Advertisement

- United States

- /

- Chemicals

- /

- NasdaqCM:BON

Returns on Capital Paint A Bright Future For Bon Natural Life (NASDAQ:BON)

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. So when we looked at the ROCE trend of Bon Natural Life (NASDAQ:BON) we really liked what we saw.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Bon Natural Life, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

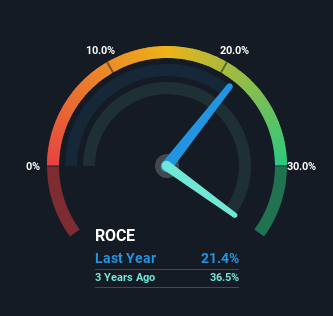

0.21 = US$6.5m ÷ (US$37m - US$6.6m) (Based on the trailing twelve months to September 2022).

Therefore, Bon Natural Life has an ROCE of 21%. That's a fantastic return and not only that, it outpaces the average of 11% earned by companies in a similar industry.

Check out our latest analysis for Bon Natural Life

Above you can see how the current ROCE for Bon Natural Life compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Bon Natural Life.

So How Is Bon Natural Life's ROCE Trending?

Bon Natural Life is displaying some positive trends. The data shows that returns on capital have increased substantially over the last four years to 21%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 288%. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

On a related note, the company's ratio of current liabilities to total assets has decreased to 18%, which basically reduces it's funding from the likes of short-term creditors or suppliers. So this improvement in ROCE has come from the business' underlying economics, which is great to see.

The Bottom Line

To sum it up, Bon Natural Life has proven it can reinvest in the business and generate higher returns on that capital employed, which is terrific. However the stock is down a substantial 70% in the last year so there could be other areas of the business hurting its prospects. In any case, we believe the economic trends of this company are positive and looking into the stock further could prove rewarding.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 5 warning signs for Bon Natural Life (of which 2 are potentially serious!) that you should know about.

High returns are a key ingredient to strong performance, so check out our free list ofstocks earning high returns on equity with solid balance sheets.

Valuation is complex, but we're here to simplify it.

Discover if Bon Natural Life might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:BON

Bon Natural Life

Engages in the research and development, manufacture, and sale of functional active ingredients extracted from natural herb plants in the People’s Republic of China and internationally.

Excellent balance sheet slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor