- United States

- /

- Entertainment

- /

- NYSE:SE

3 US Growth Companies With High Insider Ownership Growing Revenues At 42%

Reviewed by Simply Wall St

In a market environment where major U.S. indices have recently faced downturns amid concerns over economic health and high-profile tech stock declines, investors are increasingly looking for resilient opportunities. One promising avenue is growth companies with high insider ownership, which often signals confidence from those closest to the business and can be particularly compelling when these firms are also demonstrating strong revenue growth.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 23.2% |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.1% |

| GigaCloud Technology (NasdaqGM:GCT) | 25.7% | 24.3% |

| Victory Capital Holdings (NasdaqGS:VCTR) | 10.2% | 32.3% |

| Hims & Hers Health (NYSE:HIMS) | 13.7% | 40.7% |

| On Holding (NYSE:ONON) | 28.4% | 24.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.1% | 60.9% |

| Carlyle Group (NasdaqGS:CG) | 29.5% | 22% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 78.8% |

| BBB Foods (NYSE:TBBB) | 22.9% | 66.5% |

Here we highlight a subset of our preferred stocks from the screener.

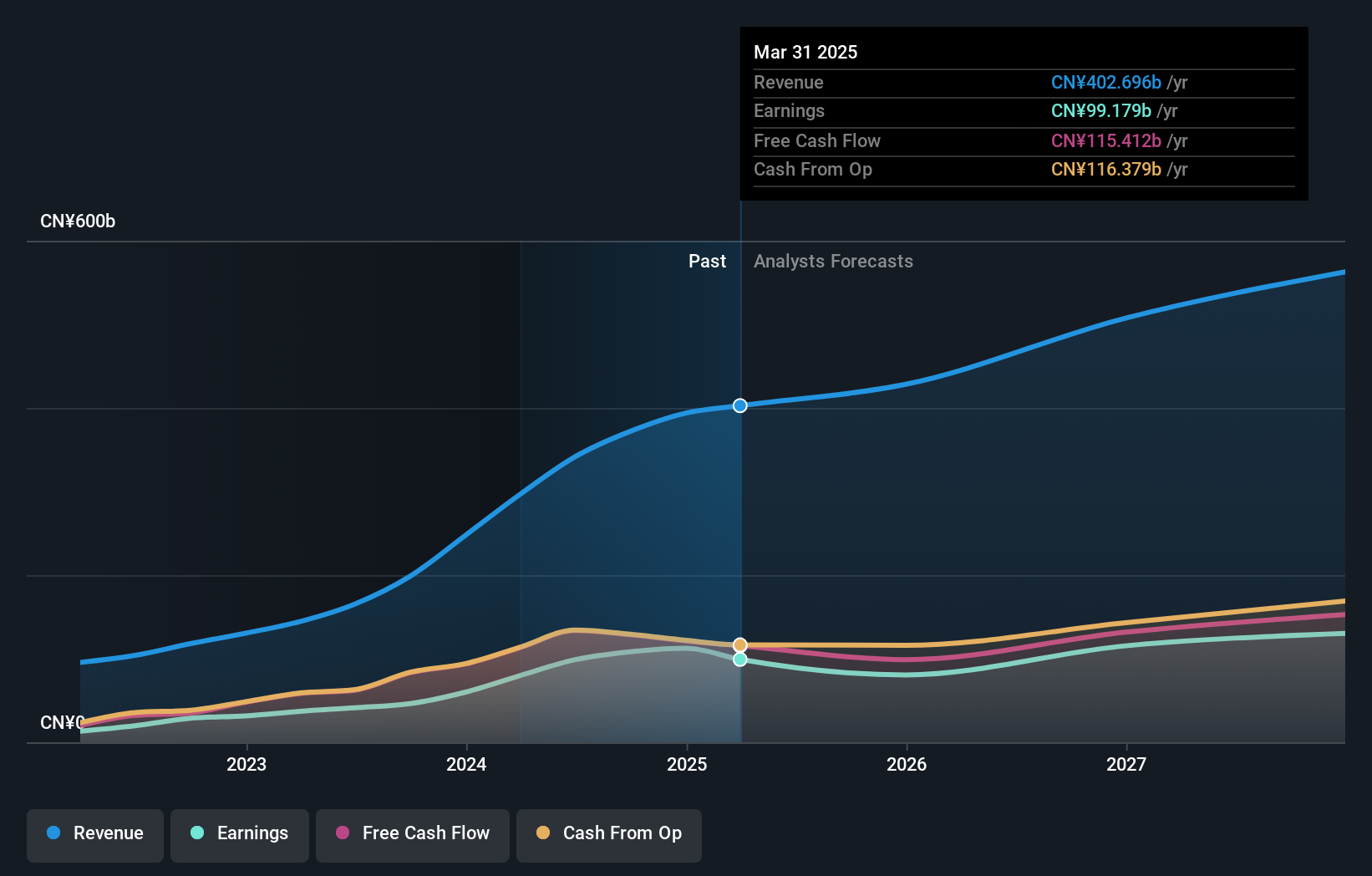

PDD Holdings (NasdaqGS:PDD)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PDD Holdings Inc., a multinational commerce group with a market cap of approximately $133.47 billion, owns and operates a diverse portfolio of businesses.

Operations: The company's revenue segment includes Internet Software & Services, generating CN¥341.59 billion.

Insider Ownership: 32.1%

Revenue Growth Forecast: 19.1% p.a.

PDD Holdings has demonstrated substantial growth, with Q2 2024 sales reaching CNY 97.06 billion and net income at CNY 32.01 billion, both significantly higher than a year ago. Despite legal challenges regarding alleged misleading statements and user privacy issues, the company is forecasted to grow earnings by 18.18% annually and revenue by 19.1% per year, outpacing the US market average. High insider ownership aligns management interests with shareholders, although past shareholder dilution is a concern.

- Dive into the specifics of PDD Holdings here with our thorough growth forecast report.

- Our expertly prepared valuation report PDD Holdings implies its share price may be lower than expected.

Sea (NYSE:SE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Sea Limited operates in digital entertainment, e-commerce, and digital financial services across Southeast Asia, Latin America, the rest of Asia, and internationally with a market cap of $44.98 billion.

Operations: Sea Limited generates revenue through three main segments: digital entertainment, e-commerce, and digital financial services across Southeast Asia, Latin America, the rest of Asia, and internationally.

Insider Ownership: 15.1%

Revenue Growth Forecast: 12.5% p.a.

Sea Limited, a growth company with high insider ownership, recently reported Q2 2024 revenue of US$3.81 billion and net income of US$79.91 million, though both figures were lower than the previous year. The company is forecasted to become profitable within three years and grow earnings by 49.4% annually, outpacing the market. Recent board changes include adding independent directors Dr. Silvio Savarese and Ms. Jessica Tan, enhancing governance as Sea continues its expansion trajectory.

- Click here and access our complete growth analysis report to understand the dynamics of Sea.

- Our comprehensive valuation report raises the possibility that Sea is priced lower than what may be justified by its financials.

Sable Offshore (NYSE:SOC)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Sable Offshore Corp. engages in oil and gas exploration and development activities in the United States, with a market cap of approximately $1.09 billion.

Operations: The company's revenue segments include oil exploration ($550 million) and gas development ($450 million).

Insider Ownership: 26.9%

Revenue Growth Forecast: 42.2% p.a.

Sable Offshore Corp. is forecast to grow revenue by 42.2% annually, significantly outpacing the US market's 8.7%. Despite recent high volatility and substantial insider selling, insiders have also bought more shares in the past three months. The company reported a net loss of US$165.44 million for Q2 2024, up from US$22.31 million a year ago, but is expected to become profitable within three years with earnings projected to grow by 95.13% annually.

- Delve into the full analysis future growth report here for a deeper understanding of Sable Offshore.

- In light of our recent valuation report, it seems possible that Sable Offshore is trading behind its estimated value.

Turning Ideas Into Actions

- Delve into our full catalog of 181 Fast Growing US Companies With High Insider Ownership here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SE

Sea

Engages in the digital entertainment, e-commerce, and digital financial service businesses in Southeast Asia, Latin America, rest of Asia, and internationally.

Excellent balance sheet and good value.