- United States

- /

- Biotech

- /

- NasdaqGM:FHTX

Foghorn Therapeutics Inc.'s (NASDAQ:FHTX) Share Price Boosted 71% But Its Business Prospects Need A Lift Too

Foghorn Therapeutics Inc. (NASDAQ:FHTX) shareholders would be excited to see that the share price has had a great month, posting a 71% gain and recovering from prior weakness. Longer-term shareholders would be thankful for the recovery in the share price since it's now virtually flat for the year after the recent bounce.

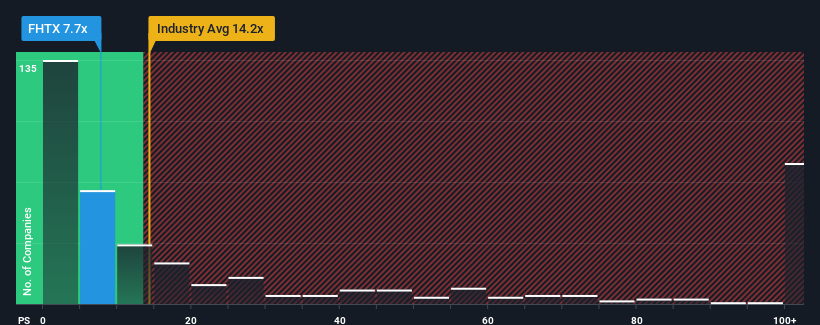

In spite of the firm bounce in price, Foghorn Therapeutics may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 7.7x, considering almost half of all companies in the Biotechs industry in the United States have P/S ratios greater than 14.2x and even P/S higher than 65x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

Check out our latest analysis for Foghorn Therapeutics

How Foghorn Therapeutics Has Been Performing

Foghorn Therapeutics certainly has been doing a good job lately as it's been growing revenue more than most other companies. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Want the full picture on analyst estimates for the company? Then our free report on Foghorn Therapeutics will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The Low P/S?

The only time you'd be truly comfortable seeing a P/S as low as Foghorn Therapeutics' is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered an exceptional 107% gain to the company's top line. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Shifting to the future, estimates from the four analysts covering the company suggest revenue should grow by 22% each year over the next three years. Meanwhile, the rest of the industry is forecast to expand by 269% per annum, which is noticeably more attractive.

With this in consideration, its clear as to why Foghorn Therapeutics' P/S is falling short industry peers. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From Foghorn Therapeutics' P/S?

Foghorn Therapeutics' stock price has surged recently, but its but its P/S still remains modest. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of Foghorn Therapeutics' analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. The company will need a change of fortune to justify the P/S rising higher in the future.

Before you take the next step, you should know about the 3 warning signs for Foghorn Therapeutics (2 can't be ignored!) that we have uncovered.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:FHTX

Foghorn Therapeutics

A clinical-stage biopharmaceutical company, engages in the discovery and development of medicines targeting genetically determined dependencies within the chromatin regulatory system in the United States.

Slight with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives