Advertisement

- United States

- /

- Life Sciences

- /

- NasdaqGS:LAB

Market Participants Recognise Standard BioTools Inc.'s (NASDAQ:LAB) Revenues Pushing Shares 33% Higher

Those holding Standard BioTools Inc. (NASDAQ:LAB) shares would be relieved that the share price has rebounded 33% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 27% in the last twelve months.

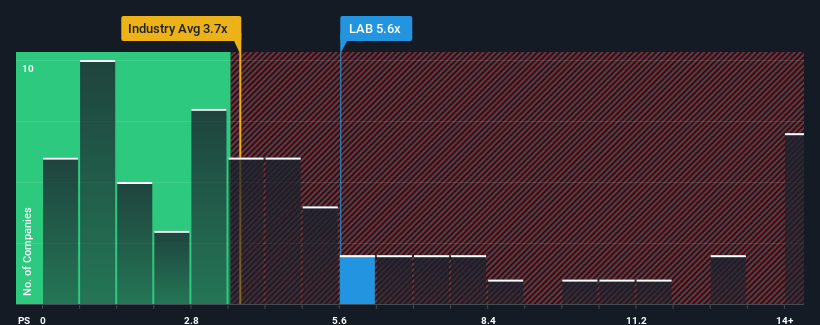

Following the firm bounce in price, when almost half of the companies in the United States' Life Sciences industry have price-to-sales ratios (or "P/S") below 3.7x, you may consider Standard BioTools as a stock probably not worth researching with its 5.6x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

See our latest analysis for Standard BioTools

What Does Standard BioTools' Recent Performance Look Like?

Standard BioTools certainly has been doing a good job lately as its revenue growth has been positive while most other companies have been seeing their revenue go backwards. Perhaps the market is expecting the company's future revenue growth to buck the trend of the industry, contributing to a higher P/S. If not, then existing shareholders might be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Standard BioTools.What Are Revenue Growth Metrics Telling Us About The High P/S?

In order to justify its P/S ratio, Standard BioTools would need to produce impressive growth in excess of the industry.

Retrospectively, the last year delivered an exceptional 29% gain to the company's top line. Still, revenue has fallen 8.1% in total from three years ago, which is quite disappointing. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the three analysts covering the company suggest revenue should grow by 24% per annum over the next three years. With the industry only predicted to deliver 7.2% per year, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Standard BioTools' P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

The large bounce in Standard BioTools' shares has lifted the company's P/S handsomely. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Standard BioTools' analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 3 warning signs for Standard BioTools (of which 2 can't be ignored!) you should know about.

If these risks are making you reconsider your opinion on Standard BioTools, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:LAB

Standard BioTools

Develops, manufactures, and sells a range of instrumentation, consumables, and services to scientists and biomedical researchers to develop therapeutics in the Americas, Europe, the Middle East, Africa, and the Asia pacific.

Flawless balance sheet and overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor