- United States

- /

- Biotech

- /

- OTCPK:EGRX

These 4 Measures Indicate That Eagle Pharmaceuticals (NASDAQ:EGRX) Is Using Debt Safely

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Eagle Pharmaceuticals, Inc. (NASDAQ:EGRX) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Eagle Pharmaceuticals

What Is Eagle Pharmaceuticals's Debt?

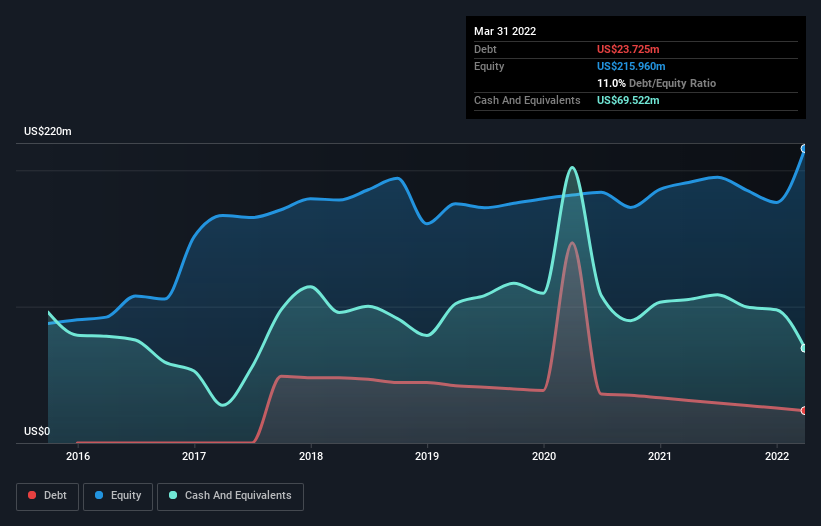

The image below, which you can click on for greater detail, shows that Eagle Pharmaceuticals had debt of US$23.7m at the end of March 2022, a reduction from US$31.3m over a year. However, its balance sheet shows it holds US$69.5m in cash, so it actually has US$45.8m net cash.

A Look At Eagle Pharmaceuticals' Liabilities

Zooming in on the latest balance sheet data, we can see that Eagle Pharmaceuticals had liabilities of US$101.6m due within 12 months and liabilities of US$2.56m due beyond that. Offsetting these obligations, it had cash of US$69.5m as well as receivables valued at US$136.8m due within 12 months. So it actually has US$102.2m more liquid assets than total liabilities.

This excess liquidity suggests that Eagle Pharmaceuticals is taking a careful approach to debt. Due to its strong net asset position, it is not likely to face issues with its lenders. Simply put, the fact that Eagle Pharmaceuticals has more cash than debt is arguably a good indication that it can manage its debt safely.

Better yet, Eagle Pharmaceuticals grew its EBIT by 193% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Eagle Pharmaceuticals's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Eagle Pharmaceuticals has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Eagle Pharmaceuticals recorded free cash flow worth a fulsome 85% of its EBIT, which is stronger than we'd usually expect. That puts it in a very strong position to pay down debt.

Summing up

While it is always sensible to investigate a company's debt, in this case Eagle Pharmaceuticals has US$45.8m in net cash and a decent-looking balance sheet. The cherry on top was that in converted 85% of that EBIT to free cash flow, bringing in US$1.0m. The bottom line is that we do not find Eagle Pharmaceuticals's debt levels at all concerning. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 2 warning signs we've spotted with Eagle Pharmaceuticals .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you're looking to trade Eagle Pharmaceuticals, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Eagle Pharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:EGRX

Eagle Pharmaceuticals

A pharmaceutical company, focuses on developing and commercializing product candidates to treat diseases of the central nervous system or metabolic critical care, and oncology in the United States.

Low with weak fundamentals.