- United States

- /

- Healthcare Services

- /

- NYSE:CVS

CVS Health (NYSE:CVS) Reports Revenue Growth But Lowers Full-Year Earnings Guidance

Reviewed by Simply Wall St

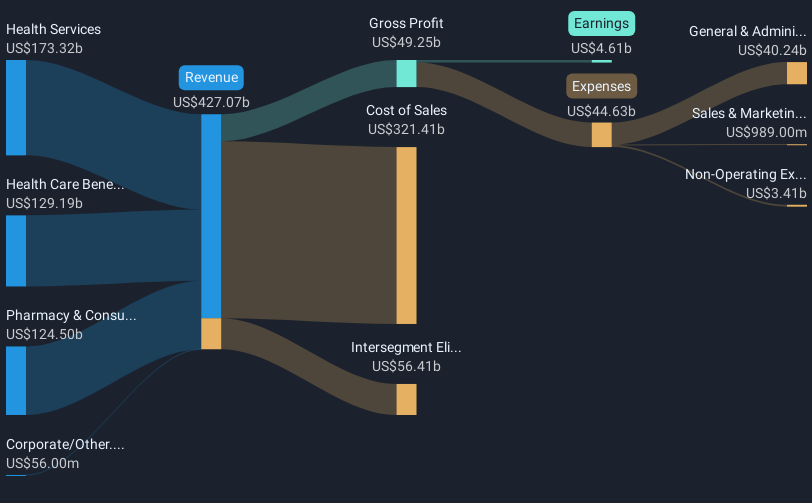

CVS Health (NYSE:CVS) reported robust year-over-year growth in Q1 2025 earnings, with significant increases in sales, revenue, and net income, though the company adjusted its annual earnings guidance downward. This financial performance, coupled with market trends where major indices including the S&P 500 and Dow continued their upward trajectory, likely contributed to the company's 17% share price increase over the last quarter. While broader market gains were supported by strong tech earnings, CVS's positive Q1 results and executive changes may have added weight to these overall market dynamics.

We've spotted 2 weaknesses for CVS Health you should be aware of, and 1 of them is concerning.

The recent report of strong Q1 2025 earnings growth for CVS Health, despite a downward adjustment in the annual guidance, provides an intriguing context for the company's strategic narrative. With advancements in integrated capabilities like Aetna's recovery, the drive towards affordable healthcare could result in improved margins and earnings. The prior earnings increase and executive changes might influence analysts' forecasts, potentially impacting assumptions of a US$5.0 billion revenue increase to US$429.4 billion by 2028 and earnings reaching US$8.3 billion. While these factors offer a lens to assess future performance, the adjustments to earnings guidance could moderate optimism over expected profit margin expansions.

Over the past five years, CVS Health's total shareholder returns, including dividends, reached 29.49%—a moderate gain that provides a context for its longer-term resilience. However, annual performance comparisons show that CVS's returns exceeded the broader US market and the Healthcare industry, highlighting its relative short-term strength. The consensus analyst price target of US$76.13 implies a 14.6% upside from the current price of US$65.03, indicating some analysts see potential for further appreciation. Investors may consider this price target within the context of the broader market dynamics and the company's strategic efforts to enhance digital strategies and biosimilar market presence.

Assess CVS Health's previous results with our detailed historical performance reports.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CVS

Undervalued established dividend payer.

Similar Companies

Market Insights

Community Narratives