- United States

- /

- Healthcare Services

- /

- OTCPK:NVTA.Q

Cautious Investors Not Rewarding Invitae Corporation's (NYSE:NVTA) Performance Completely

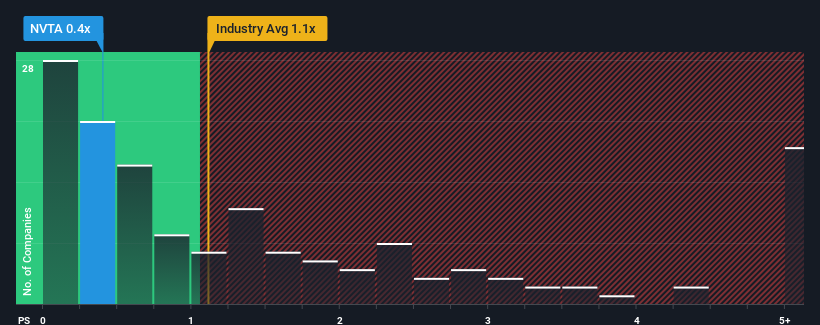

When you see that almost half of the companies in the Healthcare industry in the United States have price-to-sales ratios (or "P/S") above 1.1x, Invitae Corporation (NYSE:NVTA) looks to be giving off some buy signals with its 0.4x P/S ratio. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Invitae

What Does Invitae's Recent Performance Look Like?

Invitae hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. It seems that many are expecting the poor revenue performance to persist, which has repressed the P/S ratio. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Invitae.How Is Invitae's Revenue Growth Trending?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Invitae's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 7.4% decrease to the company's top line. Even so, admirably revenue has lifted 96% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 7.1% each year during the coming three years according to the nine analysts following the company. That's shaping up to be similar to the 7.7% per year growth forecast for the broader industry.

With this in consideration, we find it intriguing that Invitae's P/S is lagging behind its industry peers. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

What We Can Learn From Invitae's P/S?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've seen that Invitae currently trades on a lower than expected P/S since its forecast growth is in line with the wider industry. When we see middle-of-the-road revenue growth like this, we assume it must be the potential risks that are what is placing pressure on the P/S ratio. Perhaps investors are concerned that the company could underperform against the forecasts over the near term.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 5 warning signs with Invitae (at least 3 which shouldn't be ignored), and understanding them should be part of your investment process.

If these risks are making you reconsider your opinion on Invitae, explore our interactive list of high quality stocks to get an idea of what else is out there.

If you're looking to trade Invitae, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:NVTA.Q

Invitae

A medical genetics company, that provides genetic information to improve healthcare of people in the United States, Canada, and internationally.

Medium-low and slightly overvalued.

Similar Companies

Market Insights

Community Narratives