Advertisement

- United States

- /

- Insurance

- /

- NYSE:LMND

Why Lemonade (LMND) Is Up After Raising 2025 Guidance Despite Ongoing Losses

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 5, 2025, Lemonade, Inc. reported third quarter results showing US$194.5 million in revenue and a net loss of US$37.5 million, while also raising its full year 2025 guidance amid strong year-to-date performance.

- Management's raised outlook and improving losses highlight operational progress and increasing confidence in Lemonade's ongoing digital insurance expansion.

- We'll examine how Lemonade's upgraded 2025 guidance and narrowing losses could alter the company's outlook amid competitive pressures.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Lemonade Investment Narrative Recap

To be a shareholder in Lemonade, you need to believe in the long-term scalability of its AI-powered insurance model and its ability to convert rapid revenue growth into profitability despite stiff competition. The latest earnings report, with narrowed losses and raised guidance, is encouraging but does not materially change the immediate challenge of achieving sustainable profit, still the closest short-term catalyst, and the ongoing risk of elevated operating expenses that could slow progress toward breakeven.

The most relevant company announcement is Lemonade’s updated full-year guidance following strong third quarter results. The company now expects 2025 revenue between US$727 million and US$732 million, a lift from previous forecasts, suggesting that recent operational improvements are having a tangible effect, which is critical in light of ongoing pressure on margins and mounting competition for digital insurance solutions.

On the flip side, investors should be aware that amid all the revenue momentum, the risk of prolonged operating losses remains front and center if...

Read the full narrative on Lemonade (it's free!)

Lemonade's outlook anticipates $1.8 billion in revenue and $201.4 million in earnings by 2028. Achieving this will require 44.9% annual revenue growth and an earnings increase of about $405 million from the current earnings of -$204.0 million.

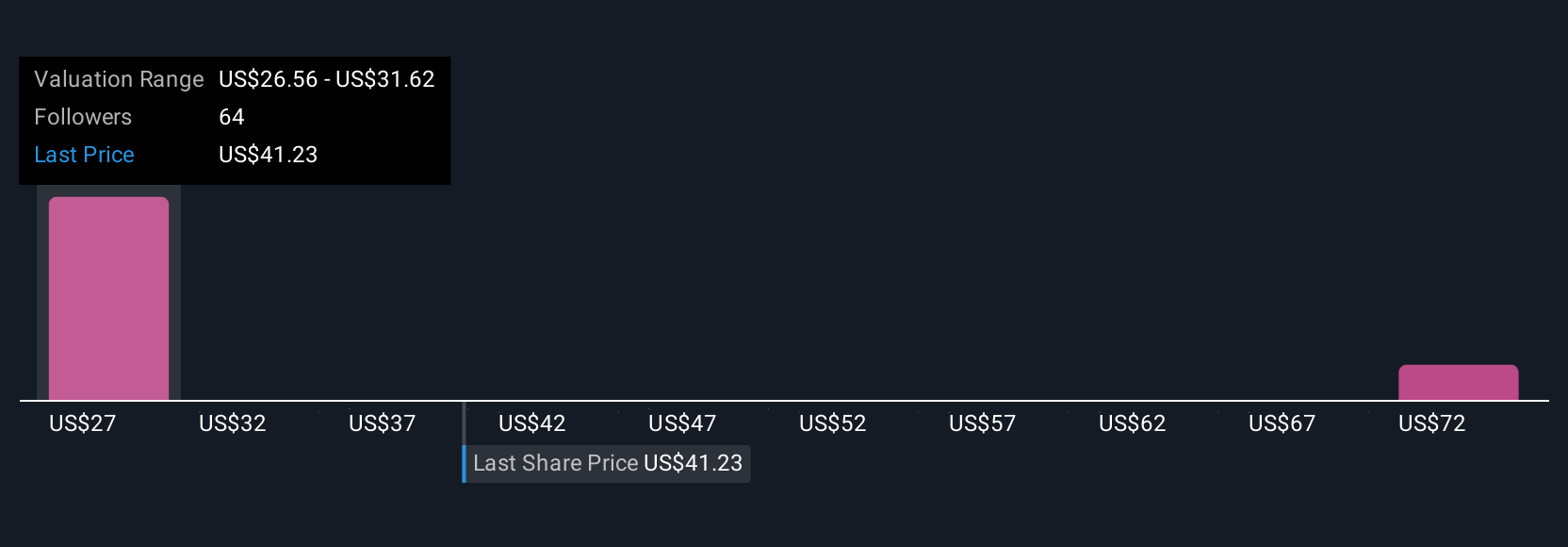

Uncover how Lemonade's forecasts yield a $49.62 fair value, a 30% downside to its current price.

Exploring Other Perspectives

Thirteen members of the Simply Wall St Community have offered fair value estimates for Lemonade that range widely from US$23.34 to US$77.14 per share. While community opinions differ, recent raised revenue guidance highlights how operational progress could influence broader expectations for Lemonade’s path to profitability.

Explore 13 other fair value estimates on Lemonade - why the stock might be worth less than half the current price!

Build Your Own Lemonade Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Lemonade research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Lemonade research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lemonade's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LMND

Lemonade

Provides various insurance products in the United States, Europe, and the United Kingdom.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor