- United States

- /

- Biotech

- /

- NasdaqGM:KYMR

Analysts Are Upgrading Kymera Therapeutics, Inc. (NASDAQ:KYMR) After Its Latest Results

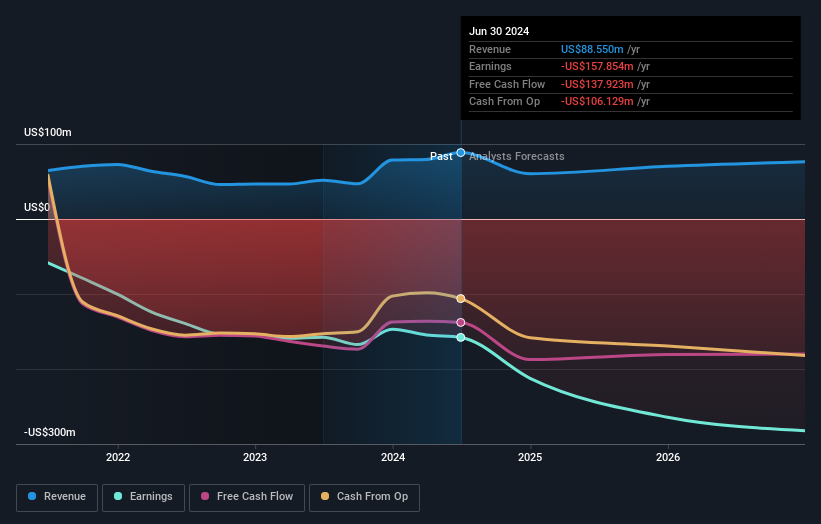

Kymera Therapeutics, Inc. (NASDAQ:KYMR) just released its latest quarterly results and things are looking bullish. Results clearly exceeded expectations, with a substantial revenue beat leading to smaller losses in what looks like a definite win for investors. Revenues were US$26m and the statutory loss per share was US$0.58, smaller than the analysts had forecast. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for Kymera Therapeutics

Taking into account the latest results, the 18 analysts covering Kymera Therapeutics provided consensus estimates of US$60.5m revenue in 2024, which would reflect a sizeable 32% decline over the past 12 months. Per-share losses are supposed to see a sharp uptick, reaching US$2.93. Before this latest report, the consensus had been expecting revenues of US$55.1m and US$2.90 per share in losses.

There were no major changes to the US$52.07consensus price target despite the higher revenue estimates, with the analysts seeming to believe that ongoing losses have a larger impact on the valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Kymera Therapeutics, with the most bullish analyst valuing it at US$112 and the most bearish at US$30.00 per share. With such a wide range in price targets, analysts are almost certainly betting on widely divergent outcomes in the underlying business. With this in mind, we wouldn't rely too heavily the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Kymera Therapeutics' past performance and to peers in the same industry. We would highlight that revenue is expected to reverse, with a forecast 53% annualised decline to the end of 2024. That is a notable change from historical growth of 5.4% over the last three years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 23% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Kymera Therapeutics is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that the analysts reconfirmed their loss per share estimates for next year. They also upgraded their revenue estimates for next year, even though it is expected to grow slower than the wider industry. The consensus price target held steady at US$52.07, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on Kymera Therapeutics. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for Kymera Therapeutics going out to 2026, and you can see them free on our platform here..

It is also worth noting that we have found 4 warning signs for Kymera Therapeutics (1 is a bit concerning!) that you need to take into consideration.

Valuation is complex, but we're here to simplify it.

Discover if Kymera Therapeutics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:KYMR

Kymera Therapeutics

A biopharmaceutical company, focuses on discovering and developing novel small molecule therapeutics that selectively degrade disease-causing proteins by harnessing the body’s own natural protein degradation system.

Flawless balance sheet and slightly overvalued.

Market Insights

Community Narratives