- United States

- /

- Chemicals

- /

- NYSE:CTVA

Corteva (CTVA): Taking Stock of Valuation After a Recent Pullback in Defensive Growth Shares

Reviewed by Simply Wall St

Corteva (CTVA) has quietly given back some gains over the past month, even as its year to date return remains solidly in positive territory, and that gap is catching investors attention.

See our latest analysis for Corteva.

That recent pullback sits against a backdrop of a much stronger year to date share price return of 16.2 percent and a 5 year total shareholder return of 77.5 percent, suggesting long term momentum remains intact even as near term enthusiasm cools.

If Corteva has you rethinking where defensive growth might come from, it could be worth scanning other quality healthcare stocks that balance resilience with earnings potential.

With earnings still growing, shares trading below analyst targets and only a modest intrinsic premium, the key question now is simple: is Corteva at an attractive entry point or is the market already baking in its next leg of growth?

Most Popular Narrative: 15.7% Undervalued

With Corteva last closing at $65.48 against a narrative fair value of $77.71, the current setup hinges on how far earnings can climb from here.

Analysts expect earnings to reach $2.3 billion (and earnings per share of $3.55) by about September 2028, up from $1.5 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $2.0 billion.

Curious how moderate top line growth, expanding margins, and a richer future earnings multiple can still point to upside from here? The narrative’s assumptions may surprise you.

Result: Fair Value of $77.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent crop protection price pressure and execution risks around the planned seed and pesticide split could still derail the implied upside from this point.

Find out about the key risks to this Corteva narrative.

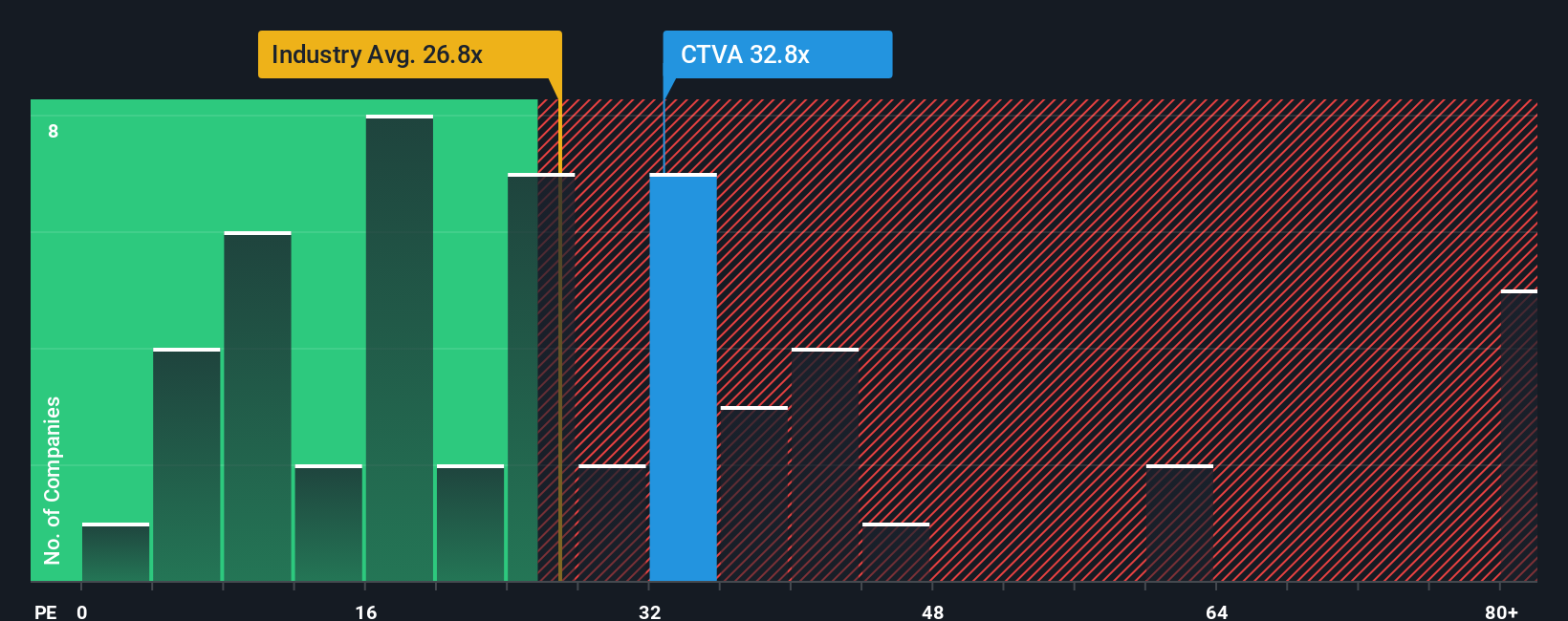

Another View: Rich On Earnings

While the narrative fair value suggests upside, the earnings lens tells a tighter story. Corteva trades on a P/E of 26.3 times versus a fair ratio of 24.8 times and a US Chemicals industry average of 24.1 times, implying limited margin of safety if sentiment sours.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Corteva Narrative

If you see the outlook differently or simply want to stress test your own thesis, build a tailored Corteva storyline in minutes, Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Corteva.

Ready for more investment ideas?

Before you move on, put Corteva in context by lining it up against fresh ideas from our stock screener, so you never miss a smarter opportunity.

- Capture potential bargains trading below their worth by targeting these 909 undervalued stocks based on cash flows that pair solid fundamentals with attractive upside.

- Ride powerful innovation trends by focusing on these 26 AI penny stocks positioned at the intersection of data, automation, and scalable business models.

- Strengthen your income stream by zeroing in on these 13 dividend stocks with yields > 3% that can help underpin long term returns with reliable payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CTVA

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion