- United States

- /

- Pharma

- /

- NasdaqGS:NGM

What NGM Biopharmaceuticals, Inc.'s (NASDAQ:NGM) 32% Share Price Gain Is Not Telling You

NGM Biopharmaceuticals, Inc. (NASDAQ:NGM) shareholders are no doubt pleased to see that the share price has bounced 32% in the last month, although it is still struggling to make up recently lost ground. But the last month did very little to improve the 84% share price decline over the last year.

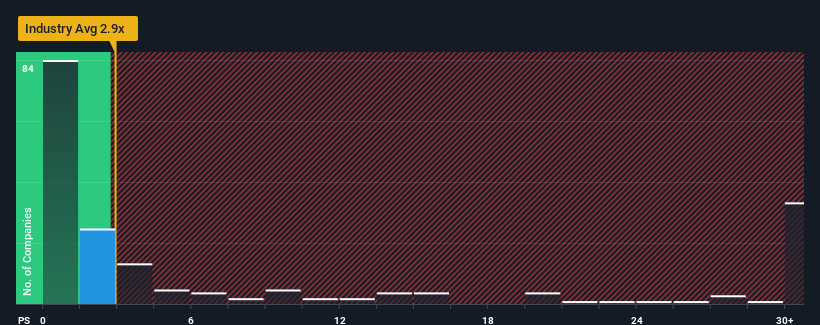

Although its price has surged higher, you could still be forgiven for feeling indifferent about NGM Biopharmaceuticals' P/S ratio of 2.9x, since the median price-to-sales (or "P/S") ratio for the Pharmaceuticals industry in the United States is about the same. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for NGM Biopharmaceuticals

What Does NGM Biopharmaceuticals' Recent Performance Look Like?

NGM Biopharmaceuticals could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on NGM Biopharmaceuticals will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The P/S?

NGM Biopharmaceuticals' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 61%. The last three years don't look nice either as the company has shrunk revenue by 77% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to slump, contracting by 90% per year during the coming three years according to the six analysts following the company. Meanwhile, the broader industry is forecast to expand by 53% per annum, which paints a poor picture.

In light of this, it's somewhat alarming that NGM Biopharmaceuticals' P/S sits in line with the majority of other companies. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh on the share price eventually.

What Does NGM Biopharmaceuticals' P/S Mean For Investors?

Its shares have lifted substantially and now NGM Biopharmaceuticals' P/S is back within range of the industry median. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

While NGM Biopharmaceuticals' P/S isn't anything out of the ordinary for companies in the industry, we didn't expect it given forecasts of revenue decline. With this in mind, we don't feel the current P/S is justified as declining revenues are unlikely to support a more positive sentiment for long. If we consider the revenue outlook, the P/S seems to indicate that potential investors may be paying a premium for the stock.

And what about other risks? Every company has them, and we've spotted 3 warning signs for NGM Biopharmaceuticals you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

If you're looking to trade NGM Biopharmaceuticals, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NGM Biopharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:NGM

NGM Biopharmaceuticals

NGM Biopharmaceuticals, Inc., a biopharmaceutical company, engages in the discovery and development of novel therapeutics to treat liver and metabolic diseases, retinal diseases, and cancer.

Flawless balance sheet with limited growth.