Advertisement

- United States

- /

- Metals and Mining

- /

- NYSE:AU

A Look at AngloGold Ashanti (NYSE:AU) Valuation as Portfolio Optimization and New Projects Drive Investor Interest

Simply Wall St

Reviewed by Kshitija Bhandaru

AngloGold Ashanti (NYSE:AU) is making waves as it kicks off drilling at the Organullo Gold Project in Argentina. The company is also streamlining its asset portfolio and focusing on tighter cost controls. These steps are helping strengthen its margins and lifting investor optimism.

See our latest analysis for AngloGold Ashanti.

AngloGold Ashanti’s share price has built a steady upward trend over the past month and quarter, now trading at $72.46. This momentum reflects renewed investor confidence as the company sharpens its portfolio focus and delivers on production stability and margin gains, with its one-year total shareholder return holding positive as well. While long-term returns have been modest, recent actions have attracted attention and may be signaling the start of a more dynamic growth phase.

If you’re looking to spot other companies benefitting from operational momentum and management focus, it’s a great time to discover fast growing stocks with high insider ownership

But with shares already climbing and investor sentiment strong, the pressing question for potential buyers is whether AngloGold Ashanti remains undervalued at current levels or if the market has already priced in the company’s future growth story.

Most Popular Narrative: 24.9% Overvalued

With AngloGold Ashanti last closing at $72.46 and the narrative fair value set at $58.00, the market price stands notably above the most widely followed expectations. This divergence is driven by bold assumptions around gold demand and the company’s operational enhancements, setting the scene for debate on whether optimism has gone too far.

Ongoing optimization of asset portfolio toward lower-risk jurisdictions, combined with disciplined cost control, notably, stable cash cost and AISC in real terms despite sectoral inflation, is improving production stability and supporting structurally stronger net margins. Organic production growth from brownfield projects, Obuasi ramp-up, Cuiabá, Siguiri, Geita, and upcoming Nevada developments is set to increase output volumes and extend mine life, driving future revenue and earnings growth over the next decade.

Want to know how these margin gains and new gold ounces are fueling this high valuation? The narrative is built on powerful forecasts for revenue, profits, and future multiples. But what numbers are so convincing that they justify such a premium? The details might surprise you. Dive deeper to see exactly which bold financial leaps support this fair value.

Result: Fair Value of $58.00 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising operating costs and unpredictable regulatory delays could challenge AngloGold Ashanti’s bullish outlook and threaten future growth momentum.

Find out about the key risks to this AngloGold Ashanti narrative.

Another View: Numbers Point to Good Value

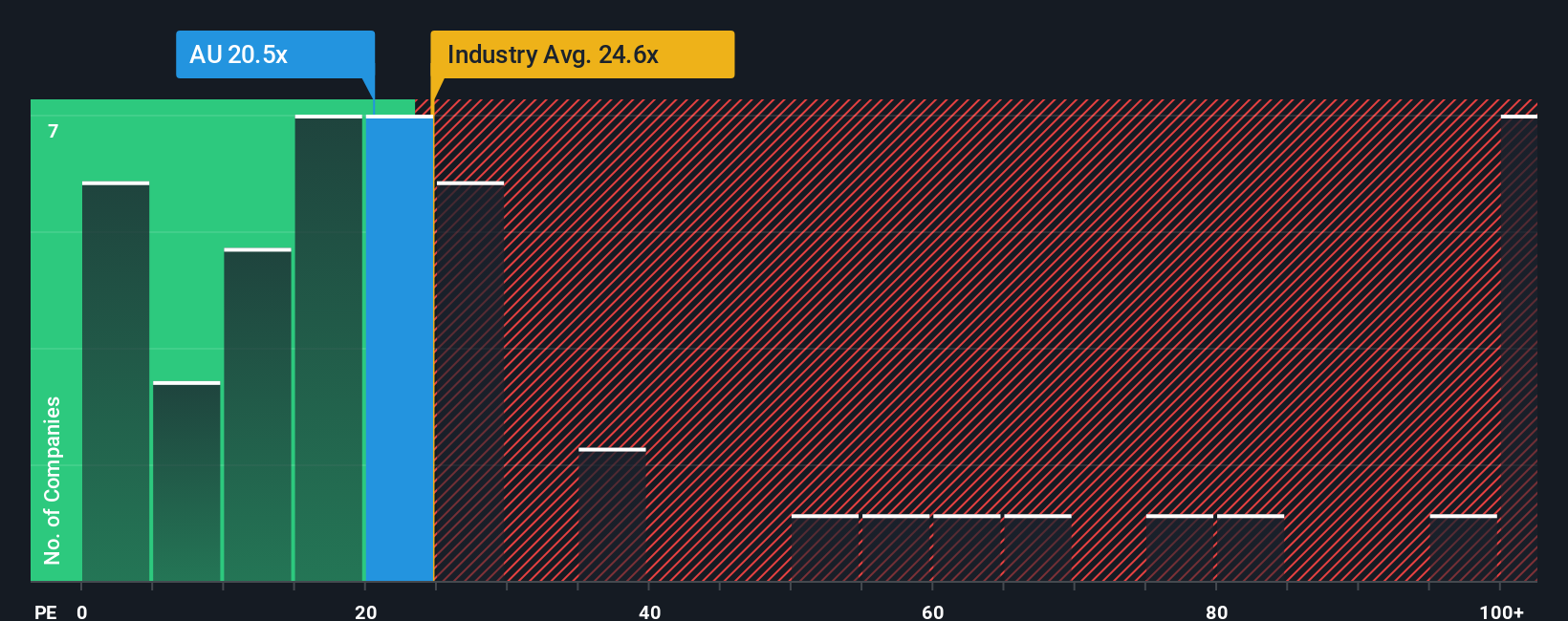

Looking from a different angle, AngloGold Ashanti’s price-to-earnings ratio stands at 20.3x, which is lower than both the US Metals and Mining industry average of 24.7x and the peer average of 34.1x. Even when compared to the fair ratio, estimated at 29.2x, the company trades at a discount. This gap signals that, despite the ongoing debate over whether shares are overvalued, there could still be underlying value that the market has yet to fully appreciate. Is this a sign investors are missing something, or is it a warning that optimism might be exceeding reality?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own AngloGold Ashanti Narrative

If you see the story differently or want to dig into the numbers yourself, you can easily craft your own take in just a few minutes with Do it your way

A great starting point for your AngloGold Ashanti research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let your next smart move slip through the cracks. Your best investing opportunities might be just a click away, beyond what’s in the headlines.

- Spot emerging market leaders and seize the upside early by checking out these 3563 penny stocks with strong financials making waves with strong financials and growth stories.

- Benefit from growth sectors and see what’s fueling innovation in healthcare by reviewing these 31 healthcare AI stocks leveraging artificial intelligence for breakthroughs.

- Unlock potential long-term winners and value opportunities you might have missed with these 900 undervalued stocks based on cash flows based on robust cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AU

AngloGold Ashanti

Operates as a gold mining company in Africa, Australia, and the Americas.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor