If you’re holding Snap (SNAP) or thinking about jumping in, the latest twist may have you pausing for a closer look. A shareholder class action lawsuit has just been filed, alleging Snap misled investors or withheld important information about how quickly its advertising revenue was really growing. Lawsuits like this can cast a shadow over a company’s financial and reputational standing, which is never something investors take lightly.

The lawsuit arrives at a time when Snap’s stock has already experienced some rough patches. Despite a flicker of growth over the past week, shares are down sharply this year and have struggled to regain momentum after larger declines earlier in the year. Add in the fact that Snap’s revenue is up for the year, but net income volatility and ongoing legal distractions remain, and it becomes apparent that the road ahead is not exactly straightforward.

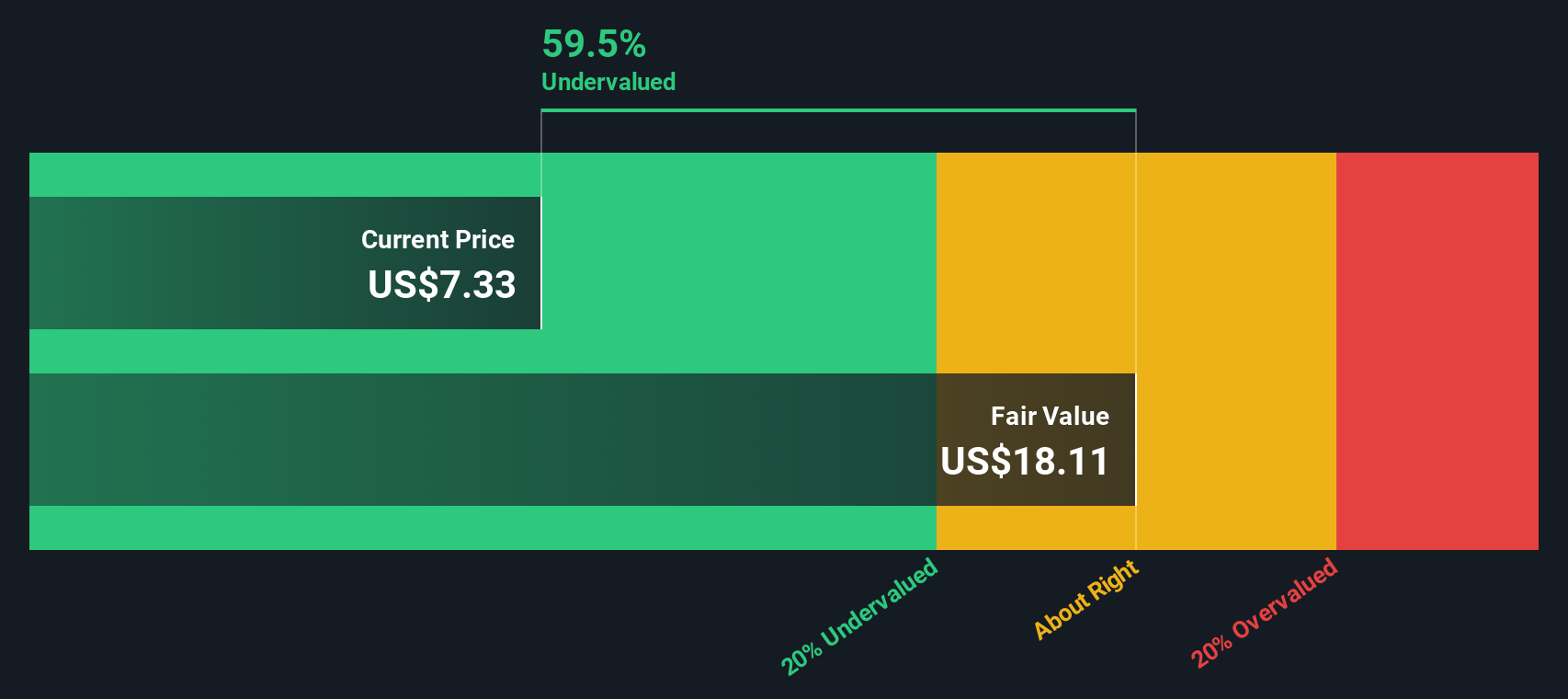

With all this swirling around, the real question is whether Snap’s current share price reflects all the risks or if there’s a chance the stock is now trading at a discount to its underlying potential.

Advertisement

Most Popular Narrative: 23.5% Undervalued

According to the community narrative, Snap is currently trading below its calculated fair value. This suggests the potential for significant upside if certain growth assumptions are met.

Accelerating innovation in augmented reality (AR), including the upcoming public launch of Specs AR glasses in 2026 and ongoing expansion of the AR developer ecosystem, positions Snap to benefit from increased user engagement. This also supports the creation of premium advertising and subscription revenue streams, which can boost top-line revenue and improve gross margins over time.

Curious why analysts are so bullish, even as Snap’s profitability remains elusive? This narrative highlights possible major transformations and sets the stage for some ambitious projections on revenue growth, margin potential, and long-term valuation. Interested in what kind of future Snap is pricing in? Read on for the bold assumptions behind this enticing valuation.

However, persistent losses and growing competition from social media giants remain significant risks. These factors could threaten Snap’s valuation story.

Another View: SWS DCF Model Tells a Different Story

While valuation based on sales multiples points toward Snap being undervalued, our DCF model takes expected future cash flows into account and presents a different perspective. Does Snap's long-term potential live up to the optimism, or are risks being underestimated?

Don’t miss out on fresh opportunities that could give your portfolio an edge. Simply Wall Street’s tailored screeners help you spot unique investment angles and filter the market in minutes. Take the guesswork out and get inspired with these smart places to look next:

Kickstart your search for high-potential value plays by zeroing in on undervalued stocks based on cash flows, which might be trading for less than their true worth.

Capitalize on global breakthroughs by browsing quantum computing stocks, which are at the forefront of innovation in computing and tomorrow’s tech.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.