Advertisement

- United States

- /

- Metals and Mining

- /

- NYSE:HL

What Can We Learn About Hecla Mining's (NYSE:HL) CEO Compensation?

Phillips Baker has been the CEO of Hecla Mining Company (NYSE:HL) since 2003, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

View our latest analysis for Hecla Mining

How Does Total Compensation For Phillips Baker Compare With Other Companies In The Industry?

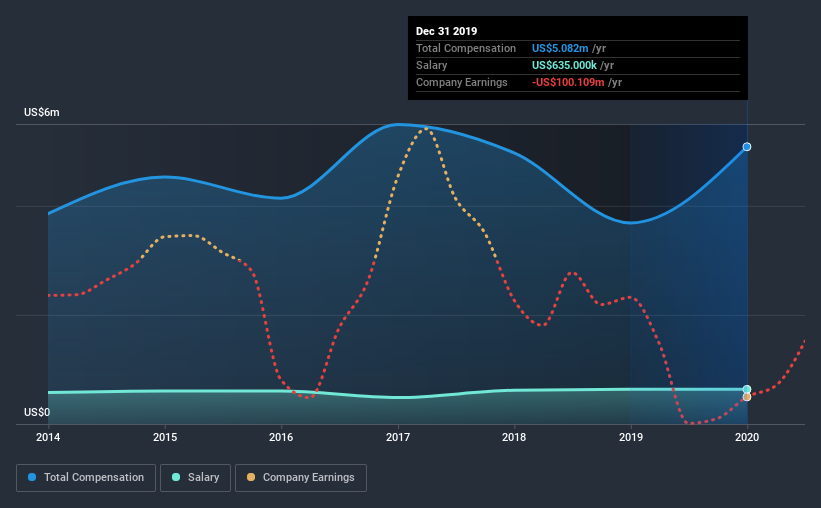

At the time of writing, our data shows that Hecla Mining Company has a market capitalization of US$3.1b, and reported total annual CEO compensation of US$5.1m for the year to December 2019. That's a notable increase of 38% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at US$635k.

On examining similar-sized companies in the industry with market capitalizations between US$2.0b and US$6.4b, we discovered that the median CEO total compensation of that group was US$6.4m. From this we gather that Phillips Baker is paid around the median for CEOs in the industry. Furthermore, Phillips Baker directly owns US$20m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | US$635k | US$635k | 12% |

| Other | US$4.4m | US$3.1m | 88% |

| Total Compensation | US$5.1m | US$3.7m | 100% |

Talking in terms of the industry, salary represented approximately 37% of total compensation out of all the companies we analyzed, while other remuneration made up 63% of the pie. In Hecla Mining's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

A Look at Hecla Mining Company's Growth Numbers

Over the last three years, Hecla Mining Company has shrunk its earnings per share by 69% per year. It achieved revenue growth of 22% over the last year.

Investors would be a bit wary of companies that have lower EPS But in contrast the revenue growth is strong, suggesting future potential for EPS growth. In conclusion we can't form a strong opinion about business performance yet; but it's one worth watching. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Hecla Mining Company Been A Good Investment?

Hecla Mining Company has generated a total shareholder return of 16% over three years, so most shareholders would be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

As we noted earlier, Hecla Mining pays its CEO in line with similar-sized companies belonging to the same industry. But revenue growth over the last year can't be ignored. Meanwhile, we would have liked to see shareholder returns post more substantial growth. An additional worry is EPS , which has posted negative growth in the previous three years. But we don't think the CEO compensation is a problem, although shareholders might want to see more growth before agreeing that Phillips should get a raise.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 3 warning signs for Hecla Mining that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you decide to trade Hecla Mining, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hecla Mining might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NYSE:HL

Hecla Mining

Provides precious and base metal properties in the United States, Canada, Japan, Korea, and China.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.9% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|21.3% undervalued

TI

Community Contributor