Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:HUM

Will Humana's (HUM) Medicare Advantage Retreat Signal a Shift in Its Long-Term Growth Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- In the past week, Humana announced it will reduce its Medicare Advantage footprint from 48 to 46 states in 2026, citing rising medical costs and pressures from government reimbursements.

- This shift highlights an industry-wide retreat among insurers from less profitable markets, reflecting broader challenges in managing growing healthcare expenditures and regulatory headwinds.

- We'll explore how Humana's decision to scale back Medicare Advantage offerings could shape its investment narrative and future growth outlook.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Humana Investment Narrative Recap

To own shares in Humana, investors must believe in the company’s ability to deliver profitable growth from Medicare Advantage while navigating regulatory complexity and medical cost pressures. The latest announcement about pulling back Medicare Advantage coverage to 46 states is not expected to materially impact the biggest short-term catalyst, a focus on clinical excellence and value-based care, but it highlights that the primary risk remains unpredictable reimbursement rates and cost headwinds. Overall, the move reinforces the sector’s challenges and doesn’t significantly change Humana’s risk-return story near term.

Among Humana’s recent updates, its expanded partnership with TailorCare stands out for its relevance; this expansion will provide Medicare Advantage members access to comprehensive musculoskeletal care in new regions, supporting better health outcomes and cost control. The initiative directly supports Humana’s emphasis on value-based care and enhanced member engagement, which is vital for achieving strong Stars ratings and improving earnings over time.

However, investors should keep in mind that, in contrast to growth headlines, ongoing litigation and regulatory pressures could impact future profitability and...

Read the full narrative on Humana (it's free!)

Humana's narrative projects $150.9 billion revenue and $3.3 billion earnings by 2028. This requires 7.0% yearly revenue growth and a $1.7 billion earnings increase from $1.6 billion today.

Uncover how Humana's forecasts yield a $298.95 fair value, a 16% upside to its current price.

Exploring Other Perspectives

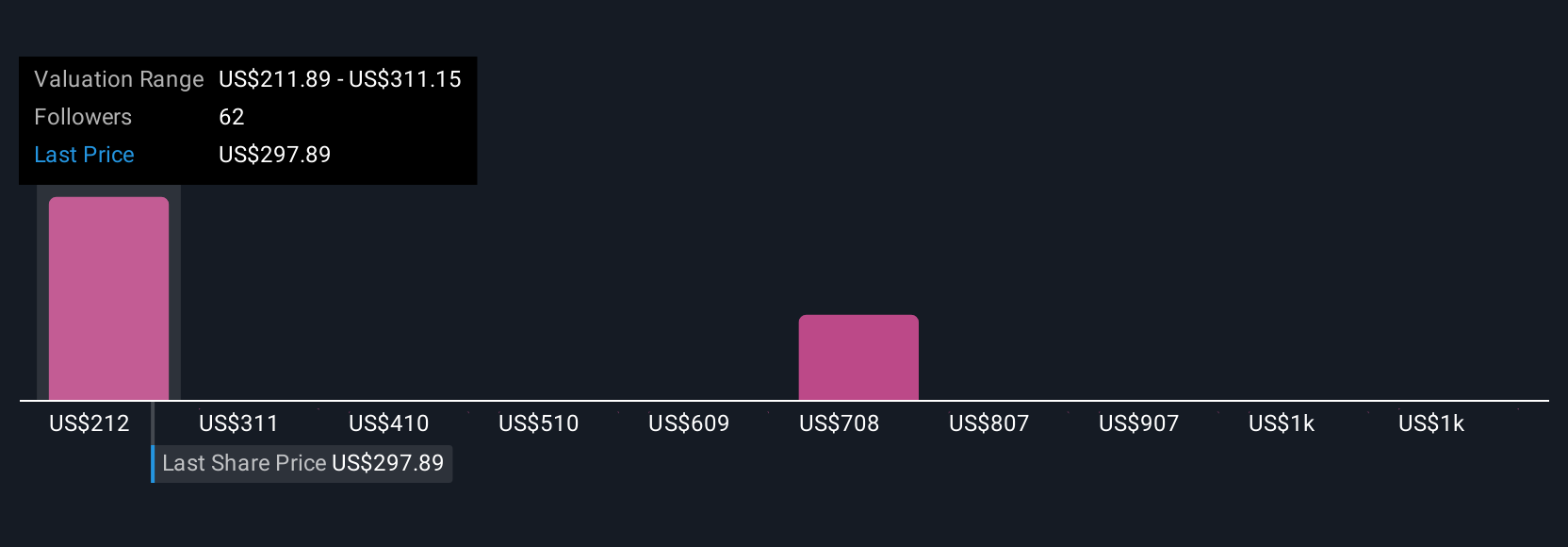

Simply Wall St Community members submitted 11 fair value estimates for Humana, ranging from US$211.89 to an ambitious US$1,204.45 per share. Opinions on growth potential are wide ranging, especially given concerns around Humana’s exposure to fluctuating government reimbursements and medical costs, so consider several viewpoints before deciding where you stand.

Explore 11 other fair value estimates on Humana - why the stock might be worth 17% less than the current price!

Build Your Own Humana Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Humana research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Humana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Humana's overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Humana might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HUM

Humana

Provides medical and specialty insurance products in the United States.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor