Advertisement

- United States

- /

- Biotech

- /

- OTCPK:CLVS.Q

How Is Clovis Oncology's (NASDAQ:CLVS) CEO Paid Relative To Peers?

This article will reflect on the compensation paid to Patrick Mahaffy who has served as CEO of Clovis Oncology, Inc. (NASDAQ:CLVS) since 2009. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

Check out our latest analysis for Clovis Oncology

How Does Total Compensation For Patrick Mahaffy Compare With Other Companies In The Industry?

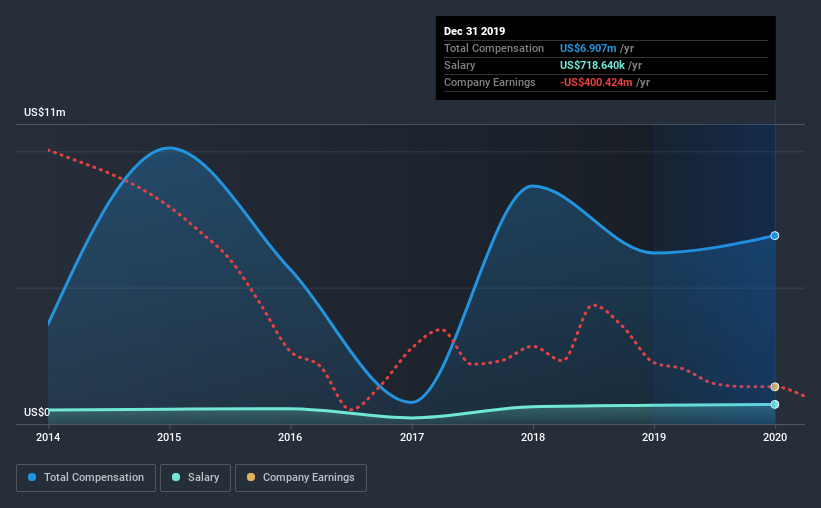

At the time of writing, our data shows that Clovis Oncology, Inc. has a market capitalization of US$575m, and reported total annual CEO compensation of US$6.9m for the year to December 2019. That's a notable increase of 10% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at US$719k.

In comparison with other companies in the industry with market capitalizations ranging from US$200m to US$800m, the reported median CEO total compensation was US$2.4m. Hence, we can conclude that Patrick Mahaffy is remunerated higher than the industry median. Moreover, Patrick Mahaffy also holds US$6.3m worth of Clovis Oncology stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | US$719k | US$689k | 10% |

| Other | US$6.2m | US$5.6m | 90% |

| Total Compensation | US$6.9m | US$6.3m | 100% |

Talking in terms of the industry, salary represented approximately 23% of total compensation out of all the companies we analyzed, while other remuneration made up 77% of the pie. It's interesting to note that Clovis Oncology allocates a smaller portion of compensation to salary in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Clovis Oncology, Inc.'s Growth

Over the past three years, Clovis Oncology, Inc. has seen its earnings per share (EPS) grow by 4.7% per year. In the last year, its revenue is up 38%.

We like the look of the strong year-on-year improvement in revenue. Combined with modest EPS growth, we get a good impression of the company. We'd stop short of saying the business performance is amazing, but there are enough positives to justify further research, or even adding the stock to your watch-list. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Clovis Oncology, Inc. Been A Good Investment?

Since shareholders would have lost about 92% over three years, some Clovis Oncology, Inc. investors would surely be feeling negative emotions. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

As previously discussed, Patrick is compensated more than what is normal for CEOs of companies of similar size, and which belong to the same industry. Over the last three years, shareholder returns have been downright disappointing for Clovis Oncology, and although earnings growth is steady, it hasn't set the world on fire. And the situation doesn't look all that good when you see Patrick is remunerated higher than the industry average. All things considered, we believe shareholders would be disappointed to see Patrick's compensation grow without first seeing an improvement in the performance of the company.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We did our research and identified 3 warning signs (and 1 which doesn't sit too well with us) in Clovis Oncology we think you should know about.

Switching gears from Clovis Oncology, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you decide to trade Clovis Oncology, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About OTCPK:CLVS.Q

Clovis Oncology

Clovis Oncology, Inc., a biopharmaceutical company, focuses on acquiring, developing, and commercializing anti-cancer agents in the United States, Europe, and internationally.

Slightly overvalued with weak fundamentals.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|18.3% undervalued

BL

Community Contributor