Advertisement

- United States

- /

- Insurance

- /

- NasdaqGS:ROOT

Assessing Root (ROOT) Valuation After Recent Share Price Pullback and Longer-Term Gains

Root (ROOT) has quietly delivered a mixed run for shareholders, with gains this year but a drop over the past 3 months. That uneven performance is pushing investors to revisit its fundamentals.

See our latest analysis for Root.

The recent pullback, including a weak 90 day share price return, sits awkwardly against Root’s positive year to date share price gain and powerful three year total shareholder return. This suggests momentum has cooled while long term believers remain firmly in the green.

If Root’s swings have you reassessing your watchlist, this could be a good moment to explore fast growing stocks with high insider ownership as potential next wave candidates.

With Root now trading well below analyst targets despite solid revenue and earnings growth, investors have to ask: is this a mispriced turnaround still flying under the radar, or is the market already reflecting its future upside?

Most Popular Narrative Narrative: 35.4% Undervalued

With Root last closing at $80.39 against a narrative fair value of $124.40, the implied upside rests heavily on aggressive but specific growth assumptions.

The rapid iteration and deployment of Root's next-generation AI and machine learning pricing models have materially improved risk segmentation and increased customer lifetime value by over 20%, positioning the company to enhance future gross margins and net income as loss ratios improve.

Ongoing investment in data science capabilities and the ability to assimilate proliferating data sources enable Root to continuously refine their underwriting accuracy and claims efficiency, which is expected to contribute to improved loss ratios and operating leverage over time, bolstering future earnings.

Want to see how this pricing engine translates into a much richer future profit profile and premium valuation multiple, despite only modest headline growth expectations? Read on.

Result: Fair Value of $124.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upside rests on fragile foundations. Intensifying digital competition and potential regulatory shifts are both capable of quickly eroding Root’s margin and growth story.

Find out about the key risks to this Root narrative.

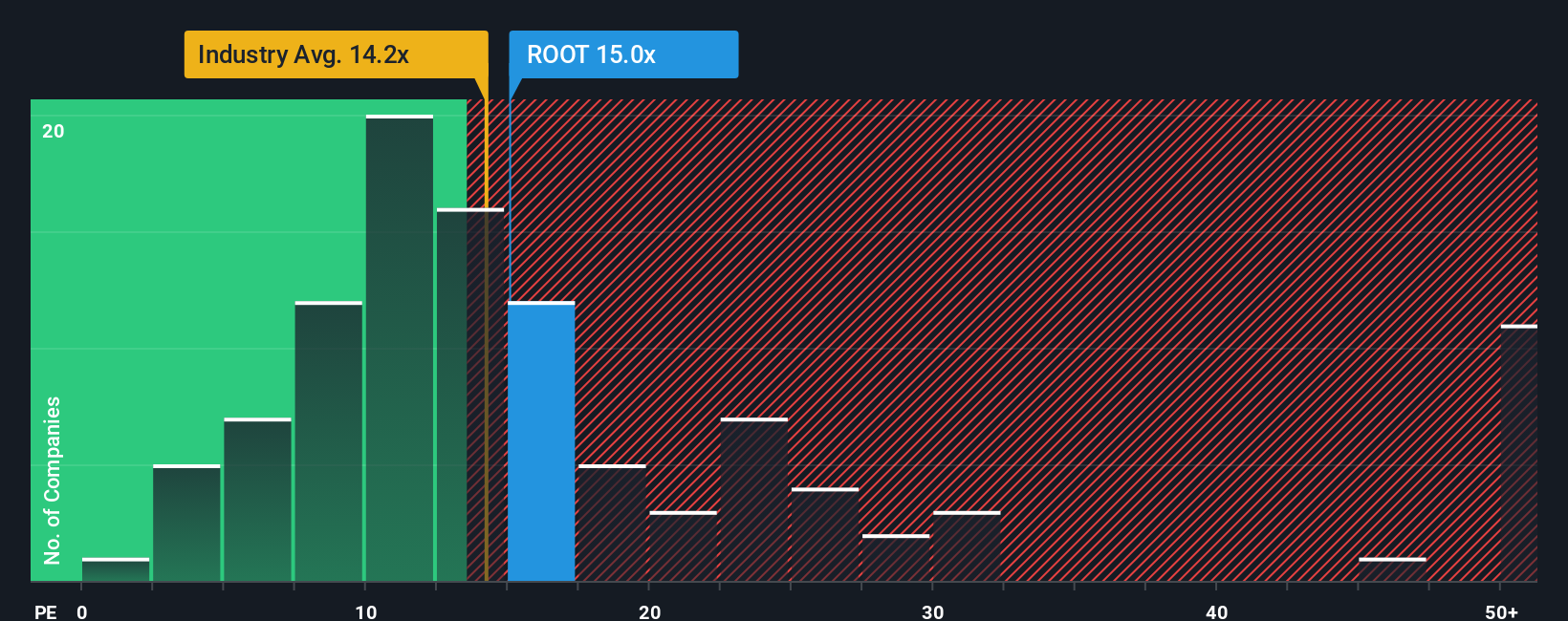

Another View on Value

While the narrative fair value points to upside, the basic earnings multiple tells a different story. Root trades on about 23 times earnings, far above its fair ratio of 15.7 times, the peer average of 12 times, and the US insurance industry at 12.8 times. That gap suggests valuation downside risk if sentiment or growth wobbles, so investors may be paying tomorrow’s price today.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Root Narrative

If you see the story differently or want to test your own assumptions against the numbers, you can build a complete narrative in minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Root.

Ready for your next investing move?

Root might be on your radar, but you will miss out on other high potential ideas if you stop here. Put the Simply Wall St Screener to work.

- Capture growth potential in cutting edge automation and intelligent platforms by scanning these 27 AI penny stocks shaping how data, software, and new technologies transform entire industries.

- Lock in income opportunities by reviewing these 15 dividend stocks with yields > 3% that can help anchor your portfolio with reliable cash flows in uncertain markets.

- Position yourself ahead of structural shifts in digital assets by tracking these 81 cryptocurrency and blockchain stocks aiming to benefit from blockchain adoption and new payment rails.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ROOT

Root

Provides insurance products and services in the United States.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5370.4% undervalued

37 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HegelBayeBagel on PlaySide Studios ·

PlaySide Studios: Market Is Sleeping on a Potential 10M+ Unit Breakout Year, FY26 Could Be the Rerate of the Decade

Fair Value:AU$0.8463.1% undervalued

10 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

AN

AnimalDoctorKwon on Inotiv ·

Inotiv NAMs Test Center

Fair Value:US$1.275.3% undervalued

20 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

TH

TheValueDetector on Cognyte Software ·

This isn’t speculation — this is confirmation.A Schedule 13G was filed, not a 13D, meaning this is passive institutional capital, not acti

Fair Value:US$95.6792.6% undervalued

31 followersusers have followed this narrative

2 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

HU

Humaninsights on Sezzle ·

Sezzle's Profits to Soar with 27% Margin Boost

Fair Value:US$113.1842.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Beacon Lighting Group ·

Beacon Trade and Vertical Integration leading Growth. However, economic headwinds and store rollouts could continue to fuel OpEx

Fair Value:AU$2.8110.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

alex30free on RaySearch Laboratories ·

High-Tech Precision Play

Fair Value:SEK 230.619.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.887.4% undervalued

59 followersusers have followed this narrative

5 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.0% undervalued

1281 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0225.7% undervalued

1077 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

Trending Discussion

TH

TheInvestingFool on PlaySide Studios ·

Looks interesting, I am jumping into the finances now. Your 15% margin seems high for a conservative model, can't just ignore the years they need to invest. You didnt seem to mention that they had to dilute the sharebase by issuing ~40mil shares. raising ~8 mil. should be enough if mouse does OK. If not they will need to raise more to suvive. Losing 20m a year, 14m after there 6m cutbacks. Am I reading it right that they have no debt. have they any history of raising debt? First look it is too dependant on the mouse and GoT games. they do well stock will 2-3x, poorly and it will drop. I am not sure I agree with your work for hire backstop. Unlikely meta horizons will continue with the same size contract going forward. say 10% margins and 15x multiple on 30m. that is 45m, which with the new sharecount is 10c. It is a backstop but maybe not that strong. Mouse fails and devs could start jumping ship and outside contracts could dry up. Hmm on top of all that AI could be disrupting the work for hire model. I think I have mostly talked myself out of it. Although Mouse looks good and does seem like the type of game that could go viral on twitch for a few months. If it does you will likly get a great return 5x plus. crap maybe I am talking myself back in.

1

|0

VF

vf220a on Impax Asset Management Group ·

Provided Very old data does not reflect current finantial and investment state of IAM .

0

|0