- United States

- /

- Medical Equipment

- /

- NYSE:GMED

Globus Medical (NYSE:GMED) Reports Strong Sales Growth But Sees US$20 Million Dip In Annual Net Income

Reviewed by Simply Wall St

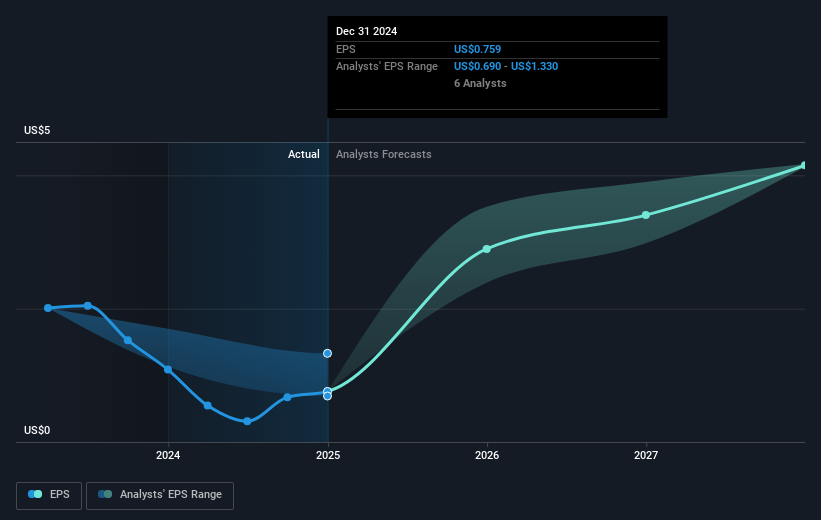

Globus Medical (NYSE:GMED) recently reported mixed financial results, with a significant rise in sales to USD 2,519 million but a drop in net income to USD 103 million for the full year ending December 2024. The company's share price exhibited a minor shift of 0.01% in the past week, occurring amidst broader market fluctuations that saw major indexes like the Dow Jones and Nasdaq experience declines due to factors including the UnitedHealth DOJ probe and tech stock performance. While Globus Medical's quarterly performance showed substantial gains in net income, the overall decline in full-year earnings and EPS could contribute to stagnant investor sentiment. This aligns with the market's subdued activity, where external market pressures and a slight pullback in key indexes have been observed. This environment suggests that while Globus's operational growth is evident, broader market uncertainties could influence its recent minimal price change.

See the full analysis report here for a deeper understanding of Globus Medical.

Globus Medical's total shareholder return over the past five years was 77.92%, reflecting a strong performance amidst varied financial landscapes. Despite a recent one-year period where it surpassed both the US Market and the US Medical Equipment industry with a robust 23.7% return, several factors shaped its longer-term trajectory. Notably, significant corporate developments such as the completion of a substantial share repurchase program in early 2024 fueled investor interest, returning US$225.59 million to shareholders. Additionally, steadily rising revenue guidance announced in 2024 culminated in an anticipated increase to between US$2.66 billion and US$2.69 billion for 2025, signaling potential growth despite challenges.

The company's recent acquisition of Nevro, finalizing an agreement in February 2025, also expanded its portfolio, positioning Globus for future scalability. This bold move, coupled with product innovations and enhanced financial reporting, reflects an ongoing commitment to growth, albeit tempered by market fluctuations and a recent dip in net income. These strategic decisions have undoubtedly influenced its half-decade success.

- See how Globus Medical measures up with our analysis of its intrinsic value versus market price.

- Assess the potential risks impacting Globus Medical's growth trajectory—explore our risk evaluation report.

- Already own Globus Medical? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GMED

Globus Medical

A medical device company, develops and commercializes healthcare solutions for patients with musculoskeletal disorders in the United States and internationally.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Community Narratives