- United States

- /

- Metals and Mining

- /

- NYSE:MP

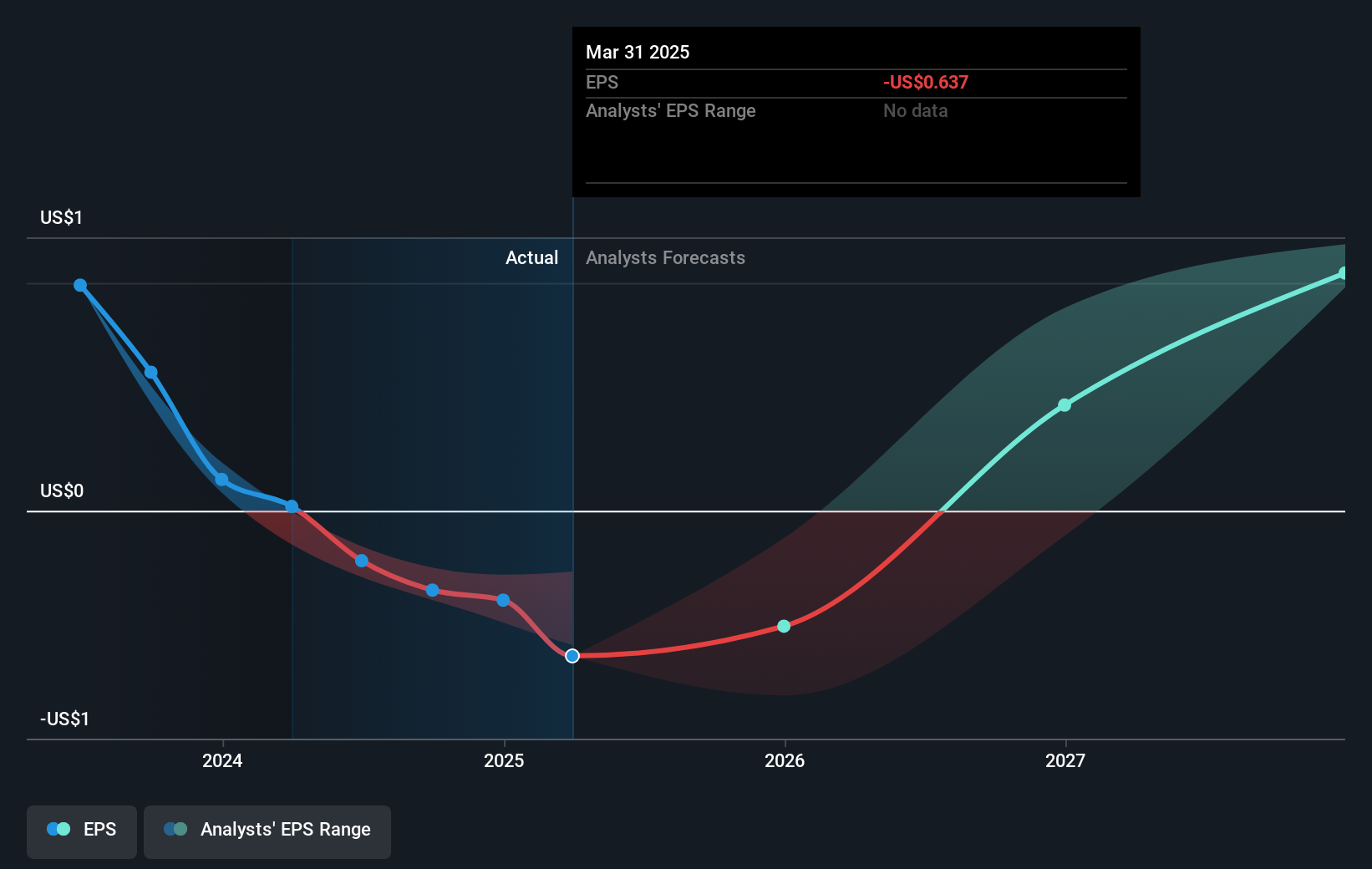

MP Materials (NYSE:MP) Reports Q1 Net Loss Despite Increase In REO Production

Reviewed by Simply Wall St

MP Materials (NYSE:MP) recently signed a Memorandum of Understanding with the Saudi Arabian Mining Company to develop a rare earth supply chain in Saudi Arabia, aligning with growing global demands. Despite reporting a net loss for the first quarter, the company increased its REO and NdPr production volumes. Additionally, no shares were repurchased in the recent buyback tranche, reflecting existing efforts. Over the past week, the company's share price rose by 11%, notably outperforming the market's 2% gain. Enhanced production results and the promising alliance appear to add weight to this recent upward trend amidst broader market growth.

We've discovered 1 weakness for MP Materials that you should be aware of before investing here.

The recent Memorandum of Understanding between MP Materials and the Saudi Arabian Mining Company could significantly influence MP's growth narrative. By developing a rare earth supply chain in Saudi Arabia, the company stands to expand its reach into ex-China markets, potentially increasing revenue opportunities and enhancing production efficiency. This collaboration may further bolster MP’s position by integrating strategic partnerships, which aligns well with existing efforts to enhance production capacities.

Over the longer term, MP Materials' total return, including share price and dividends, was 34.34% over the past year. This performance exceeds both the broader market's return and the US Metals and Mining industry, which had varying results over the same period. While the company's share price rose by 11% in the past week, outperforming the 2% market gain, its longer-term success underscores its enhanced capabilities in navigating volatile pricing and market demands.

The recent partnership news might positively impact revenue and earnings forecasts, further pushing analyst expectations. Given the increased production capabilities and expanded market access through new agreements, analysts' anticipated revenue growth of 33.6% per year could see validation. The consensus price target of US$26.69, slightly higher than the current share price of US$24.58, suggests moderate upside potential, indicating that the market views the company's future prospects with cautious optimism. Nonetheless, the forecasted improvement in margins and earnings growth would be critical in achieving the price target, inviting investors to evaluate their assumptions against these predictions.

Click to explore a detailed breakdown of our findings in MP Materials' financial health report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MP

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion