Advertisement

- United States

- /

- Chemicals

- /

- NasdaqGS:LIN

Is Linde plc (NASDAQ:LIN) Potentially Undervalued?

Today we're going to take a look at the well-established Linde plc (NASDAQ:LIN). The company's stock saw a double-digit share price rise of over 10% in the past couple of months on the NASDAQGS. The recent share price gains has brought the company back closer to its yearly peak. With many analysts covering the large-cap stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. However, could the stock still be trading at a relatively cheap price? Today we will analyse the most recent data on Linde’s outlook and valuation to see if the opportunity still exists.

What's The Opportunity In Linde?

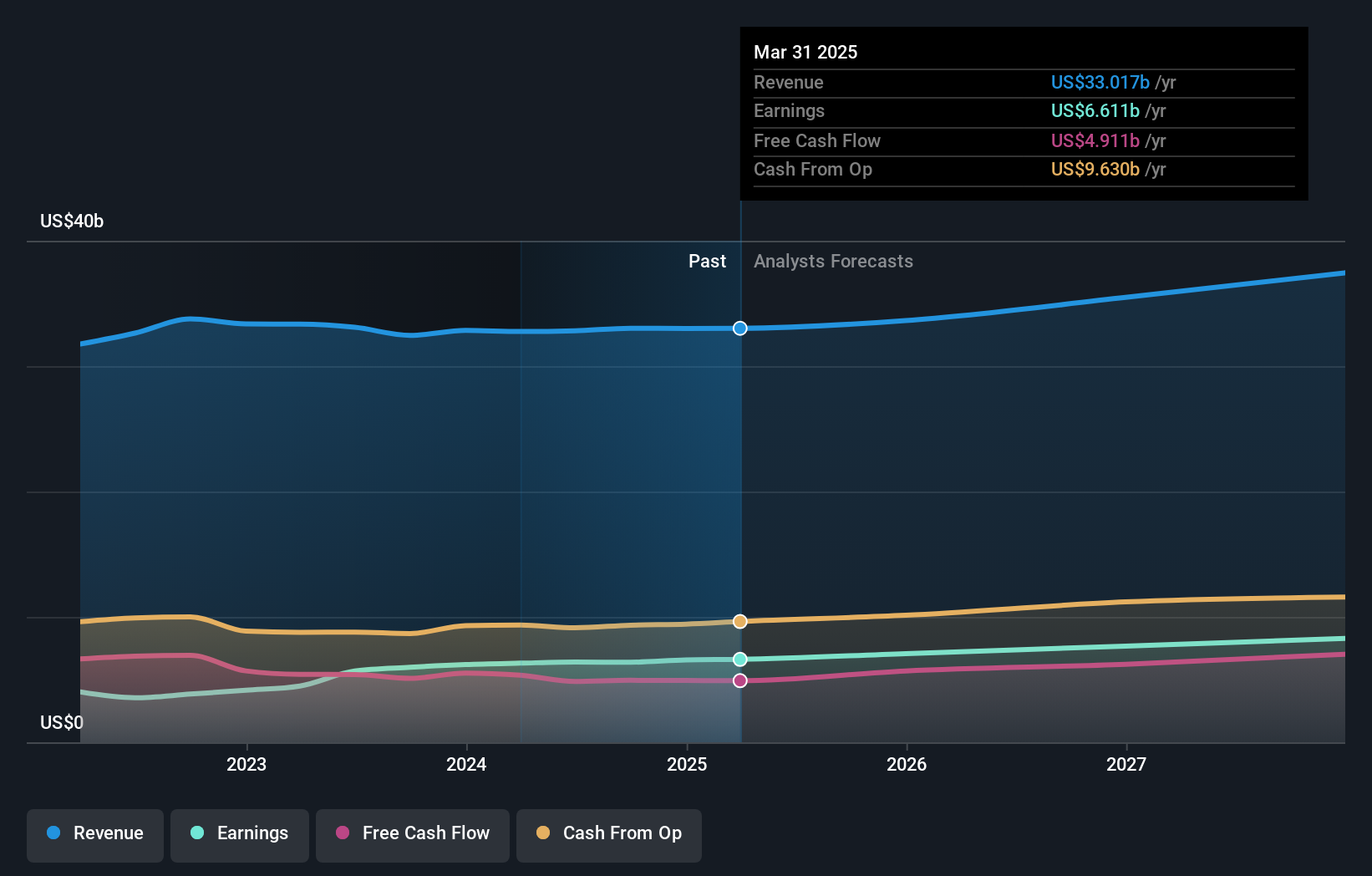

According to our price multiple model, where we compare the company's price-to-earnings ratio to the industry average, the stock currently looks expensive. In this instance, we’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. We find that Linde’s ratio of 33.02x is above its peer average of 22.27x, which suggests the stock is trading at a higher price compared to the Chemicals industry. In addition to this, it seems like Linde’s share price is quite stable, which could mean two things: firstly, it may take the share price a while to fall back down to an attractive buying range, and secondly, there may be less chances to buy low in the future once it reaches that value. This is because the stock is less volatile than the wider market given its low beta.

Check out our latest analysis for Linde

Can we expect growth from Linde?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. Linde's earnings over the next few years are expected to increase by 30%, indicating a highly optimistic future ahead. This should lead to more robust cash flows, feeding into a higher share value.

What This Means For You

Are you a shareholder? It seems like the market has well and truly priced in LIN’s positive outlook, with shares trading above industry price multiples. However, this brings up another question – is now the right time to sell? If you believe LIN should trade below its current price, selling high and buying it back up again when its price falls towards the industry PE ratio can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping tabs on LIN for some time, now may not be the best time to enter into the stock. The price has surpassed its industry peers, which means it is likely that there is no more upside from mispricing. However, the positive outlook is encouraging for LIN, which means it’s worth diving deeper into other factors in order to take advantage of the next price drop.

So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. While conducting our analysis, we found that Linde has 2 warning signs and it would be unwise to ignore these.

If you are no longer interested in Linde, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:LIN

Linde

Operates as an industrial gas company worldwide.

Proven track record second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7059.1% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17030.5% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.8% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.5% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

JU

julio on Bath & Body Works ·

BBWI VALUATION

Fair Value:US$32.943.1% undervalued

20 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on NGEx Minerals ·

Lundin-Backed: 10x High-Grade Copper-Gold Discovery + Billion-Pound Resource Anchor

Fair Value:CA$4123.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Nippn ·

Do not mistake depreciation for deterioration

Fair Value:JP¥2.65k2.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.2% undervalued

124 followersusers have followed this narrative

2 commentsusers have commented on this narrative

35 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.7% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1926.5% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative