Advertisement

- United States

- /

- Media

- /

- NasdaqCM:THRY

Thryv Holdings, Inc. Just Missed Earnings - But Analysts Have Updated Their Models

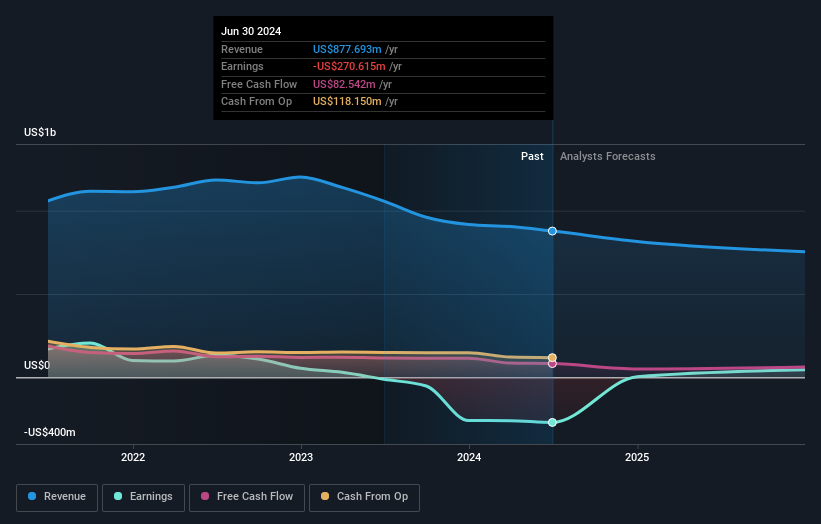

Shareholders might have noticed that Thryv Holdings, Inc. (NASDAQ:THRY) filed its second-quarter result this time last week. The early response was not positive, with shares down 7.0% to US$18.13 in the past week. It looks like a pretty bad result, all things considered. Although revenues of US$224m were in line with analyst predictions, statutory earnings fell badly short, missing estimates by 67% to hit US$0.15 per share. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

See our latest analysis for Thryv Holdings

After the latest results, the consensus from Thryv Holdings' five analysts is for revenues of US$815.4m in 2024, which would reflect a noticeable 7.1% decline in revenue compared to the last year of performance. Thryv Holdings is also expected to turn profitable, with statutory earnings of US$0.29 per share. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$818.5m and earnings per share (EPS) of US$0.62 in 2024. The analysts seem to have become more bearish following the latest results. While there were no changes to revenue forecasts, there was a large cut to EPS estimates.

It might be a surprise to learn that the consensus price target fell 9.9% to US$29.50, with the analysts clearly linking lower forecast earnings to the performance of the stock price. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Thryv Holdings, with the most bullish analyst valuing it at US$36.00 and the most bearish at US$25.00 per share. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Of course, another way to look at these forecasts is to place them into context against the industry itself. Over the past five years, revenues have declined around 9.0% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for an annualised 14% decline in revenue until the end of 2024. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 3.2% per year. So while a broad number of companies are forecast to grow, unfortunately Thryv Holdings is expected to see its revenue affected worse than other companies in the industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Thryv Holdings. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Thryv Holdings analysts - going out to 2025, and you can see them free on our platform here.

Before you take the next step you should know about the 1 warning sign for Thryv Holdings that we have uncovered.

Valuation is complex, but we're here to simplify it.

Discover if Thryv Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:THRY

Thryv Holdings

Provides digital marketing solutions and cloud-based tools to the small-to-medium-sized businesses in the United States.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets