Advertisement

- United States

- /

- Entertainment

- /

- NasdaqCM:RDI

What Can We Make Of Reading International's (NASDAQ:RDI) CEO Compensation?

This article will reflect on the compensation paid to Ellen Cotter who has served as CEO of Reading International, Inc. (NASDAQ:RDI) since 2015. This analysis will also assess whether Reading International pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

Check out our latest analysis for Reading International

Comparing Reading International, Inc.'s CEO Compensation With the industry

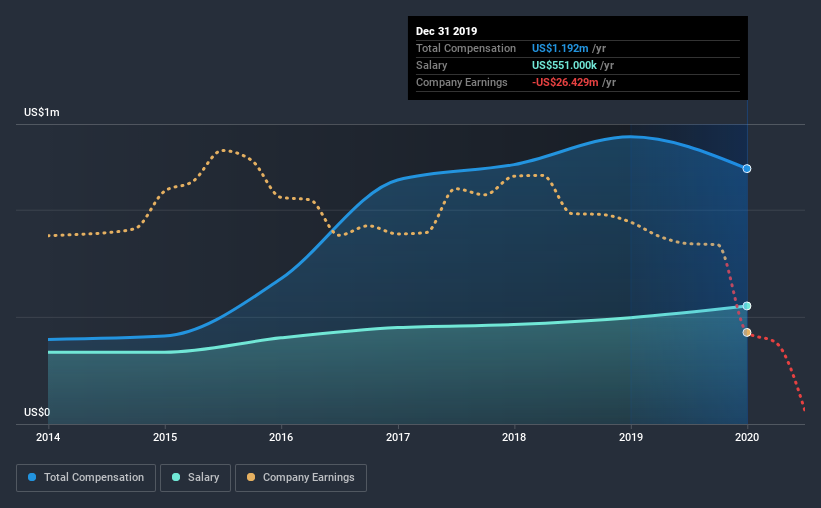

At the time of writing, our data shows that Reading International, Inc. has a market capitalization of US$118m, and reported total annual CEO compensation of US$1.2m for the year to December 2019. That's a notable decrease of 11% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at US$551k.

On comparing similar-sized companies in the industry with market capitalizations below US$200m, we found that the median total CEO compensation was US$320k. Accordingly, our analysis reveals that Reading International, Inc. pays Ellen Cotter north of the industry median. Furthermore, Ellen Cotter directly owns US$3.5m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | US$551k | US$496k | 46% |

| Other | US$641k | US$844k | 54% |

| Total Compensation | US$1.2m | US$1.3m | 100% |

Speaking on an industry level, nearly 21% of total compensation represents salary, while the remainder of 79% is other remuneration. It's interesting to note that Reading International pays out a greater portion of remuneration through salary, compared to the industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Reading International, Inc.'s Growth Numbers

Over the last three years, Reading International, Inc. has shrunk its earnings per share by 107% per year. In the last year, its revenue is down 33%.

The decline in EPS is a bit concerning. And the impression is worse when you consider revenue is down year-on-year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Reading International, Inc. Been A Good Investment?

With a three year total loss of 73% for the shareholders, Reading International, Inc. would certainly have some dissatisfied shareholders. So shareholders would probably want the company to be lessto generous with CEO compensation.

To Conclude...

As we noted earlier, Reading International pays its CEO higher than the norm for similar-sized companies belonging to the same industry. This doesn't look good against shareholder returns, which have been negative for the past three years. Add to that declining EPS growth, and you have the perfect recipe for shareholder irritation. Overall, with such poor performance, shareholder's would probably have questions if the company decided to give the CEO a raise.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 1 warning sign for Reading International that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you decide to trade Reading International, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqCM:RDI

Reading International

Focuses on the ownership, development, and operation of entertainment and real property assets in the United States, Australia, and New Zealand.

Slight and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor