- United States

- /

- Chemicals

- /

- NYSE:WLK

Westlake (NYSE:WLK) Eyes Growth with Innovation in Polyethylene and Housing Market Opportunities

Reviewed by Simply Wall St

Westlake (NYSE:WLK) is leveraging its integrated manufacturing footprint in North America to drive efficiency and market penetration, as highlighted by recent developments in product innovation and sustainability. The company remains financially strong with strategic investments poised to capitalize on growth opportunities in the housing market. The accompanying report explores key areas such as financial health, competitive strategies, and potential market challenges impacting Westlake's future trajectory.

Click to explore a detailed breakdown of our findings on Westlake.

Key Assets Propelling Westlake Forward

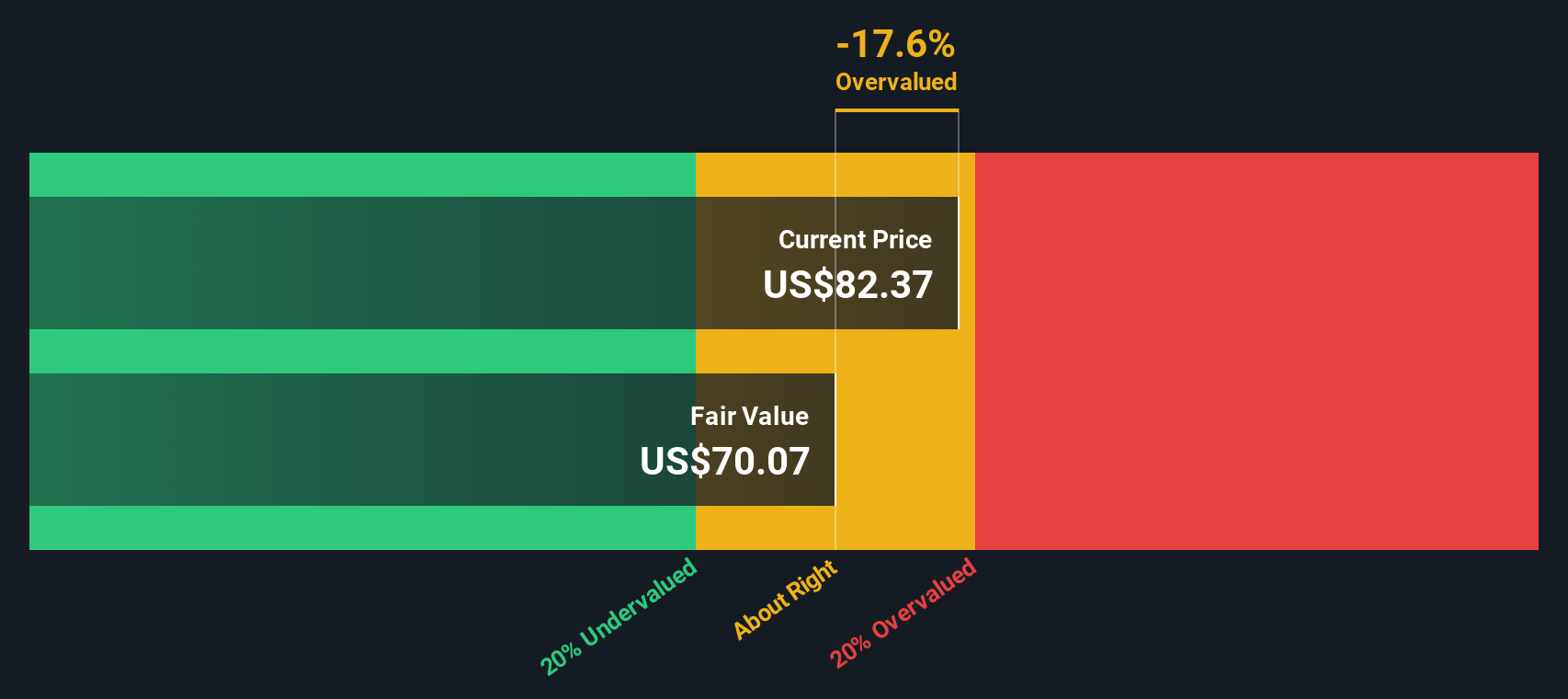

Westlake's integrated manufacturing footprint in North America, as highlighted by Jean-Marc Gilson, President and CEO, is a significant asset. This strategic integration allows the company to optimize its production across various segments, enhancing cost efficiency and market penetration. The focus on product innovation and sustainability, particularly in polyethylene, further strengthens its position. Steve Bender, CFO, noted record sales volumes driven by the adoption of post-consumer recycled products, showcasing Westlake's commitment to meeting customer demands while boosting profitability. Financially, Westlake's investment-grade balance sheet with $2.9 billion in cash provides the flexibility for strategic investments and acquisitions, supporting future growth. Notably, the company is trading below its estimated fair value of $225.05, with a target price indicating a potential increase of over 20%, reflecting its strong market positioning.

Vulnerabilities Impacting Westlake

The company faces certain vulnerabilities. The impact of unplanned maintenance outages, as reported by Gilson, resulted in a $120 million hit to EBITDA, underscoring operational challenges. Weather-related disruptions also deferred shipments, affecting sales volumes in the HIP segment. Additionally, competitive pressures from low-cost Asian imports are squeezing margins in the epoxy business, particularly in Europe. Financially, the past year's earnings growth saw a 91.9% decline, and the current net profit margin is 0.8%, down from 9.2% last year. The high dividend payout ratio of 268.1% suggests earnings are not adequately covering dividends, which could be a concern for investors.

Potential Strategies for Leveraging Growth and Competitive Advantage

The housing market presents a promising opportunity for Westlake, with Gilson expressing optimism about pent-up demand driving construction activity as interest rates are expected to reduce by 2025. This could significantly benefit the HIP segment. Moreover, easing monetary policies and economic stimulus measures by the U.S. Federal Reserve and ECB could enhance consumer demand for durable goods and housing. Westlake's continued development of innovative products, like PVCO and ABA pipes, positions it well for market expansion and increased share. Analysts forecast a target price more than 20% higher than the current share price, indicating potential upside.

Market Volatility Affecting Westlake's Position

Economic uncertainty remains a threat, with slow recovery in key regions posing risks to growth projections. Regulatory and trade challenges, such as ongoing disputes and potential antidumping duties, could impact market dynamics and profitability. Additionally, volatility in raw material and feedstock costs may affect margins and operational expenses. Despite these challenges, Westlake's strategic initiatives and financial health provide a solid foundation to navigate these external pressures effectively.

Conclusion

Westlake's strategic integration of its North American manufacturing operations positions it to effectively manage production costs and expand market reach, bolstering its competitive edge. The company's focus on innovation and sustainability, particularly in polyethylene, aligns with market trends and customer demand, enhancing its long-term profitability prospects. The potential for growth in the housing market, coupled with strategic investments supported by a strong cash position, underscores Westlake's capacity to capitalize on emerging opportunities. Trading below its estimated fair value of $225.05, with a target price suggesting over 20% upside, indicates that the market may not fully recognize Westlake's growth potential and strategic positioning, offering a compelling opportunity for investors.

Key Takeaways

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Westlake, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Westlake might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WLK

Westlake

Manufactures and markets performance and essential materials, and housing and infrastructure products in the United States, Canada, Germany, China, Mexico, Brazil, France, Italy, and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives