- United States

- /

- Media

- /

- NasdaqGS:CMCSA

Comcast (NasdaqGS:CMCSA) Declares Quarterly Dividend Of US$0.33

Reviewed by Simply Wall St

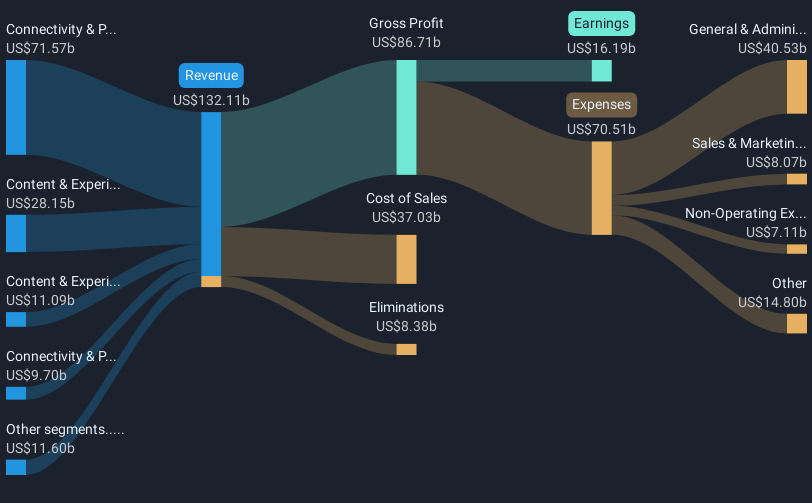

Comcast (NasdaqGS:CMCSA) recently announced a decrease in its quarterly cash dividend to $0.33 per share. This decision came amid a 4.65% rise in the company's share price over the last month. Against this backdrop, Comcast's price move aligned with broader market trends, as the Nasdaq Composite added 0.3% despite declines in other indices. Additional developments such as Comcast's business expansions in Connecticut and share buybacks provided context for investor interest. Although market conditions fluctuated with factors like rising Treasury yields, Comcast's strategic initiatives may have added weight to the upward price movement.

Comcast's recent dividend cut to US$0.33 per share may signal cost management amid revenue pressures, as highlighted by the company's current challenges in broadband and wireless segments. Over the last five years, Comcast's total shareholder return, including share price appreciation and dividends, was 2.65%, reflecting modest growth compared to its short-term price gains. However, it underperformed the broader US market and the US Media industry over the past year, which saw returns of 11.1% and 1.3%, respectively.

The dividend reduction, coupled with competition concerns and travel-related risks impacting theme parks and media segments, paints a complicated picture for future revenue and earnings. Analysts expect annual earnings to decline by 2.5% over the next three years, which could be exacerbated by these factors. With a current price of US$34.49 and a bearish price target of US$30.00, the recent share price movement warrants caution, suggesting it remains slightly above some analyst valuations. This gap between the current price and the lowest analyst target signifies uncertainty in meeting bullish projections and investor confidence in strategic investments across Comcast's diverse segments.

Our valuation report here indicates Comcast may be undervalued.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CMCSA

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion