- United States

- /

- Entertainment

- /

- NasdaqGS:WMG

Warner Music Group (NASDAQ:WMG) Will Pay A Larger Dividend Than Last Year At $0.16

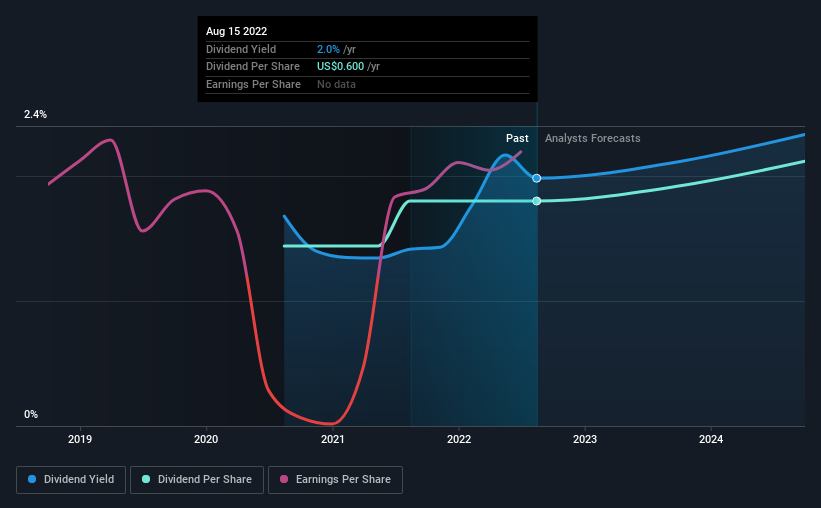

Warner Music Group Corp.'s (NASDAQ:WMG) periodic dividend will be increasing on the 1st of September to $0.16, with investors receiving 6.7% more than last year's $0.15. This will take the dividend yield to an attractive 2.0%, providing a nice boost to shareholder returns.

Check out our latest analysis for Warner Music Group

Warner Music Group's Payment Has Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Before making this announcement, Warner Music Group was paying out quite a large proportion of both earnings and cash flow, with the dividend being 133% of cash flows. Paying out such a high proportion of cash flows can expose the business to needing to cut the dividend if the business runs into some challenges.

Looking forward, earnings per share is forecast to rise by 87.8% over the next year. If the dividend continues on this path, the payout ratio could be 61% by next year, which we think can be pretty sustainable going forward.

Warner Music Group Doesn't Have A Long Payment History

The company has maintained a consistent dividend for a few years now, but we would like to see a longer track record before relying on it. Since 2020, the annual payment back then was $0.48, compared to the most recent full-year payment of $0.60. This works out to be a compound annual growth rate (CAGR) of approximately 12% a year over that time. Warner Music Group has been growing its dividend quite rapidly, which is exciting. However, the short payment history makes us question whether this performance will persist across a full market cycle.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. It's encouraging to see that Warner Music Group has been growing its earnings per share at 40% a year over the past three years. EPS is growing rapidly, although the company is also paying out a large portion of its profits as dividends. If earnings keep growing, the dividend may be sustainable, but generally we'd prefer to see a fast growing company reinvest in further growth.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. While Warner Music Group is earning enough to cover the payments, the cash flows are lacking. We don't think Warner Music Group is a great stock to add to your portfolio if income is your focus.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Case in point: We've spotted 2 warning signs for Warner Music Group (of which 1 is potentially serious!) you should know about. Is Warner Music Group not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

If you're looking to trade Warner Music Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Warner Music Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:WMG

Warner Music Group

Operates as a music entertainment company in the United States, the United Kingdom, Germany, and internationally.

Moderate growth potential with mediocre balance sheet.

Market Insights

Community Narratives