Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:CI

Does Cigna Offer Value After Pharmacy Benefit Business Shakeup and Share Price Drop?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Cigna Group is trading at a bargain or priced for perfection? If questions about the stock’s value have been on your mind, you’re in good company.

- The share price has been somewhat volatile lately, edging up 0.1% over the past week but down 6.9% in the last month, with a modest 1.4% year-to-date gain and a 39.0% return over five years.

- In the news, Cigna has been attracting attention after announcing significant changes to its pharmacy benefit management business and strategic partnerships. These developments have generated renewed investor interest and shifted sentiment about the company’s long-term direction.

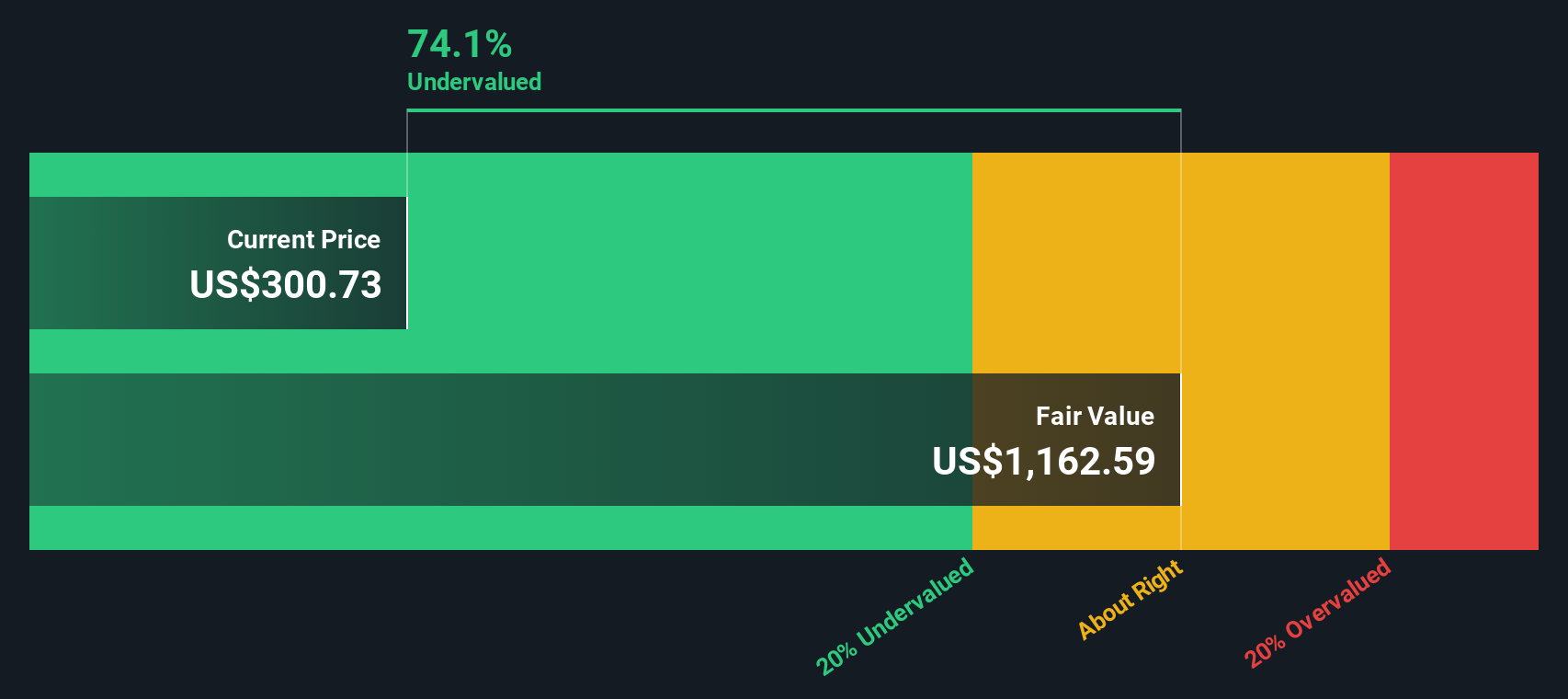

- The numbers matter too. Cigna Group currently scores a 5 out of 6 on our undervaluation checks, which suggests it may be undervalued in most key areas. Next, we'll break down the different ways to evaluate that score, and provide a smarter approach to valuation at the end of this article.

Approach 1: Cigna Group Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and then discounting them back to their present value. This approach allows investors to assess what a business is truly worth today, based on the cash it is expected to generate in the years ahead.

Cigna Group's latest reported Free Cash Flow stands at $7.03 Billion. Analyst forecasts project strong growth, with Free Cash Flow expected to reach $11.24 Billion by 2029. While analysts provide estimates for the next few years, Simply Wall St extends these projections to ensure a complete valuation picture for the company. All figures and calculations here are reported in US dollars.

The DCF model indicates an intrinsic fair value of $1,025.26 per share. Compared to the stock's current trading price, this means Cigna Group is trading at a 72.9% discount to its estimated intrinsic value, which suggests the shares are significantly undervalued based on projected cash flows.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Cigna Group is undervalued by 72.9%. Track this in your watchlist or portfolio, or discover 923 more undervalued stocks based on cash flows.

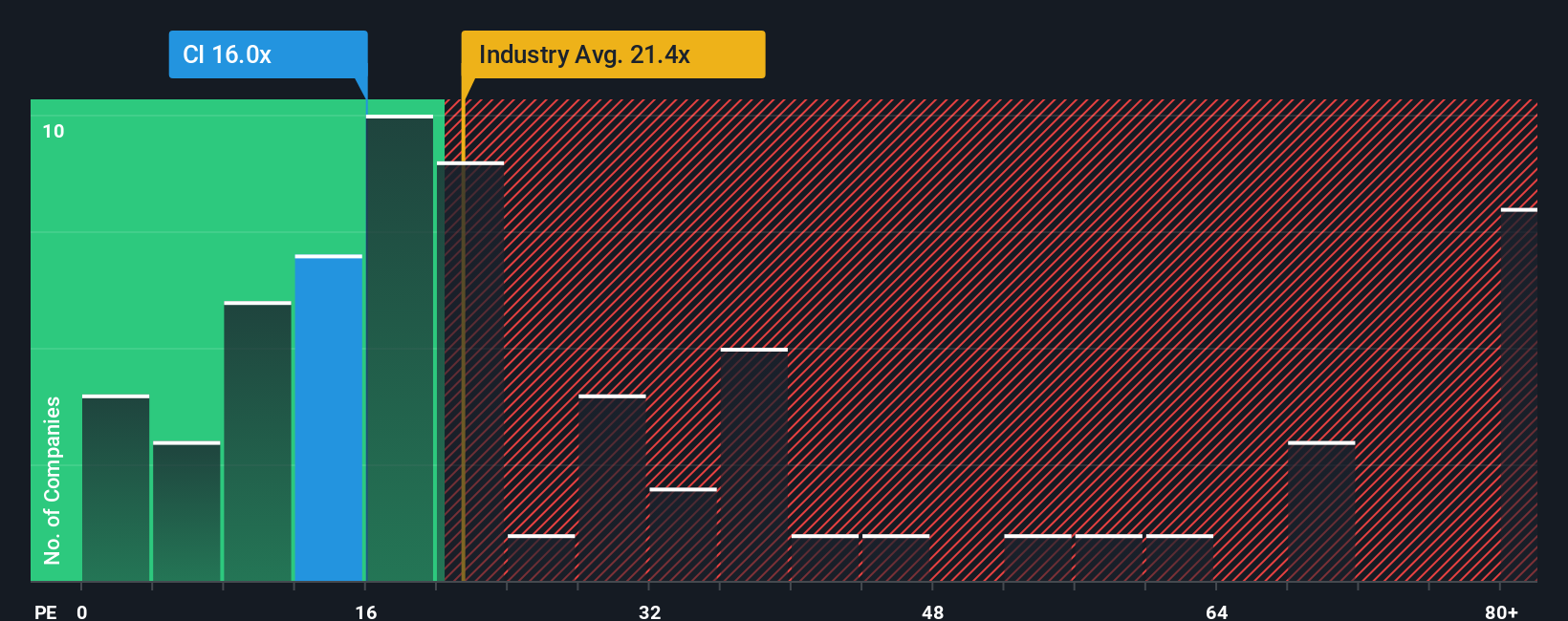

Approach 2: Cigna Group Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies because it helps investors gauge how much they are paying for each dollar of a company's earnings. When a business like Cigna Group is consistently profitable, the PE ratio provides a clear indication of whether its stock is affordable compared to its current and expected earnings power.

It is important to note that higher growth expectations typically justify higher PE ratios, while greater risks or slower growth tend to push the fair ratio lower. Therefore, what is considered a reasonable PE ratio depends on how much growth investors expect from the company and its overall risk profile.

Cigna Group currently trades at a PE of 12.1x, which is well below the healthcare industry average of 22.8x and its peer group average of 31.8x. This may initially suggest that the stock is undervalued relative to the broader sector and similar companies. However, using Simply Wall St’s proprietary “Fair Ratio”, which for Cigna Group is 28.6x, provides a more tailored benchmark. The Fair Ratio is designed to account for the company’s specific growth outlook, profit margins, market cap, and industry dynamics, making it a more meaningful indicator than simply comparing with peers or sector averages.

Comparing the current PE to this Fair Ratio, it is clear that Cigna Group’s shares are trading at a substantial discount by this measure. This indicates that, based on its earnings potential and fundamentals, the stock could be considered significantly undervalued at present levels.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Cigna Group Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. Narratives are a simple, yet powerful way to connect a company’s story, such as its business model, risks, and market drivers, to a financial forecast and then to a fair value estimate. Instead of relying solely on broad ratios or analyst consensus, Narratives let you bring your own perspective and assumptions to the table by outlining how you expect Cigna Group’s revenue, earnings, and margins to change.

On Simply Wall St’s Community page, Narratives are easy to use and trusted by millions of investors. They show you how your view of Cigna Group’s future growth and risks translates, mathematically, into a fair value and whether the current share price is above or below that value. This lets you make clear decisions about timing, backed by your reasoning rather than generic benchmarks.

Narratives also stay up to date automatically as new developments, like earnings releases or news, emerge so your investment story always reflects the latest information.

For example, some investors currently forecast Cigna Group’s fair value as high as $428.00 per share if they expect aggressive revenue growth and margin expansion, while others are much more cautious, seeing fair value at only $300.00. Your Narrative helps you decide where you stand and what action to take.

Do you think there's more to the story for Cigna Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CI

Cigna Group

Provides insurance and related products and services in the United States.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

95 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative