Advertisement

- United States

- /

- Chemicals

- /

- NYSE:ECL

Assessing Ecolab (ECL) Valuation After Its Multi‑Billion Dollar Fixed‑Rate Bond Offerings

What Ecolab’s new bond offerings mean for equity investors

Ecolab (ECL) has just tapped the bond market with several fixed rate note offerings totaling multiple billions of US dollars, across maturities from 2029 to 2036, drawing fresh attention to the stock.

The company issued callable, senior unsecured notes with fixed coupons, including 4.600% notes due 2029, 4.800% notes due 2031, 5.150% notes due 2033, and 5.350% notes due 2036, each priced slightly below par.

See our latest analysis for Ecolab.

The bond issuance comes as the stock trades at US$248.64, with the 30 day share price return down 9.8% and the 90 day share price return down 17.4%. The 3 year total shareholder return of 53.1% points to stronger longer term momentum, despite a more muted 1 year total shareholder return of a 3.7% decline.

If the recent pullback in Ecolab has you reassessing your watchlist, this can be a good moment to broaden your view and check out 20 top founder-led companies

With Ecolab’s shares down over the past quarter but longer term returns still positive, and with several billion dollars of new fixed rate debt now in place, is the stock offering value today, or is the market already pricing in future growth?

Most Popular Narrative: 22% Undervalued

With Ecolab’s fair value narrative set at $318.95 against a last close of $248.64, the valuation gap rests on a detailed earnings and margin story.

Analysts are assuming Ecolab's revenue will grow by 7.9% annually over the next 3 years. Analysts assume that profit margins will increase from 12.9% today to 15.0% in 3 years time.

Read the complete narrative. Read the complete narrative.

Want to see what kind of revenue path and margin reset could justify that higher fair value? The narrative leans on compound growth, firmer profitability and a premium future earnings multiple. Curious how those ingredients combine into one price target engine?

Result: Fair Value of $318.95 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this narrative still hinges on risks related to softer demand in heavy industrial markets, as well as higher costs from tariffs and local suppliers that could pressure margins.

Find out about the key risks to this Ecolab narrative.

Another way to look at Ecolab’s valuation

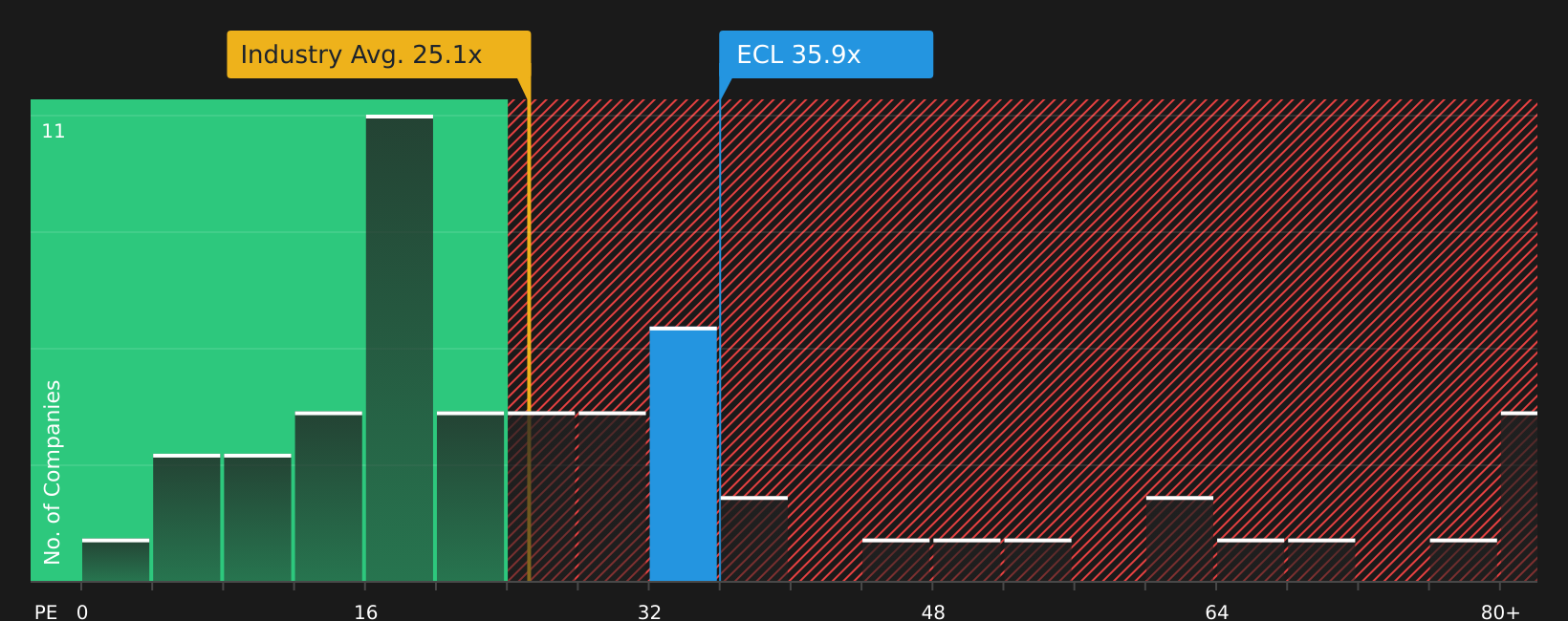

That 22% “undervalued” fair value hinges on earnings forecasts and a premium future P/E. Yet on today’s numbers, Ecolab trades on a P/E of 33.2x, compared with a fair ratio of 24.9x and an industry average of 26.8x, which points to a rich price tag rather than a bargain. So which signal earns more weight in your own framework?

Before leaning on any single ratio, it helps to see how current pricing stacks up across peers, the industry and the fair ratio over time. Then you can decide what kind of valuation risk you are comfortable taking on. See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Seeing mixed signals on value, risk and returns so far? Act while the details are fresh in your mind and weigh both sides with 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Ecolab is on your radar, do not stop there. Widen your opportunity set with a few targeted stock ideas that match different goals and risk levels.

- Target steadier portfolios by reviewing companies that rank highly in our 67 resilient stocks with low risk scores so you are not relying on a single stock story.

- Pursue potential mispricings with the 51 high quality undervalued stocks to spot companies where current prices differ meaningfully from their assessed fundamentals.

- Hunt for future standouts using the screener containing 21 high quality undiscovered gems before these opportunities attract wider market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Ecolab might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ECL

Ecolab

Provides water, hygiene, and infection prevention solutions and services in the United States and internationally.

Proven track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4353.2% undervalued

73 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22043.1% undervalued

23 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.8% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

RE

RetiredbutWorking on USA Rare Earth ·

USAR Secures $19.3M Boost to Develop an Independent Rare Earth Supply Chain

Fair Value:US$0.336.7k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1932.1% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NE

newsfinder11221 on Tanco Holdings Berhad ·

Tanco Holdings Expands Growth Pipeline With Smart Port, ECRL And Property Projects

Fair Value:RM 8.1279.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.0% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.8% undervalued

1190 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative