Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:HCA

HCA Healthcare (HCA): Valuation Spotlight After Affordable Care Act Subsidy Extension News

Simply Wall St

Reviewed by Simply Wall St

HCA Healthcare (HCA) shares rose 3% after reports that the Trump administration may extend Affordable Care Act subsidies for two more years. This move could ease regulatory uncertainty and boost revenue visibility for hospital operators.

See our latest analysis for HCA Healthcare.

The recent news about potential Affordable Care Act subsidy extensions sparked a strong rally in HCA Healthcare’s stock, building on an already impressive run this year. In addition to operational expansions and new hospital launches, investor enthusiasm is fueled by reduced policy uncertainty. This has led to fresh optimism around HCA’s future performance. Overall, HCA’s share price has climbed more than 70% year-to-date, with a 56.6% total shareholder return over the past year. This indicates that positive momentum is building for the company.

If you’re watching how healthcare stocks are responding to policy developments, now is an ideal time to explore the wider set of opportunities through our See the full list for free.

With the stock already up more than 70% this year, investors may be wondering whether HCA Healthcare is still undervalued or if the market has already factored in all of the company’s future growth potential. Is there still a compelling buying opportunity here, or have recent gains fully priced in the good news?

Most Popular Narrative: 6% Overvalued

Compared to HCA Healthcare’s last close price of $508.29, the most widely followed narrative estimates fair value at $477.70 per share. This sets the stage for key questions about what drives this premium.

Supplemental payment approvals and increased state-directed payments are viewed as material tailwinds that support higher revenue and contribute to robust medium-term growth estimates. The company's commitment to long-term volume growth targets and stable hospital utilization is considered favorably, supporting confidence in operational execution.

Wondering what bold forecasts support this pricing? The narrative relies on a precise mix of expanding revenues and anticipated strength in future earnings. The profitability forecast may surprise you. Interested in the details behind HCA’s valuation logic? Explore the full story to uncover the unique blend of growth and margin assumptions at play.

Result: Fair Value of $477.70 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent policy uncertainty and potential changes in supplemental payments could present challenges for HCA Healthcare’s revenue growth trajectory in the quarters ahead.

Find out about the key risks to this HCA Healthcare narrative.

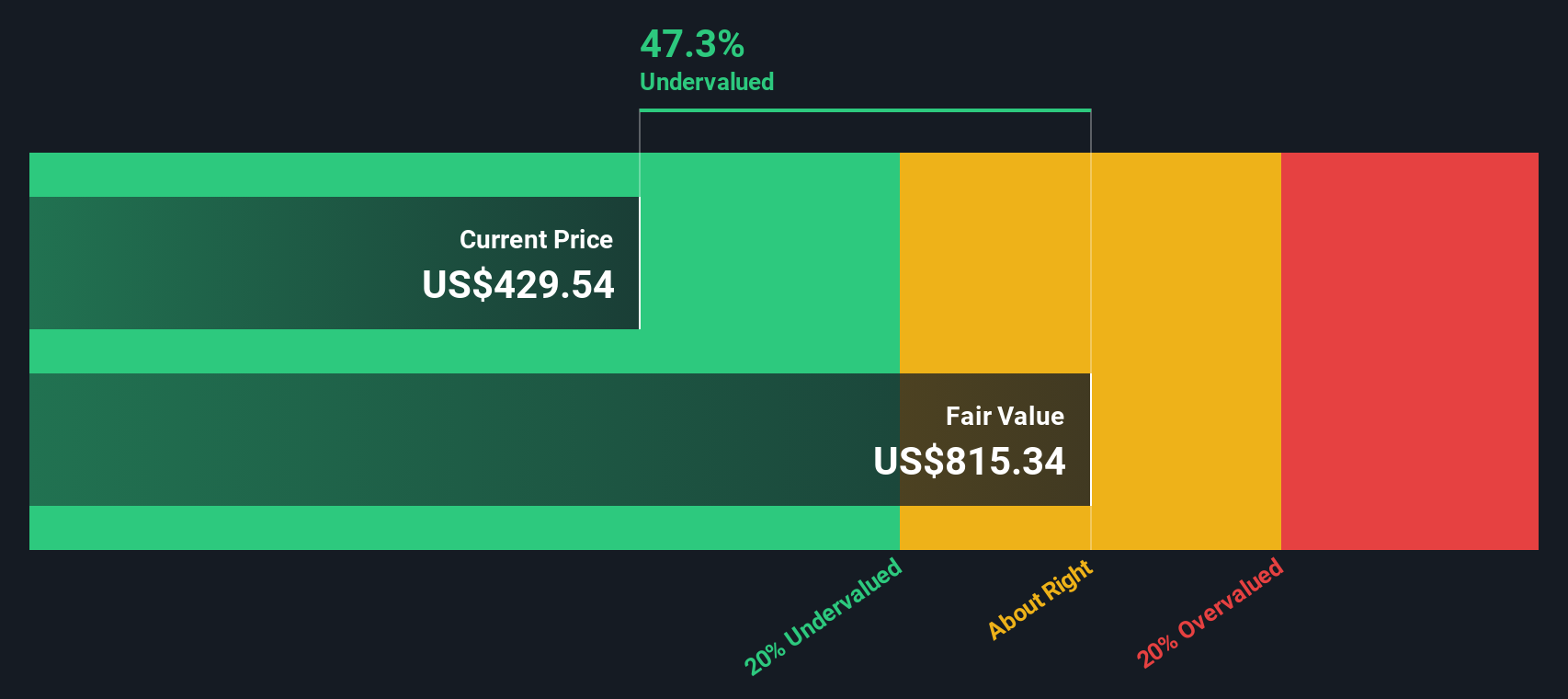

Another View: Discounted Cash Flow Suggests Upside

The SWS DCF model takes a different approach than the market pricing narrative and points to a much higher fair value. It estimates HCA Healthcare shares are trading about 43.5% below what intrinsic cash flows could justify. This notable difference raises questions about whether recent price gains already reflect the company’s true potential, or if additional value may be present that is not yet recognized.

Look into how the SWS DCF model arrives at its fair value.

Build Your Own HCA Healthcare Narrative

If you believe there is more to HCA Healthcare’s story or want to put your own analysis to the test, the tools are here to help you craft a personalized assessment in just a few minutes. Do it your way

A great starting point for your HCA Healthcare research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors stay ahead with fresh opportunities. Don’t miss your chance to find market-beating ideas others overlook before the spotlight turns their way.

- Tap into the momentum of artificial intelligence with these 25 AI penny stocks, which is powering disruptive innovations across industries and reshaping the business landscape.

- Secure reliable income streams by checking out these 15 dividend stocks with yields > 3%, which offers yields above 3% and shows strong fundamentals for long-term growth.

- Position yourself early in the quantum computing wave through these 28 quantum computing stocks, where cutting-edge breakthroughs could drive the next technology boom.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HCA Healthcare might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HCA

HCA Healthcare

Through its subsidiaries, owns and operates hospitals and related healthcare entities in the United States.

Undervalued with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative