Advertisement

- United States

- /

- Household Products

- /

- NYSE:KMB

With Kimberly-Clark Corporation (NYSE:KMB) It Looks Like You'll Get What You Pay For

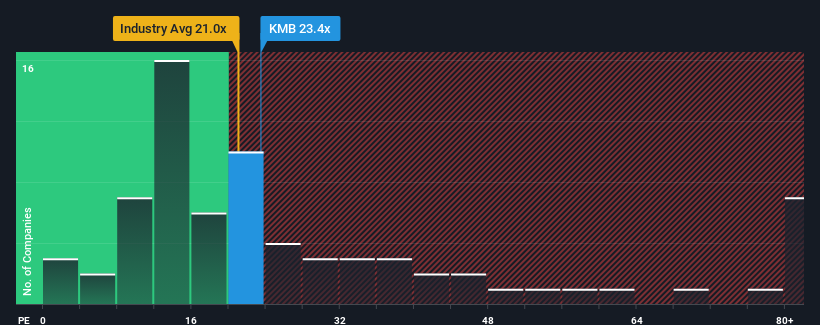

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 16x, you may consider Kimberly-Clark Corporation (NYSE:KMB) as a stock to potentially avoid with its 23.4x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

The recently shrinking earnings for Kimberly-Clark have been in line with the market. It might be that many expect the company's earnings to strengthen positively despite the tough market conditions, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Kimberly-Clark

Is There Enough Growth For Kimberly-Clark?

There's an inherent assumption that a company should outperform the market for P/E ratios like Kimberly-Clark's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 1.4% decrease to the company's bottom line. As a result, earnings from three years ago have also fallen 25% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 15% per annum during the coming three years according to the analysts following the company. That's shaping up to be materially higher than the 13% per annum growth forecast for the broader market.

In light of this, it's understandable that Kimberly-Clark's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Kimberly-Clark's P/E?

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Kimberly-Clark's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Before you settle on your opinion, we've discovered 3 warning signs for Kimberly-Clark that you should be aware of.

Of course, you might also be able to find a better stock than Kimberly-Clark. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Kimberly-Clark might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:KMB

Kimberly-Clark

Manufactures and markets personal care products in the United States.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|41.9% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|31.9% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|24.9% undervalued

MA

Community Contributor