- United States

- /

- Entertainment

- /

- NasdaqGS:ROKU

Continued Volatility may Give Investors an Opportunity to Invest in Roku (NASDAQ:ROKU) at a Great Price

Roku’s (NASDAQ:ROKU) share price has continued to slide despite the company delivering record earnings earlier this month. We recently suggested that Roku’s share price may be in for continued volatility as the market continues to focus on top line growth. This opinion has been supported by the fact that the stock has continued to trade lower after reporting a very impressive set of results.

Highlights from the second quarter results included:

- Year-on-year revenue growth of 81%.

- Year-on-year platform revenue growth of 117%.

- Sequential active accounts growth of 2.7%.

- Average revenue per user up 46% year-on-year.

The only negative in terms of numbers was the fact that the total number of hours watched was lower than the first quarter. This isn’t surprising as the US economy did begin to open up in the second quarter, meaning consumers spent less time at home. However, it is an issue for Roku, as the company earns a significant share of its revenue from advertising, which is related to viewing hours.

Another headwind that Roku is beginning to face is competition. TCL Technology, a long-standing partner of Roku recently announced a new range of Google TVs. This will make it easier for Google to compete with Roku as an operating system, and in delivering ad supported content to consumers.

Roku’s third headwind is the chip shortage and other supply chain issues that are impacting the company’s margins. The higher input costs may ultimately affect sales too.

While Roku is facing several challenges, the company’s underlying fundamentals continue to improve. This can be illustrated by examining Roku’s ROCE (Return on Capital Employed).

Return On Capital Employed (ROCE): What is it?

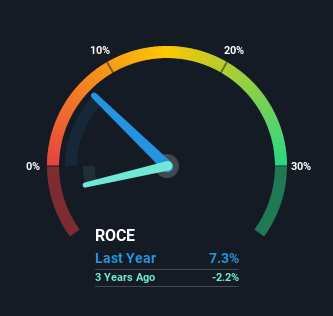

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Roku:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.073 = US$222m ÷ (US$3.6b - US$611m) (Based on the trailing twelve months to June 2021).

Therefore, Roku has an ROCE of 7.3%. Even though it's in line with the industry average of 7.3%, it's still a low return by itself.

See our latest analysis for Roku

NasdaqGS:ROKU Return on Capital Employed August 18th 2021

In the above chart we have measured Roku's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Roku.

What Can We Tell from Roku's ROCE Trend?

The fact that Roku is now generating some pre-tax profits from its prior investments is very encouraging. Shareholders would no doubt be pleased with this because the business was loss-making five years ago but it is now generating 7.3% on its capital. In addition to that, Roku is employing 3,635% more capital than previously which is expected of a company that's trying to break into profitability. We like this trend, because it tells us the company has profitable reinvestment opportunities available to it, and if it continues going forward that can lead to a multi-bagger performance.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 17%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. Therefore, we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books.

The Bottom Line on Roku's ROCE

In summary, it's great to see that Roku has managed to break into profitability and is continuing to reinvest in its business. Since the stock has returned a staggering 508% to shareholders over the last three years, it looks like investors are recognizing these changes. Therefore, we think it would be worth your time to check if these trends are going to continue.

Roku is well positioned within the streaming video space. It doesn’t compete with the likes of Netflix and Disney, but acts as a platform for multiple streaming channels. In addition, Roku’s own ad supported channel is one of very few alternatives for advertisers wanting exposure to audiences who have moved away from cable TV.

The current headwinds are likely to lead to continued volatility for Roku’s share price. But this may give investors an opportunity to invest in a high-quality business at an attractive price. You can keep an eye on Roku’s valuation and growth forecasts here..

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.

About NasdaqGS:ROKU

Roku

Operates a TV streaming platform in the United states and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives