- United States

- /

- Chemicals

- /

- NYSE:ALB

Albemarle Tops Our List of Lithium Stocks - Who Else is Worth Checking Out?

We are looking for feedback on this article .

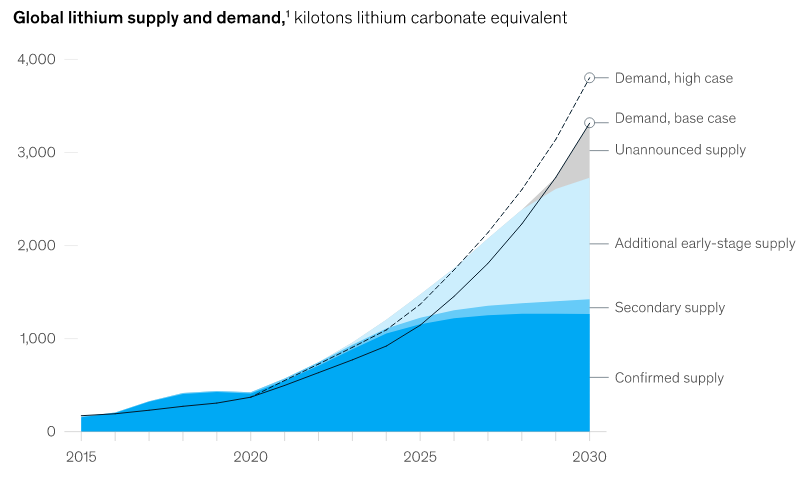

Lithium has been the talk of the town recently and it’s no secret as to why. Recent estimates from McKinsey suggest a global demand of around 3 million metric tons of lithium carbonate equivalent (LCE) in 2030. In contrast, the total global LCE output for 2021 amounted to only 540,000 metric tons, a mere 18% of the anticipated need for 2030. These figures point to a potential shortfall in the future and questions are being raised over how this demand will be met.

The rise in this demand is attributed to an increase in consumer demand for Electric Vehicles (EVs). These EVs are requiring batteries that have higher energy densities and longer lifespans, the main component of which is high-grade lithium. The sudden rise in demand has caused raw lithium prices to skyrocket, leaving battery producers scrambling to secure their supply of a commodity that is quickly entering into a shortage. So this begs the question: Which companies are best positioned to take advantage?

Albemarle Corporation (NYSE:ALB)

Albemarle is a global leader in the extraction and production of lithium, bromine and refining catalyst solutions. Lithium is undoubtedly the largest branch of the business, accounting for 42% of the US$3.3B in net sales for the 2021 calendar year.

At a current output of 88,000 metric tons of LCE per year, Albemarle asserts itself as a dominant player in the lithium market at 16% total market share. The company is poised to continue in a strong market popsition with plans expand processing infrastructure in 2022 and with the long-term goal of more than doubling their lithium production capacity. With this expansion pipeline, they'll be targeting low-cost juristictions to reduce capital expenditure and impove returns.

Here are where we see Albemarle’s competitive advantage lay:

- Project feasibility. Albemarle has proved it can already economically produce battery grade lithium in a period where lithium prices were much lower, illustrating the company’s ability to continue operations should lithium prices fall.

- Ability to be self-funded. Albemarle's lithium branch is already profit making, so earnings can be retained and capital can be invested into the aforementioned expansion projects without the need for significant capital raises or taking on large amounts of debt. Smaller companies and emerging players will have to undergo financing stages which carry risks and may result in shareholder dilution.

Albemarle has a firm grasp on the market and seems positioned to continue riding this lithium wave from strength to strength. But these factors don’t paint the full picture and investors should always consider the financials of a company to inform their assessment. You can see our analysis of Albemarle’s financials for free on our website .

Sociedad Química y Minera de Chile (NYSE:SQM)

Sociedad Química y Minera de Chile (SQM) stands as the NYSE’s other lithium giant. Producing 101,000 metric tons of LCE during 2021, SQM’s impressive output accounts for 18.7% of global lithium production for the year and with several project expansions in the works, this output will continue to scale with the market demand.

According to SQM’s latest earnings report, 2022 sales estimates top out at 140,000 metric tons of lithium, with capacity potentially reaching 190,000-200,000 should expansion projects be completed in time, and dependant on the market demand for lithium.

Here are the key factors driving the company forward in the next few years:

- Significant Expansion pipeline. With SQM’s joint venture in Mt Holland expecting to enter production in 2024 and a drastic increase to the production capabilities of their Salar del Carmen project, there’s ample opportunity for the company to grow their presence in the market and beat out new entrants.

- Variable exposure to lithium prices. Looking forward to 2022, SQM’s sales contracts are detailed as follows: 20% fixed or variable price, 50% variable price with a ceiling and 30% not contracted. This means that SQM will still be exposed to the increase in lithium prices on previously negotiated contracts even if the price of lithium was lower at the time the contract was agreed upon, opening the company up to increased revenues.

Investors should always consider the risks and financial health of a company to inform their investment decision. You can see our rundown of SQM’s risks and financials for free on our website .

Livent Corporation (NYSE:LTHM)

Livent’s premier resource is located in Salar Del Hombre Muerto in Argentina, achieving a reasonable current output of 27,000 metric tons of Lithium Carbonate and Lithium Chloride. While this is modest in comparison to the big players in the sector, expansion is at the forefront of the company’s mission, with a 20,0000 metric tons expansion of their Argentinian operation slated for 2023 and a further 20,000 metric tons anticipated for 2025.

Livent’s production figures account for around 5% of the total market share. While this lags the other two companies, Livent’s key focus on cost leadership within the production of LCE, Lithium Hydroxide and Lithium Chloride should provide an advantage over its peers.

These are the factors that are important to the performance of Livent:

- Low cost focus. High lithium prices can make many more projects economically feasible, but striving for lower operating costs will mean a project can weather the storm if demand and prices fall. By securing a low-impurity lithium resource, Livent has allowed processing costs to be cut, giving a competitive advantage over other brine operations.

- Exposure to Lithium Carbonate, Lithium Chloride and Lithium Hydroxide prices. New high-density batteries are more compatible with lithium hydroxide owing to greater nickel content in the cathodes. Should primary lithium demand switch from carbonate to hydroxide, Livent’s exposure to the prices in both products should help it navigate pricing volatility.

Livent is a smaller company and that does carry some possible risks. Investors who are interested in finding out more can do so for free on our website .

The Future Prospects

When you take a step back and look at the global lithium sector, you begin to see a trend. Most supply comes from a select few companies, leaving a mass of newcomers are scrambling to secure funding to bring their projects to market. After all, there’s no shortage of lithium resources on Earth, just a shortage of processing power to extract it from the ground and refine it. New companies coming to the table will reach maturity and begin reaping the rewards of their capital investments. These next few companies aren’t generating significant revenues but we believe they’ll be ones to watch.

Lithium Americas Corp. (NYSE:LAC)

Lithium Americas is an emerging player in the sector. Their flagship project is their Cauchari-Olaroz brine resource in Argentina, which is currently 85% through the construction of its Stage 1 production facility, targeting 40,000 metric tons per annum (tpa) of battery-grade lithium carbonate. Lithium Americas is striving for cost leadership, forecasting operating expenditure of US$3,600 per metric tonne. With a project life of 40 years and a second stage expansion already on the cards, there is plenty to keep investors following their developments closely.

Here are some of the Lithium Americas’ most eye-catching features:

- Completed acquisition of Millennial Lithium in January 2022. Lithium Americas now has 100% ownership of the advanced-stage Pastos Grandes project, which is located nearby to their Caucharí-Olaroz tenements. The transaction was completed for around US$400 million and provides Lithium Americas with exposure to a rich brine resource of 4.1 million metric tonnes of LCE.

- Continued development of Thacker Pass resource. Lithium Americas has a 100% stake in one of the largest resources in the United States. The project’s feasibility study is due in the second half of 2022, targeting 40,000 tpa of lithium carbonate, with scenarios being assessed for expansion up to a total of 80,0000 tpa. Preparation work to begin construction of the initial infrastructure is set to commence in 2022.

For those who are eager to find out more, you can do so by taking a look at the future growth section in our company report for Lithium Americas on our website .

Piedmont Lithium Inc. (NASDAQ:PLL)

Piedmont Lithium Inc. is a lithium company looking to develop key strategic assets in North Carolina, Quebec and Ghana. With a consolidated enterprise targeting 60,000 tonnes of LiOH per year and an additional 390,000 tonnes per year in spodumene concentrate (SC6) production, Piedmont is looking to become a significant player in America’s shift to newer energy initiatives.

Here is why Piedmont Lithium’s future may become interesting:

- Entered into a binding agreement with Tesla Inc. (NASDAQ:TSLA) to supply spodumene concentrate from their North Carolina project. The agreement is for an initial five-year term on a fixed price commitment representing one-third of Piedmont’s planned production from their North Carolina project. Deliveries planned to begin between July 2022 and July 2023, but timeline has been postponed indefinitely due to delays in development.

- The Carolina project offers industry leading sustainability with close proximity to a key target market. Piedmont owns 100% of the project which is set to lead the way in terms of cost and sustainability, offering much lower direct water usage in the processing of lithium hydroxide, requiring only 6,300 gallons per tonne of LiOH. Compare this to Chilean projects in the Atacama region which need up to 124,000 gallons of water per tonne, it’s clear to see where the benefits lay for Piedmont as water scarcity continues to be a frequent discussion point into the future.

If you’re looking to find out about the growth estimates for Piedmont Lithium Inc. (NASDAQ:PLL), we encourage you to take a deep dive into our coverage of analysts’ estimates for the company in our company report .

Standard Lithium Ltd. (NYSE:SLI)

Standard Lithium Ltd. is a steadily growing lithium prospect, headquartered out of Vancouver, Canada. Touting itself as “America’s 21st Century lithium company”, Standard Lithium vows to be the answer to the question of lithium supply but within an innovative context. Partnering with chemical major LANXESS AG (ETR:LXS) , the company is planning to implement ground-breaking technology and leverage their class leading resource to help them rise to the top of the lithium game.

Here are some points of interest to kick-start your research into Standard Lithium:

- Ability to fast-track commercial brine operations using existing brine operations. Standard lithium is able to piggy-back its operations off of LANXESS’ existing bromine extraction facility, negating the need for exorbitant capital expenditure that other companies of similar size will have to go through.

- First to market with a revolutionary extraction process. Standard Lithium has developed its own direct lithium extraction (DLE) process called LiSTR. The company promotes this proprietary process as being able to deliver increased recovery efficiency when compared to traditional evaporation methods and a smaller environmental footprint. The most valuable part of this process is that it is scalable, modular and able to be bolted on the LANXESS’ existing bromine infrastructure, allowing Standard Lithium to bring their lithium to market more quickly than competitors.

For those that appreciate the future merits of Standard Lithium Ltd. (NYSE:SLI) and wish to know more about the company’s current financial health can do so by heading to the company report on our website.

The Bottom Line

With expansion on the horizon for all of these companies, it appears that they’re all well positioned to tackle the impending energy revolution. But this shift to cleaner energy isn’t just going to impact lithium companies. Energy production, storage and personal transportation industries are primed to undergo rapid change as fossil fuels are phased out, paving the way for innovation. We encourage you to check out

our list of the largest automakers from around the globe to see if you can identify the key players that will adapt to the changing landscape.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Bailey and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Bailey Pemberton

Bailey is an Equity Analyst at Simply Wall St with 4 years of experience as an Associate Adviser at Baywealth Financial Group, where he helped with client portfolio management, investment strategy and research. He completed a Bachelor of Commerce majoring in Finance from the University of Western Australia. As an equity analyst, Bailey provides the team with valuable insights, helping guide the creation of article content and new features like Narratives.

About NYSE:ALB

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Automotive Electronics Manufacturer Consistent and Stable

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion