Advertisement

- United States

- /

- Insurance

- /

- NYSE:MKL

Is Markel Group’s Acquisition Spree Justifying Its 21% Rally in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if Markel Group is a hidden gem or fairly priced? You're not alone; many investors are eyeing this stock for its intriguing track record.

- The share price recently climbed 2.3% over the past week and has soared 21.1% year-to-date, suggesting real momentum and shifting perceptions in the market.

- Much of this recent activity is contextualized by news that Markel Group continues to pursue strategic acquisitions in the specialty insurance space, catching analysts' attention and fueling investor optimism. Headlines have also highlighted the company’s ongoing efforts to expand its investment portfolio, generating curiosity about what’s next.

- The official valuation score for Markel Group stands at 0 out of 6 on our checks, indicating it isn't considered undervalued by classic measures. Let's break down how this score is calculated, and stick around because we’ll share a smarter way to approach valuation at the end of this article.

Markel Group scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Markel Group Excess Returns Analysis

The Excess Returns valuation model focuses on how effectively a company puts its shareholders’ capital to work by looking at the difference between the return on invested equity and the cost of that equity. For Markel Group, this approach highlights key profitability and growth metrics emerging from analyst estimates and historical performance.

Markel Group has a Book Value of $1,429.48 per share and a Stable Earnings Per Share (EPS) of $119.86, derived from a weighted average of future return on equity projections from four analysts. The company's Cost of Equity is $110.03 per share, while the resulting Excess Return stands at $9.82 per share. With an average Return on Equity of 7.58% and a Stable Book Value forecast to rise to $1,581.85, Markel demonstrates solid, though not exceptional, returns above its cost of capital. This model suggests the company generates value, but only modestly relative to the required hurdle rate.

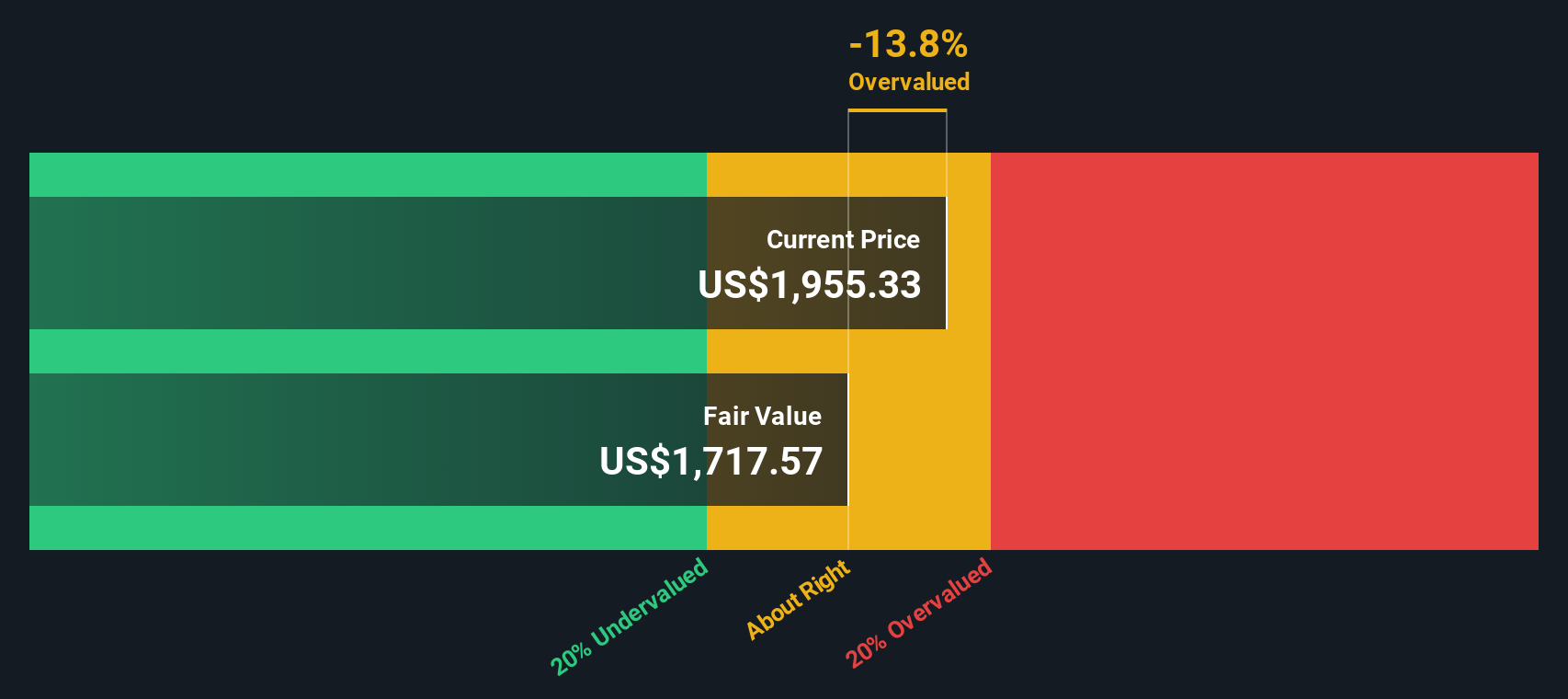

Based on these projections, Markel Group is estimated to be 12.6% overvalued compared to its intrinsic worth. This means the current share price exceeds the value implied by the company’s ability to produce returns on equity above its cost.

Result: OVERVALUED

Our Excess Returns analysis suggests Markel Group may be overvalued by 12.6%. Discover 917 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Markel Group Price vs Earnings

The price-to-earnings (PE) ratio is often the go-to valuation metric for established, profitable companies like Markel Group because it provides a clear sense of how much investors are willing to pay for each dollar of current earnings. It is especially useful for profitability-focused businesses since it intuitively links valuation with the company’s ability to consistently generate income.

However, what constitutes a “normal” or “fair” PE ratio depends largely on several factors. For example, companies expected to grow earnings rapidly or those with lower risks generally command higher PE multiples. On the other hand, sluggish growth or elevated risks will usually temper these ratios, since investors may not be willing to pay a premium.

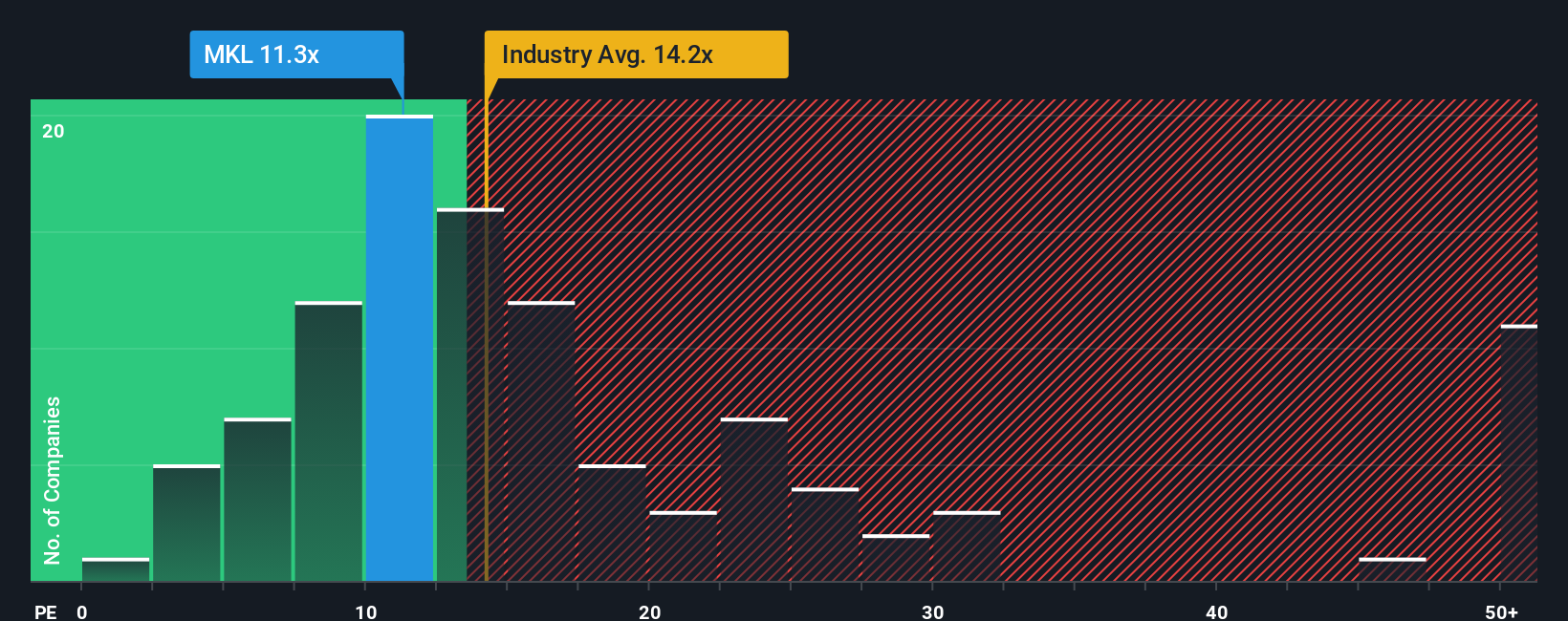

Markel Group currently trades at a PE ratio of 14.48x. This is slightly above both the insurance industry average of 13.18x and the peer average of 13.49x. Simply Wall St’s proprietary Fair Ratio for Markel is calculated at 11.17x. The Fair Ratio is a more reliable benchmark than standard comparisons because it weighs not only industry and market cap but also factors such as the company’s unique earnings growth forecasts, risks, and profit margins.

Given Markel’s actual PE is noticeably higher than its Fair Ratio, the stock appears overvalued using this approach.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Markel Group Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your unique perspective on a company, where you combine the story you believe, about its management, strategy, or industry dynamics, with numbers like future revenue, earnings, and margins to form your fair value estimate.

Narratives link what is actually happening in the business to a financial forecast, and then they show how those forecasts translate to a fair value for the stock. This approach, available and easy to use on Simply Wall St's Community page, lets millions of investors visualize and compare their outlooks, making it accessible for all experience levels.

You can use Narratives to decide when to buy or sell by contrasting your calculated Fair Value with the current Share Price, updating your view instantly as new information, such as news or earnings, comes in. For example, one Markel Group Narrative might forecast continued growth from digital transformation and capital redeployment (leading to a fair value above $2,053), while another might be cautious due to competitive threats and shrinking margins (with a lower estimate around $1,931), demonstrating how different stories can guide different investing decisions.

Do you think there's more to the story for Markel Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MKL

Markel Group

Through its subsidiaries, engages in the insurance business in the United States and internationally.

Excellent balance sheet with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative