3x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Ocuphire Pharma

What Does Ocuphire Pharma's Recent Performance Look Like?

Ocuphire Pharma hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on Ocuphire Pharma will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For Ocuphire Pharma?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Ocuphire Pharma's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 52% decrease to the company's top line. At least revenue has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Shifting to the future, estimates from the four analysts covering the company suggest revenue should grow by 25% per year over the next three years. With the industry predicted to deliver 36% growth per year, the company is positioned for a weaker revenue result.

With this information, we find it interesting that Ocuphire Pharma is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

The Final Word

Following Ocuphire Pharma's share price tumble, its P/S is just clinging on to the industry median P/S. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

When you consider that Ocuphire Pharma's revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. A positive change is needed in order to justify the current price-to-sales ratio.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Ocuphire Pharma that you should be aware of.

If these risks are making you reconsider your opinion on Ocuphire Pharma, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:IRD

Opus Genetics

A clinical-stage ophthalmic biopharmaceutical company, focuses on developing and commercializing therapies for the treatment of inherited retinal diseases.

Flawless balance sheet slight.

Market Insights

Community Narratives