Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Apellis Pharmaceuticals, Inc. (NASDAQ:APLS) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

What Is Apellis Pharmaceuticals's Debt?

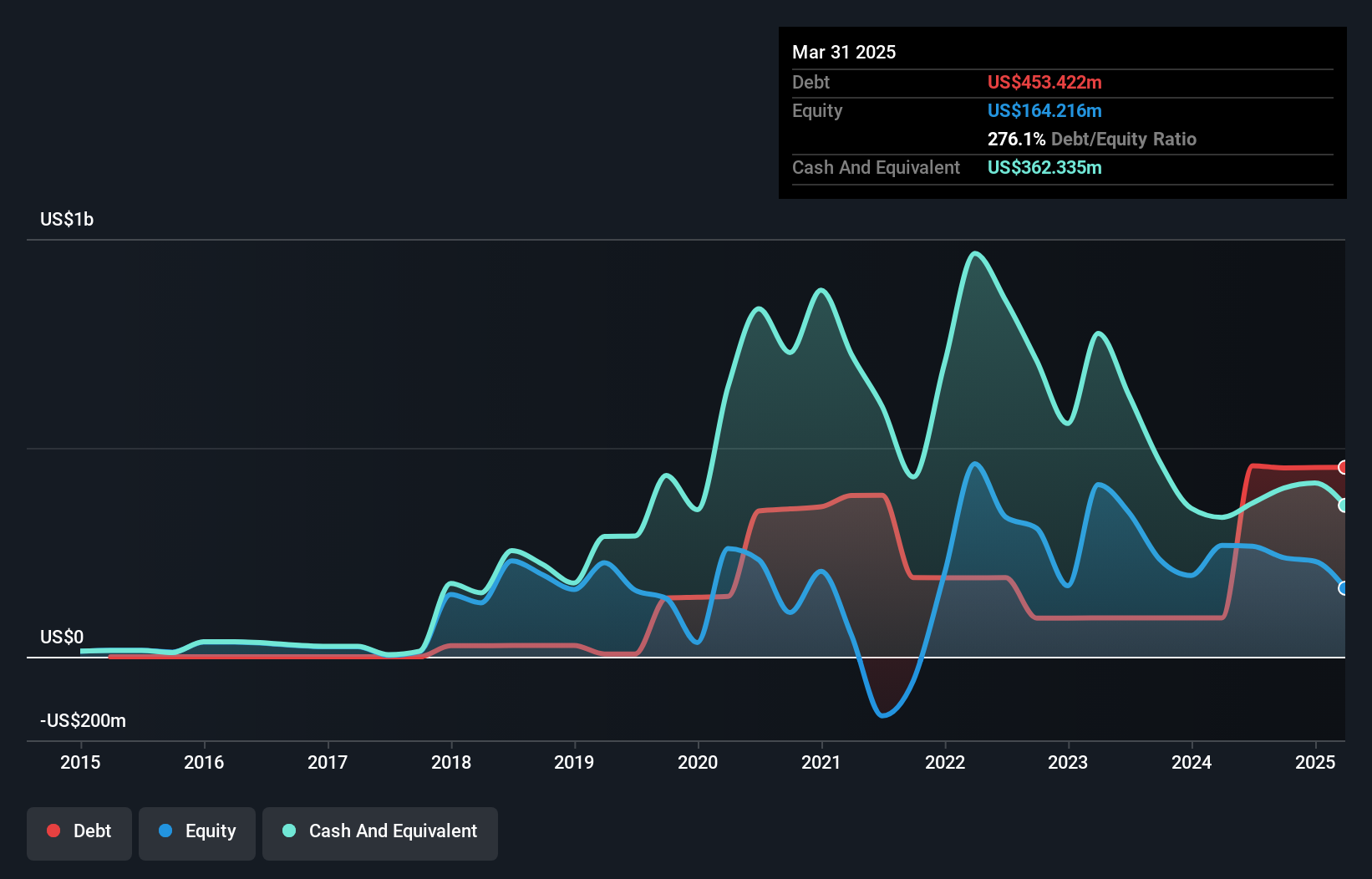

As you can see below, at the end of March 2025, Apellis Pharmaceuticals had US$453.4m of debt, up from US$93.1m a year ago. Click the image for more detail. However, because it has a cash reserve of US$362.3m, its net debt is less, at about US$91.1m.

A Look At Apellis Pharmaceuticals' Liabilities

Zooming in on the latest balance sheet data, we can see that Apellis Pharmaceuticals had liabilities of US$178.4m due within 12 months and liabilities of US$464.7m due beyond that. On the other hand, it had cash of US$362.3m and US$244.4m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$36.4m.

This state of affairs indicates that Apellis Pharmaceuticals' balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the US$2.46b company is short on cash, but still worth keeping an eye on the balance sheet. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Apellis Pharmaceuticals can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Check out our latest analysis for Apellis Pharmaceuticals

In the last year Apellis Pharmaceuticals wasn't profitable at an EBIT level, but managed to grow its revenue by 48%, to US$776m. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

While we can certainly appreciate Apellis Pharmaceuticals's revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. To be specific the EBIT loss came in at US$186m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled US$8.4m in negative free cash flow over the last twelve months. So to be blunt we think it is risky. For riskier companies like Apellis Pharmaceuticals I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:APLS

Apellis Pharmaceuticals

A commercial-stage biopharmaceutical company, focuses on the discovery, development, and commercialization of novel therapeutic compounds to treat diseases with high unmet needs.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets