Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:LDI

US Growth Companies With High Insider Ownership In October 2024

Simply Wall St

Reviewed by Simply Wall St

As of late October 2024, U.S. stock markets have shown a mixed performance with the S&P 500 and Nasdaq gaining ground, while the Dow Jones Industrial Average has experienced a four-day losing streak amid varied corporate earnings reports. In this fluctuating environment, growth companies with high insider ownership can be appealing to investors as they often indicate strong confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| GigaCloud Technology (NasdaqGM:GCT) | 25.6% | 26% |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 23.4% |

| Victory Capital Holdings (NasdaqGS:VCTR) | 10.2% | 33.3% |

| Super Micro Computer (NasdaqGS:SMCI) | 25.7% | 28.7% |

| Hims & Hers Health (NYSE:HIMS) | 13.7% | 37.4% |

| Bridge Investment Group Holdings (NYSE:BRDG) | 11.3% | 102.3% |

| Coastal Financial (NasdaqGS:CCB) | 18.4% | 40.4% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| BBB Foods (NYSE:TBBB) | 22.9% | 51.2% |

Below we spotlight a couple of our favorites from our exclusive screener.

Bridgewater Bancshares (NasdaqCM:BWB)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Bridgewater Bancshares, Inc. is the bank holding company for Bridgewater Bank, offering banking products and services to commercial real estate investors, entrepreneurs, business clients, and individuals in the United States with a market cap of $416.60 million.

Operations: Revenue segments for the bank include various banking products and services tailored to commercial real estate investors, entrepreneurs, business clients, and individuals in the United States.

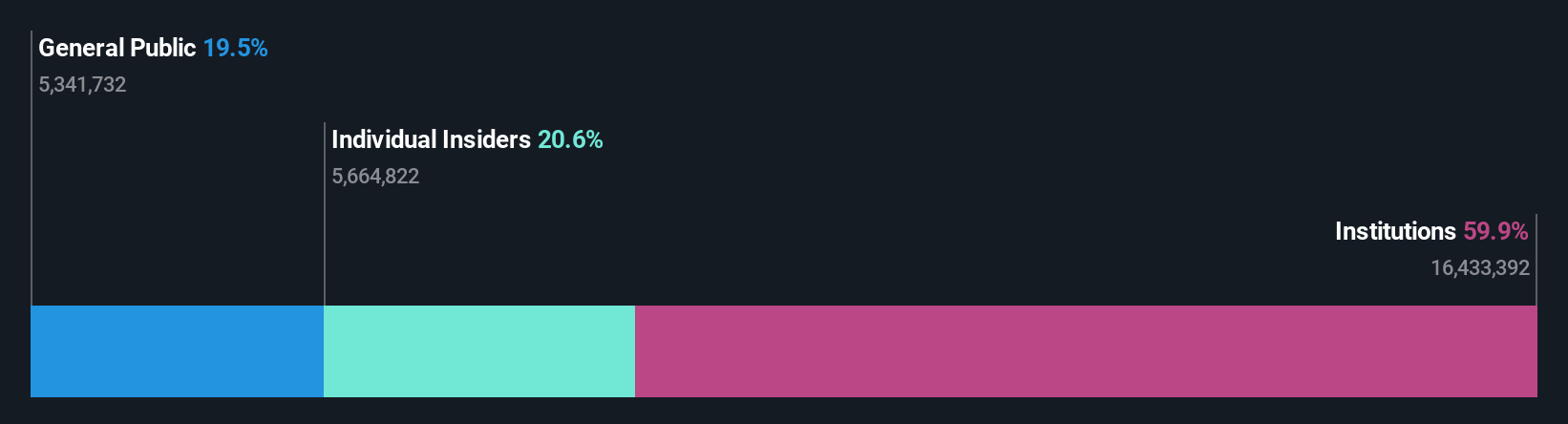

Insider Ownership: 20.6%

Revenue Growth Forecast: 10.3% p.a.

Bridgewater Bancshares demonstrates a mixed outlook as a growth company with high insider ownership. Recent earnings show a decline in net income and EPS compared to the previous year, but future earnings are forecasted to grow significantly at 21.3% annually, outpacing the US market. Revenue is also expected to rise faster than the market average. Despite no substantial insider buying recently, more shares have been bought than sold by insiders over three months.

- Get an in-depth perspective on Bridgewater Bancshares' performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Bridgewater Bancshares' share price might be on the cheaper side.

Taboola.com (NasdaqGS:TBLA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Taboola.com Ltd. operates an artificial intelligence-based algorithmic engine platform across various countries including Israel, the United States, the United Kingdom, and Germany, with a market cap of approximately $1.23 billion.

Operations: The company generates revenue primarily from its advertising segment, amounting to $1.62 billion.

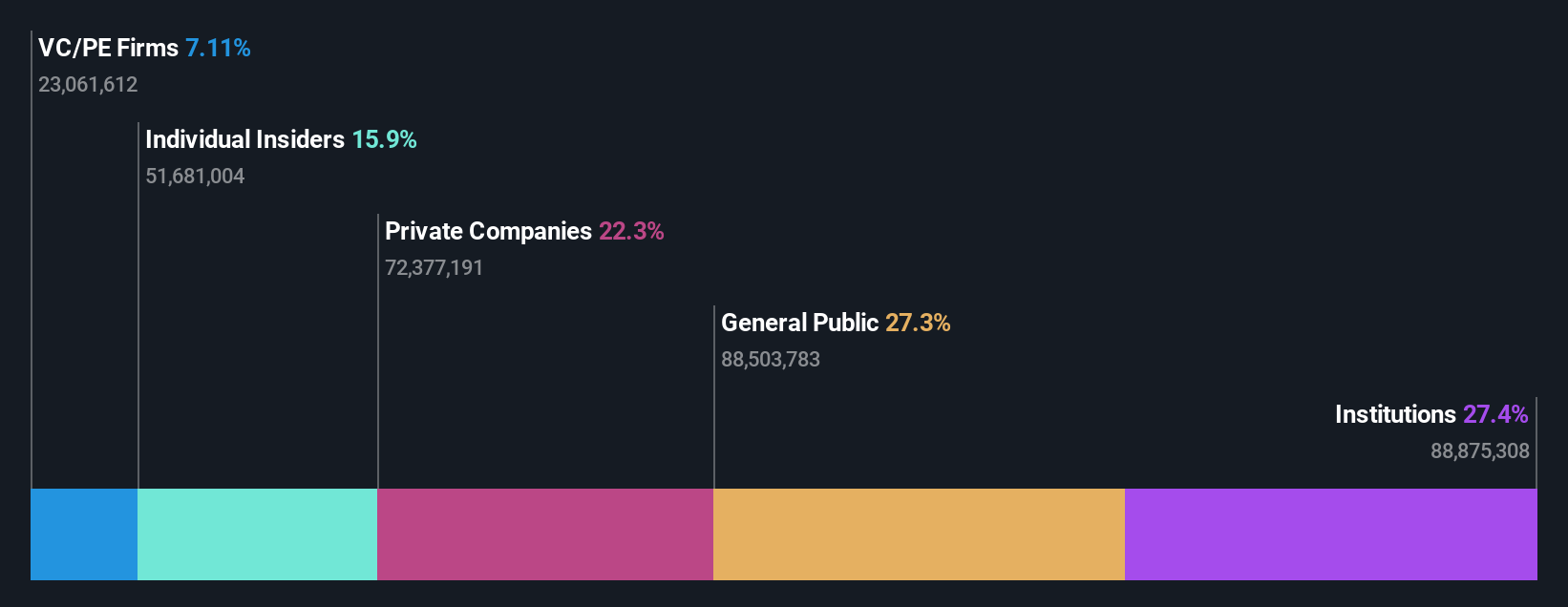

Insider Ownership: 13.3%

Revenue Growth Forecast: 14.0% p.a.

Taboola.com is poised for growth with a forecasted annual earnings increase of 59.5%, surpassing market averages. Despite recent insider selling, the stock trades at a significant discount to its estimated fair value. Recent product innovations like Abby, an AI-driven campaign assistant, and Maximize Conversions technology are driving advertiser engagement and efficiency gains. The company reported Q2 sales of US$428.16 million, reducing net losses considerably from the previous year while executing substantial share buybacks.

- Navigate through the intricacies of Taboola.com with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility Taboola.com's shares may be trading at a discount.

loanDepot (NYSE:LDI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: loanDepot, Inc. operates in the United States by originating, financing, selling, and servicing residential mortgage loans with a market cap of approximately $688.72 million.

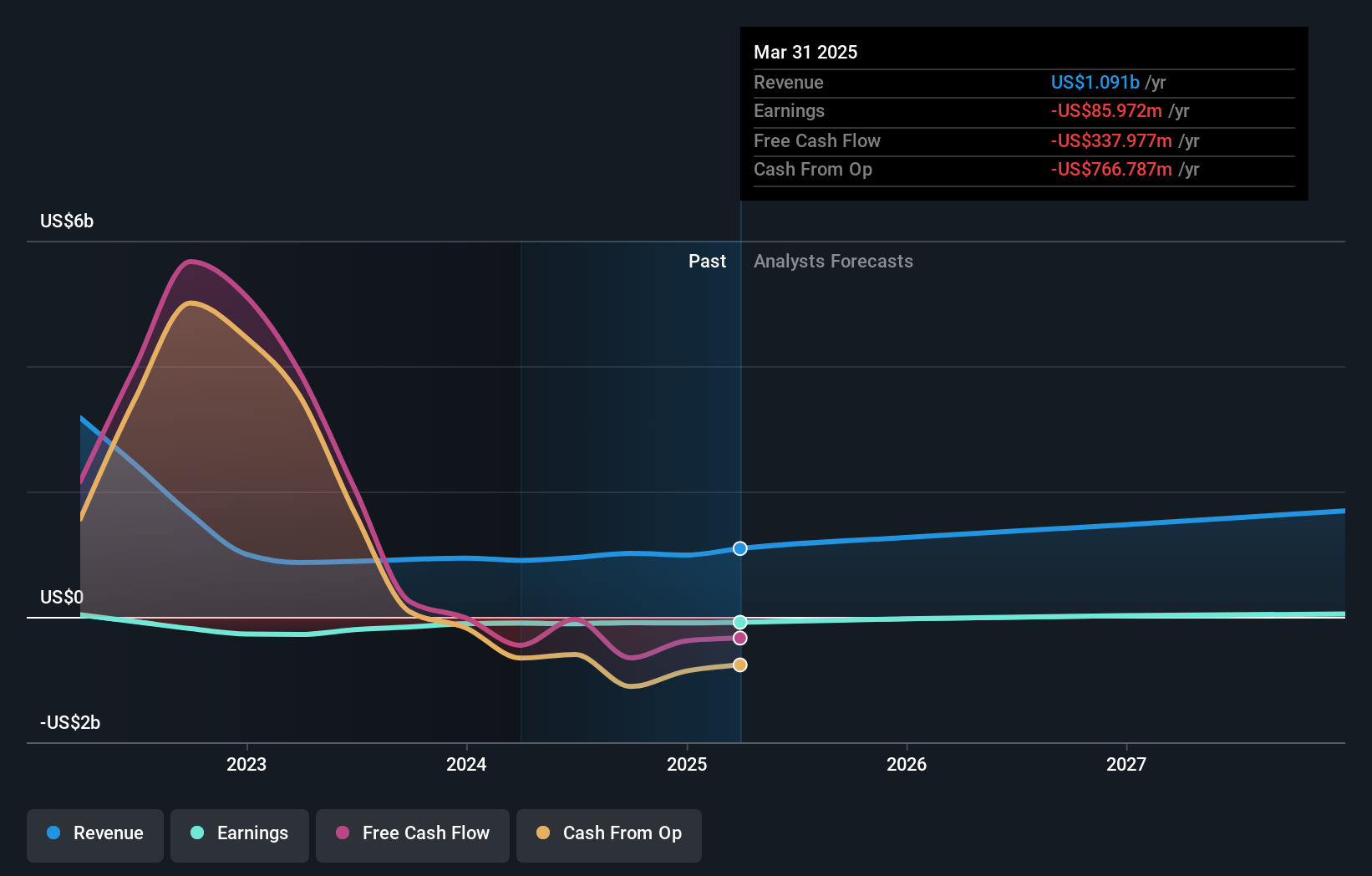

Operations: The company's revenue segment primarily consists of originating, financing, and selling mortgage loans, generating $911.64 million.

Insider Ownership: 11.8%

Revenue Growth Forecast: 18.8% p.a.

loanDepot's revenue is projected to grow at 18.8% annually, outpacing the broader US market, and it is expected to achieve profitability within three years. Despite recent share dilution and significant insider selling, the company has secured a revolving line of credit with Flagstar Bank and expanded its product suite with a first-lien HELOC. Recent earnings showed a net loss increase but stable revenue compared to last year, reflecting ongoing financial challenges amidst strategic growth initiatives.

- Take a closer look at loanDepot's potential here in our earnings growth report.

- Our expertly prepared valuation report loanDepot implies its share price may be lower than expected.

Next Steps

- Discover the full array of 184 Fast Growing US Companies With High Insider Ownership right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if loanDepot might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LDI

loanDepot

Engages in originating, financing, selling, and servicing residential mortgage loans in the United States.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|12.7% undervalued

MA

Community Contributor