- United States

- /

- Hospitality

- /

- NasdaqGS:SABR

Undervalued Small Caps In United States With Insider Buying

Reviewed by Simply Wall St

Over the last 7 days, the market has risen 1.0%, driven by gains of 2.5% in one sector. The market is up 28% over the last 12 months, with earnings expected to grow by 15% per annum over the next few years. In this thriving environment, identifying undervalued small-cap stocks with insider buying can present unique opportunities for investors seeking growth potential at a reasonable price.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Columbus McKinnon | 19.6x | 0.9x | 45.87% | ★★★★★★ |

| Hanover Bancorp | 9.1x | 2.1x | 49.42% | ★★★★★☆ |

| Thryv Holdings | NA | 0.8x | 22.80% | ★★★★★☆ |

| MYR Group | 32.8x | 0.5x | 44.89% | ★★★★☆☆ |

| Franklin Financial Services | 10.3x | 2.0x | 37.09% | ★★★★☆☆ |

| Vital Energy | 4.2x | 0.6x | 5.98% | ★★★★☆☆ |

| German American Bancorp | 14.2x | 4.8x | 45.23% | ★★★☆☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

| Sabre | NA | 0.4x | -51.97% | ★★★☆☆☆ |

| Duluth Holdings | NA | 0.2x | -900387.72% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Advantage Solutions (NasdaqGS:ADV)

Simply Wall St Value Rating: ★★★★★☆

Overview: Advantage Solutions is a leading provider of outsourced sales and marketing services to consumer goods companies and retailers, with a market cap of approximately $1.43 billion.

Operations: Advantage Solutions generates revenue primarily through its services, with recent figures showing $4.07 billion in revenue as of June 2024. The gross profit margin has varied, reaching 13.95% in the same period while net income has shown fluctuations, recording a loss of $176.58 million. Operating expenses and non-operating expenses have also been significant factors impacting overall profitability.

PE: -7.1x

Advantage Solutions, a provider of sales and omnichannel marketing solutions, recently unveiled a new brand identity to reflect its transition into a unified retail solutions company. Despite reporting a net loss of US$100.84 million for Q2 2024 and facing significant impairment charges, the company has shown insider confidence with share repurchases totaling US$22.07 million between April and July 2024. Dropped from several Russell indexes in July 2024, Advantage continues to focus on driving demand and growth for brands and retailers through its streamlined operations.

- Delve into the full analysis valuation report here for a deeper understanding of Advantage Solutions.

Examine Advantage Solutions' past performance report to understand how it has performed in the past.

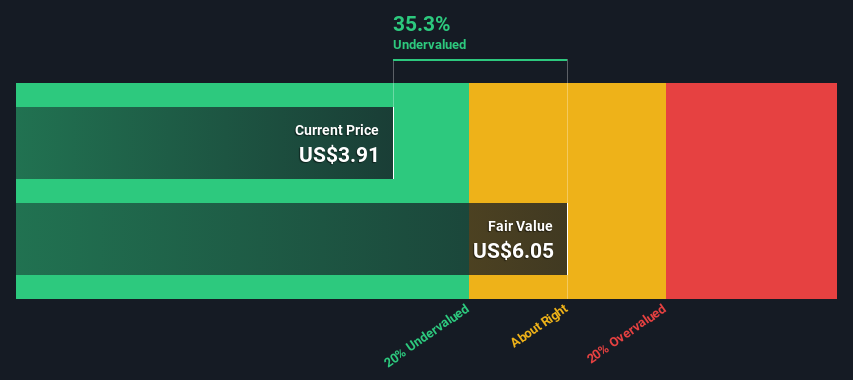

Sabre (NasdaqGS:SABR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Sabre is a technology solutions provider for the global travel and hospitality industries, with a market cap of approximately $1.66 billion.

Operations: The company generates revenue primarily from Travel Solutions ($2.70 billion) and Hospitality Solutions ($315.74 million). For the period ending 2024-06-30, it reported a gross profit margin of 59.47% with operating expenses amounting to $1.44 billion and R&D expenses at $882.44 million.

PE: -2.8x

Sabre Corporation, a tech provider in the travel industry, recently announced that Malaysia Airlines selected its PRISM tool to optimize corporate travel. Sabre's Q2 2024 earnings showed sales of US$767.24 million with a reduced net loss of US$69.76 million compared to the previous year. Despite executive changes and board reshuffling, insider confidence remains high with recent share purchases by key executives this year. The company’s expanding partnerships and innovative products suggest potential growth in an evolving market.

- Dive into the specifics of Sabre here with our thorough valuation report.

Review our historical performance report to gain insights into Sabre's's past performance.

Victoria's Secret (NYSE:VSCO)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Victoria's Secret operates as a specialty retailer of women's lingerie, intimate apparel, and beauty products with a market cap of approximately $2.56 billion.

Operations: The company generated $6.13 billion in revenue for the most recent period, with a gross profit margin of 44.67%. Operating expenses include significant allocations to sales and marketing ($454 million) and general & administrative expenses ($2.03 billion).

PE: 14.3x

Victoria's Secret, a smaller company in the US market, has shown signs of being undervalued. Recently, they reported second-quarter sales of US$1.42 billion and net income of US$31.8 million, a notable turnaround from last year's loss. Additionally, insider confidence is reflected through significant stock purchases by executives over the past few months. Leadership changes include appointing Hillary Super as CEO effective September 9, 2024, aiming to drive profitable growth with her extensive retail experience.

- Take a closer look at Victoria's Secret's potential here in our valuation report.

Evaluate Victoria's Secret's historical performance by accessing our past performance report.

Summing It All Up

- Reveal the 49 hidden gems among our Undervalued US Small Caps With Insider Buying screener with a single click here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SABR

Sabre

Operates as software and technology company for travel industry in the United States, Europe, Asia-Pacific, and internationally.

Fair value with moderate growth potential.