Advertisement

- United States

- /

- Media

- /

- NasdaqGS:ECHO

EchoStar (ECHO) On Chapter 11 Filing Has Fair Value Back In Focus

EchoStar (ECHO) is back in focus after its Dish DBS and wireless subsidiaries filed for prepackaged Chapter 11 bankruptcy protection, following a delayed spectrum license sale to AT&T that highlights complex restructuring and financing pressures.

See our latest analysis for EchoStar.

The share price reaction around the Chapter 11 news has been negative in the short term, with EchoStar’s 1 month share price return down 15.8% and 3 month share price return down 20.3%. Its 1 year total shareholder return is 199.8%, suggesting strong longer term momentum that is now being tested as investors reassess the balance between past gains and current restructuring risks.

If this kind of restructuring story has your attention, it could be a good moment to broaden your search and uncover 19 top founder-led companies

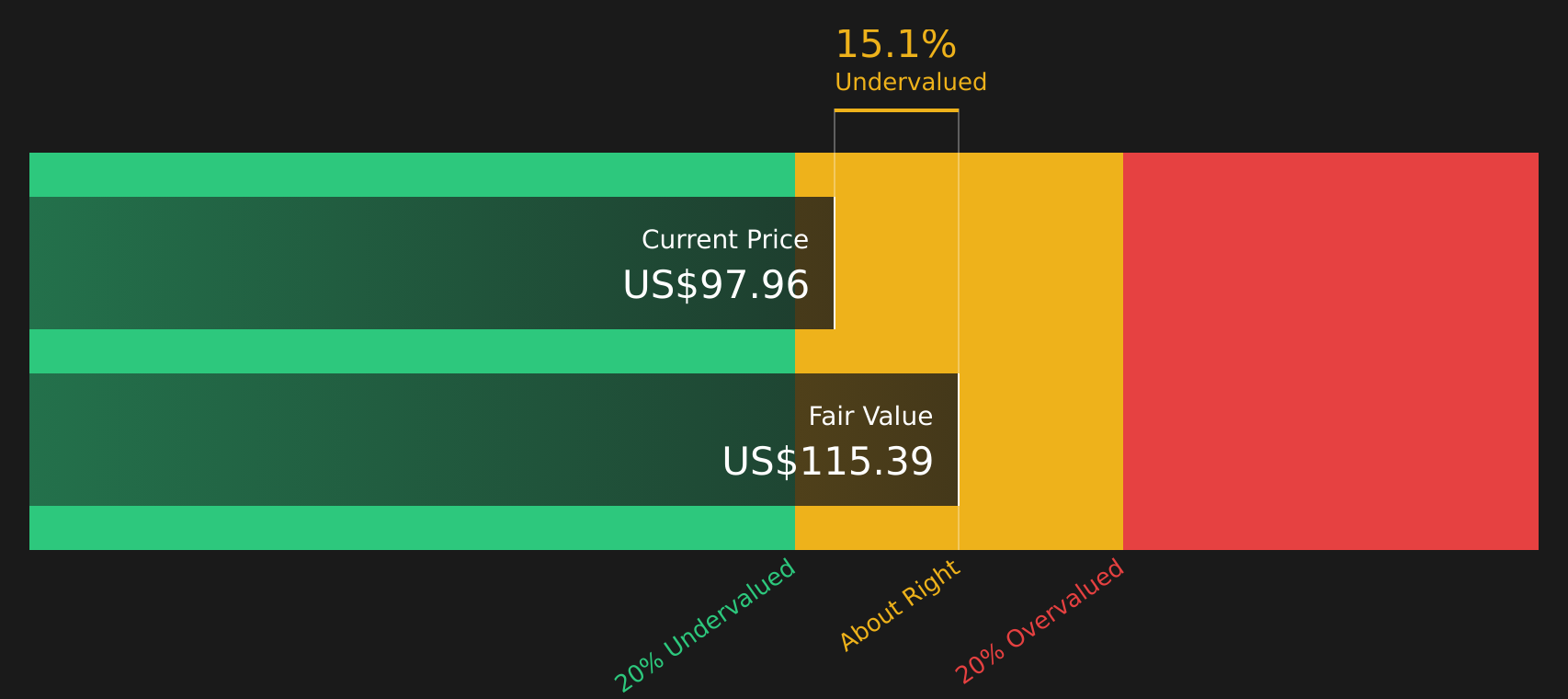

EchoStar now trades at US$97.91 compared with analyst targets around US$141 and one intrinsic value estimate that sits materially lower. This raises a simple question: where does fair value really sit after the Chapter 11 shock?

Most Popular Narrative: 123% Overvalued

EchoStar’s last close at $97.91 sits well above the narrative fair value of $43.91. This frames the current Chapter 11 reaction against a much lower anchor.

What I love about the EchoStar story is how fast a narrative can flip. For years, it was a "has-been." But with one bold management call, they teleported themselves into the center of the most exciting tech ecosystem of the decade.

Want to see how this bold pivot justifies such a low fair value? The narrative leans heavily on shrinking revenue, thin margins and an earnings trajectory that has to work hard to get back to profitability. Curious which assumptions really compress that valuation and how they treat future cash generation across EchoStar’s segments?

Result: Fair Value of $43.91 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, EchoStar’s loss of US$14,441.396 and revenue that declined 2.8% each year, along with Chapter 11 complexity, could still pull this narrative off course.

Find out about the key risks to this EchoStar narrative.

Another View: DCF Puts EchoStar Below Fair Value

The user narrative frames EchoStar as 123% overvalued at $97.91 versus a $43.91 fair value, but the SWS DCF model tells a different story. In this view, EchoStar trades at a 15.5% discount to an estimated future cash flow value of $115.82, suggesting the market could be underpricing its ability to repair losses and reach profitability. Which story do you think the market will lean toward as the Chapter 11 process unfolds?

For readers who want to see exactly how that future cash flow estimate is built line by line, it is worth reviewing how the SWS DCF model treats EchoStar’s current losses, expected earnings growth and forecast revenue decline, all in one place, in Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out EchoStar for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on EchoStar split between caution and optimism, this is a good time to act quickly, review the underlying numbers yourself, and weigh the company’s potential 3 key rewards

Looking for more investment ideas beyond EchoStar?

If the EchoStar story has sharpened your focus, do not stop here; broaden your watchlist now or you risk missing other opportunities emerging in plain sight.

- Target long term compounding potential by scanning 45 high quality undervalued stocks that combine stronger fundamentals with more appealing price tags.

- Strengthen the income side of your portfolio by reviewing 9 dividend fortresses that aim to deliver higher yields with staying power.

- Prioritise resilience by focusing on 74 resilient stocks with low risk scores that show healthier risk profiles than the broader market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EchoStar might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ECHO

EchoStar

Provides pay-tv services in the United States, Mexico, Canada, South and Central America, Asia, Africa, Australia, Europe, India, and the Middle East.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1941.1% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

45 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.5% undervalued

15 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30154.5% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

DA

danmad on Cobram Estate Olives ·

More than just olive oil on the shelf

Fair Value:AU$3.64.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Verisk Analytics ·

VRSK 05-2026

Fair Value:US$76.85149.8% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

45 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.6% undervalued

90 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5455.7% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3455.9% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

1

|0