- United States

- /

- Medical Equipment

- /

- NYSE:PEN

Penumbra (NYSE:PEN) Announces Retirement Of Long-Serving Board Member Don Kassing

Reviewed by Simply Wall St

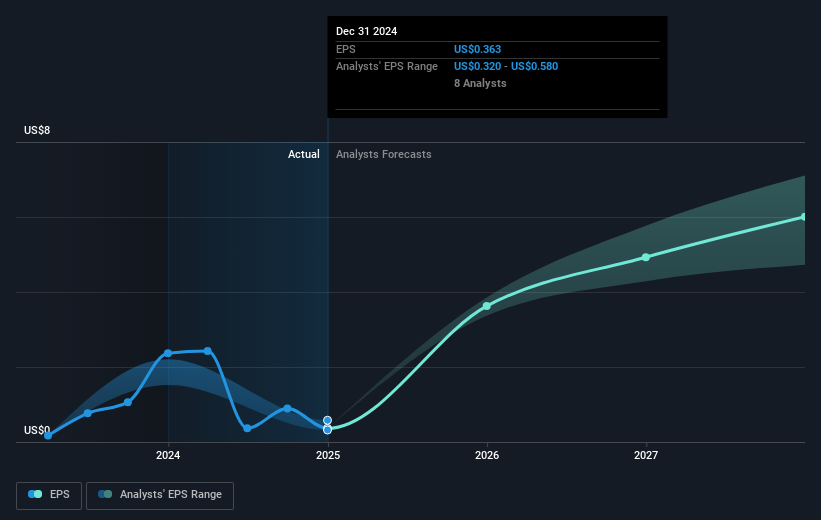

Penumbra (NYSE:PEN) experienced a 19% price increase over the last quarter, primarily driven by strategic corporate decisions and an evolving market landscape. The retirement announcement of Don Kassing, a longstanding board member, raised expectations for potential strategic shifts at the company. During this period, Penumbra also reported its fourth-quarter and full-year earnings, revealing increased sales but a significant drop in net income, indicating challenges in profitability. Despite a broader market decline driven by economic data and negative performances in sectors like healthcare and tech, Penumbra's proactive projections for 2025 revenue growth, ranging between 12% and 14%, supported investor confidence. This optimistic outlook seemingly insulated Penumbra's share price from the adverse market trends, positioning it as a resilient player amidst a volatile trading landscape.

Unlock comprehensive insights into our analysis of Penumbra stock here.

Over the past five years, Penumbra's shares have delivered a total return of 75.86%. A key factor in this trajectory has been the company's ability to achieve significant earnings growth, averaging 22.5% annually over this period until 2024. Additionally, Penumbra's foresight in anticipating revenue growth, reflected in corporate guidance updates such as the October 2024 forecast of 2025 revenue growth between 12% and 14%, has been critical. The company's capability to innovate, as demonstrated by events like the FDA clearance and launch of the Lightning Flash 2.0 thrombectomy system in April 2024, has also been influential in maintaining investor interest.

Penumbra's enhanced capital management has further played a part, with the completion of a $100 million share buyback program by September 2024. Despite facing challenges, such as a large one-off loss impacting its 2024 financial results, Penumbra managed to outperform both the US market and the Medical Equipment industry over the past year, showcasing resilience amidst fluctuations.

- Analyze Penumbra's fair value against its market price in our detailed valuation report—access it here.

- Analyze the downside risks for Penumbra and understand their potential impact—click to learn more.

- Got skin in the game with Penumbra? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PEN

Penumbra

Designs, develops, manufactures, and markets medical devices in the United States and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives