- United States

- /

- Interactive Media and Services

- /

- NYSE:TWTR

If Twitter (NYSE:TWTR) Improves the Selection Effect, it has a Potential to be a Multi-Bagger

The most recent social media outage brought Twitter, Inc. (NYSE: TWTR) into focus, as it "saved the day" for the social media.

Yet, the stock suffered one of the most significant recent single-day drops, leading the broad market by a wide margin. The stock now trades over 25% below the yearly highs.

Check out our latest analysis for Twitter

Growth and Innovation

In the latest round of innovation, Twitter announced 3 new options:

- Tips: Allow donations to followers through several payment options (even Bitcoin).

- Super Follows: Content monetization through creating a separate tier of followers that pay a monthly subscription.

- Safety Mode: Option to temporarily reduce the negative engagement like spam or harmful language.

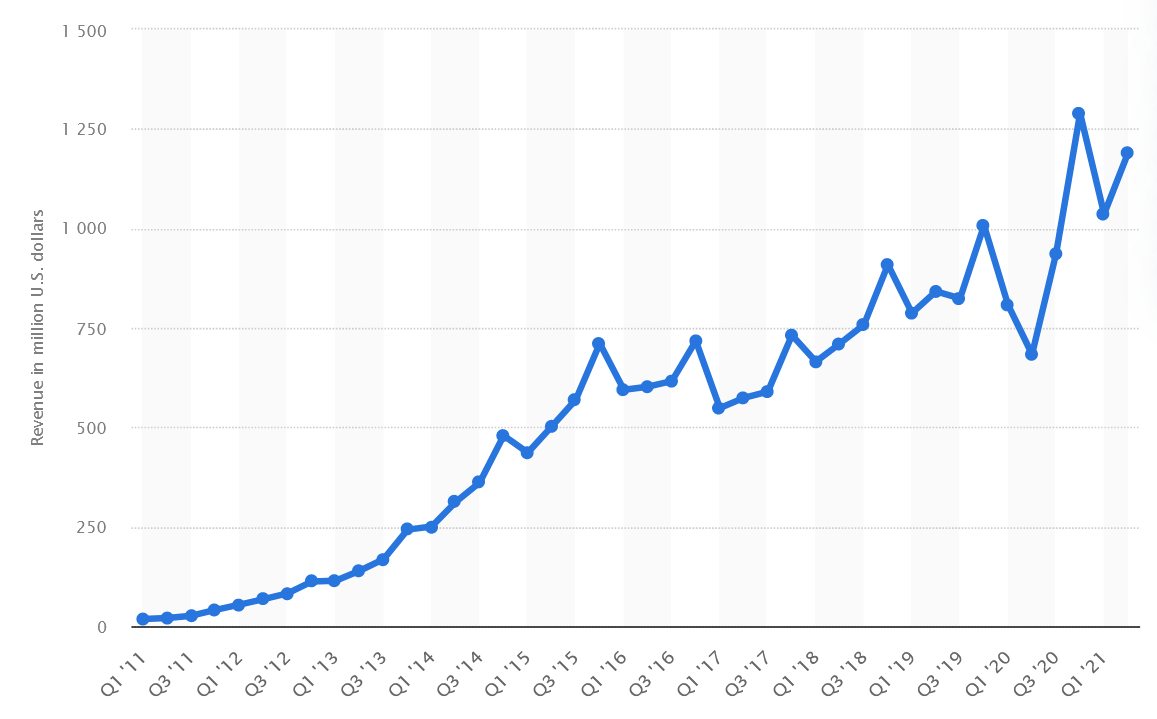

Although the company doesn't expect to report significant (if any) GAAP operating income for Q3, the growth is evident because the company currently has 650+ job openings around the world.

Selection Effect vs. Advertising Effect – The Problem with Online Advertising

Once upon a time, a local pizzeria hired 3 boys to hand out the coupons. After a short time, it was clear that one of them was a significant outperformer. At the end of the day, his coupons would dominate in the stack. Yet, his secret was simple – stand near the pizzeria and hand coupons to the people going in.

This is the biggest problem of online advertising. While the advertising revenue is skyrocketing, it is hard to distinguish the selective traffic (one that is going to the pizzeria anyways) vs. advertised traffic (one that is sent to the pizzeria).

Algorithmic targeting is only increasing the selective traffic, and this is something where we believe that Twitter has an opportunity to differentiate itself from the competition. Focusing on the metrics of the advertised traffic would be a significant step to boost the margins, especially for B2B revenue, which is often recurring.

Estimating the Intrinsic Value - Discounted Cash Flow Model

Remember, though, that there are many ways to estimate a company's value, and a DCF is just one method. For those keen learners of equity analysis, the Simply Wall St analysis model here may be something of interest to you.

Crunching the numbers

We will use a two-stage DCF model, which, as the name states, considers two stages of growth. The first stage is generally a higher growth period which levels off heading towards the terminal value, captured in the second 'steady growth' period.

In the first stage, we need to estimate the cash flows to the business over the next ten years. Where possible, we use analyst estimates, but when these aren't available, we extrapolate the previous free cash flow (FCF) from the last estimate or reported value.

We assume companies with shrinking free cash flow will slow their rate of shrinkage and that companies with growing free cash flow will see their growth rate slow over this period. We do this to reflect that growth tends to slow more in the early years than in later years.

A DCF is all about the idea that a dollar in the future is less valuable than a dollar today, so we need to discount the sum of these future cash flows to arrive at a present value estimate:

10-year free cash flow (FCF) forecast

| 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | |

| Levered FCF ($, Millions) | US$812.4m | US$1.09b | US$1.54b | US$2.38b | US$2.99b | US$3.54b | US$4.01b | US$4.41b | US$4.75b | US$5.03b |

| Growth Rate Estimate Source | Analyst x8 | Analyst x6 | Analyst x2 | Analyst x1 | Est @ 25.38% | Est @ 18.35% | Est @ 13.44% | Est @ 9.99% | Est @ 7.58% | Est @ 5.9% |

| Present Value ($, Millions) Discounted @ 7.0% | US$759 | US$954 | US$1.3k | US$1.8k | US$2.1k | US$2.4k | US$2.5k | US$2.6k | US$2.6k | US$2.6k |

("Est" = FCF growth rate estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = US$20b

The second stage is also known as Terminal Value; this is the business's cash flow after the first stage. The Gordon Growth formula is used to calculate Terminal Value at a future annual growth rate equal to the 5-year average of the 10-year government bond yield of 2.0%. We discount the terminal cash flows to today's value at the cost of equity of 7.0%.

Terminal Value (TV)= FCF2031 × (1 + g) ÷ (r - g) = US$5.0b× (1 + 2.0%) ÷ (7.0% - 2.0%) = US$102b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= US$102b÷ ( 1 + 7.0%)10= US$52b

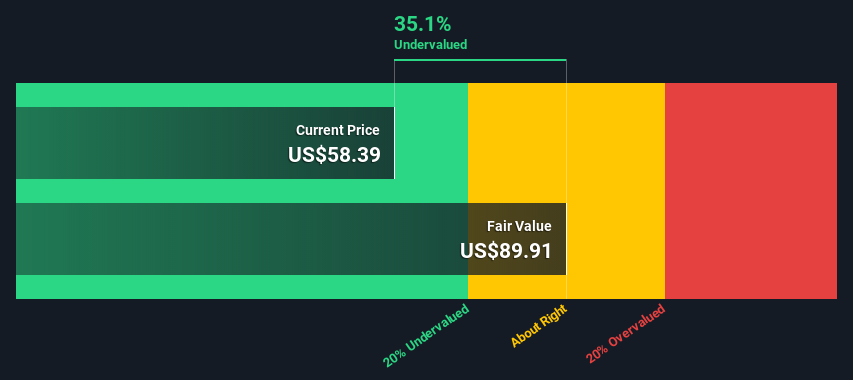

The total value is the sum of cash flows for the next ten years plus the discounted terminal value, which results in the Total Equity Value, which in this case is US$72b.

In the final step, we divide the equity value by the number of shares outstanding. Compared to the current share price of US$58.4, the company appears quite good value at a 35% discount to where the stock price trades currently.

Remember, though, that this is just an approximate valuation.

Important assumptions

The calculation above is dependent on two assumptions. The first is the discount rate, and the other is the cash flows. The DCF also does not consider the possible cyclicality of an industry or a company's future capital requirements, so it does not give a complete picture of its potential performance.

Given that we are looking at Twitter as potential shareholders, the cost of equity is used as the discount rate rather than the cost of capital (or the weighted average cost of capital, WACC), which accounts for debt.

We've used 7.0% in this calculation, which is based on a levered beta of 1.145. Beta is a measure of a stock's volatility compared to the market as a whole. We get our beta from the industry average beta of globally comparable companies, with an imposed limit between 0.8 and 2.0, which is a reasonable range for a stable business.

Looking Ahead:

Valuation is only one side of the coin in terms of building your investment thesis, and it is only one of many factors that you need to assess for a company. DCF models are not the be-all and end-all of investment valuation.

For Twitter, there are three essential items you should further research:

- Risks: For example, we've discovered 2 warning signs for Twitter that you should be aware of before investing here. Furthermore, Twitter has a rich valuation compared to its current revenue - it has to keep growing at a modest rate to mandate it.

- Management: Have insiders been ramping up their shares to take advantage of the market's sentiment for TWTR's future outlook? Check out our management and board analysis with insights on CEO compensation and governance factors.

- Other Solid Businesses: Low debt, high returns on equity, and good past performance are fundamental to a strong business. Why not explore our interactive list of stocks with solid business fundamentals to see if there are other companies you may not have considered!

PS. Simply Wall St updates its DCF calculation for every American stock every day, so if you want to find the intrinsic value of any other stock, just search here.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Twitter might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NYSE:TWTR

Twitter, Inc. operates as a platform for public self-expression and conversation in real-time.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion