- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:TZOO

Travelzoo (NasdaqGS:TZOO) Shares Drop 20% Following Q4 Earnings Report With Sales At US$21 Million

Reviewed by Simply Wall St

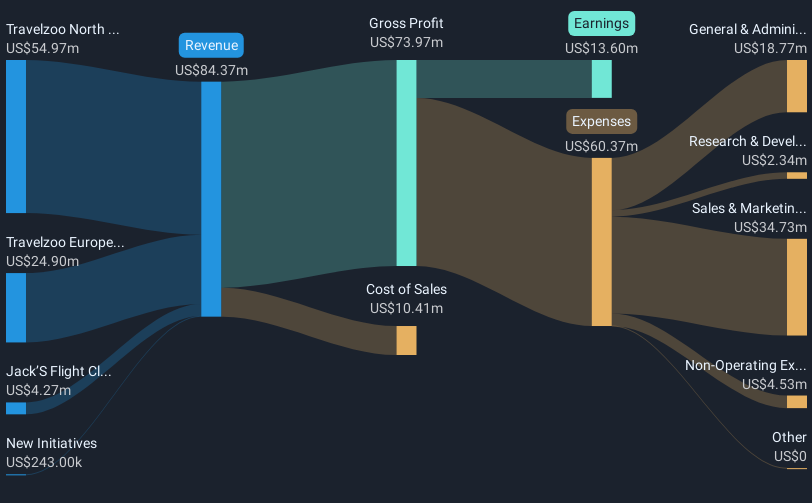

Travelzoo (NasdaqGS:TZOO) experienced a 20% decline last month, a significant move that coincided with several notable events. Travelzoo's Q4 2024 earnings report showed decreased sales at $20.68 million from $21.15 million the previous year, though EPS did rise slightly. The company's recent announcement to continue revenue growth through enhanced membership models may not have been enough to offset concerns. The completion of a share buyback program was announced, but market sentiment may have been affected by mixed broader market performance. The tech-heavy Nasdaq, where the company is listed, recorded declines amid investor concerns over economic policy and tech sector weakness. The overall market dropped 4% last month, which likely amplified Travelzoo’s price slide. Investor worries about potential tariff impacts and broader economic health added pressure across sectors, influencing Travelzoo’s recent market valuation adjustments despite its efforts to bolster long-term growth via membership strategies.

Take a closer look at Travelzoo's potential here.

Travelzoo's total return of 74.69% over the past five years highlights its strong long-term performance. During this period, the company benefited from a series of strategies and market conditions that contributed to this growth. A standout factor has been its substantial earnings growth, with the company's profits increasing significantly, averaging over 45% yearly. Additionally, Travelzoo's return on equity is considered very large, which speaks to effective capital utilization and profitability.

Another critical aspect in Travelzoo's five-year journey has been its value positioning, trading at a notably lower Price-To-Earnings Ratio compared to both its industry and peers. Such positioning likely attracted value-focused investors. The completion of various stock buyback programs, including the most recent in February 2025, illustrates the company's commitment to shareholder value, albeit without dividend payouts. Furthermore, the company's forecasted revenue and earnings growth rates are expected to surpass broader market averages, positioning Travelzoo for continued competitive performance.

- See how Travelzoo measures up with our analysis of its intrinsic value versus market price.

- Assess the downside scenarios for Travelzoo with our risk evaluation.

- Is Travelzoo part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Travelzoo, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Travelzoo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TZOO

Travelzoo

Operates as an Internet media company that provides travel, entertainment, and local experiences worldwide.

Undervalued with solid track record.

Similar Companies

Market Insights

Community Narratives