Advertisement

- United States

- /

- Pharma

- /

- NasdaqCM:CORT

Corcept Therapeutics (CORT): Assessing Valuation After Revenue Outlook Revision and Growth in Korlym Prescriptions

Simply Wall St

Reviewed by Simply Wall St

Corcept Therapeutics (CORT) has adjusted its revenue outlook for 2025, citing capacity constraints with a previous specialty pharmacy vendor. This adjustment comes as new prescriptions for Korlym continue to increase in its hypercortisolism segment.

See our latest analysis for Corcept Therapeutics.

Corcept’s revenue guidance revision comes after strong momentum in both its core business and share price. Despite recent insider selling and mixed third-quarter results, the stock has delivered a 59.7% year-to-date share price return. Its three-year total shareholder return of 219% indicates that long-term growth potential remains a consideration.

If you’re curious about what other innovative healthcare names are gaining traction, discover new opportunities with our See the full list for free.

With analyst price targets well above current levels, along with strong growth in both revenue and new prescriptions, is Corcept Therapeutics undervalued at today’s share price or has the market already priced in its potential upside?

Most Popular Narrative: 40.7% Undervalued

The latest widely followed narrative pegs Corcept Therapeutics’ fair value at $134.50, which stands far above the last close of $79.80. This gap invites close attention to the ambitious growth expectations baked into the consensus fair value estimate.

The publication of the CATALYST study and the resulting increased awareness and screening for hypercortisolism among physicians are expanding the potential addressable patient pool. This is expected to drive significant acceleration in revenue growth over the next several years.

Want to know the bold growth assumptions powering this valuation? The narrative hinges on rapid sales expansion, margin transformation, and aggressive earnings projections few companies can match. Dive in to see the exact levers propelling this price target. Discover if you agree with the aggressive forecast.

Result: Fair Value of $134.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, heavy reliance on Korlym and potential setbacks in upcoming regulatory approvals could undermine the company’s projected growth trajectory in the coming years.

Find out about the key risks to this Corcept Therapeutics narrative.

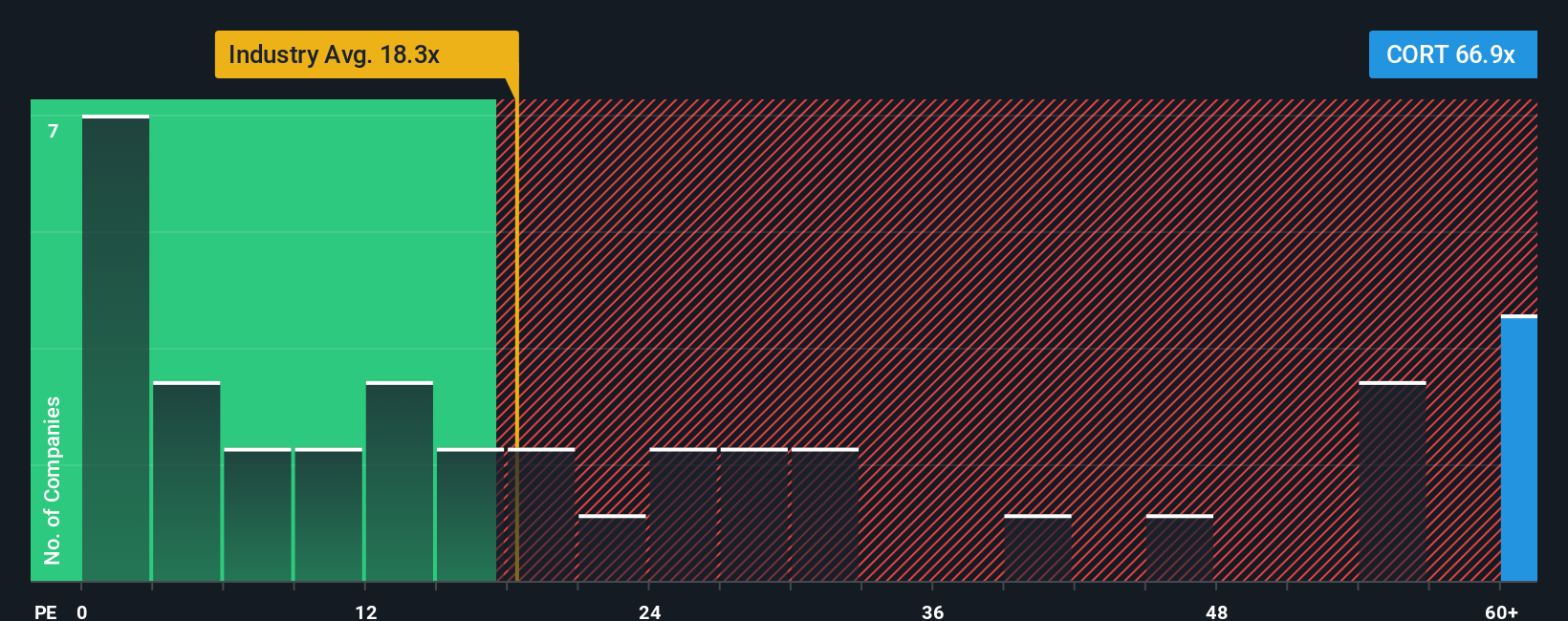

Another View: What Do the Multiples Say?

Shifting from price targets to industry comparisons, Corcept Therapeutics trades at a price-to-earnings ratio of 80.2x, which is far higher than both the Pharmaceuticals industry average of 20.6x and its peer average of 35.6x. Even compared to a fair ratio of 68.5x, the current valuation remains stretched. For investors, could this signal more risk if high growth expectations are not met?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Corcept Therapeutics Narrative

If you have a different perspective or want to see how your own analysis compares, you can quickly put together your own narrative and get fresh insights in just a few minutes. Do it your way

A great starting point for your Corcept Therapeutics research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors know that casting a wider net can uncover hidden gems and fresh opportunities. Don’t let your next great pick slip through your fingers.

- Grow your passive income by tapping into these 15 dividend stocks with yields > 3%, which spotlights stocks with strong yields and established track records.

- Capture early-stage momentum by targeting these 3579 penny stocks with strong financials, featuring financial resilience and breakthrough growth stories.

- Stay ahead of the curve in medical innovation by exploring these 30 healthcare AI stocks, bringing you tomorrow’s leaders in AI-driven healthcare solutions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:CORT

Corcept Therapeutics

Engages in discovery and development of medication for the treatment of severe endocrinologic, oncologic, metabolic, and neurologic disorders in the United States.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative