- United States

- /

- Healthcare Services

- /

- NYSE:AMN

AMN Healthcare Services, Inc. (NYSE:AMN) Looks Inexpensive After Falling 27% But Perhaps Not Attractive Enough

AMN Healthcare Services, Inc. (NYSE:AMN) shareholders won't be pleased to see that the share price has had a very rough month, dropping 27% and undoing the prior period's positive performance. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 40% share price drop.

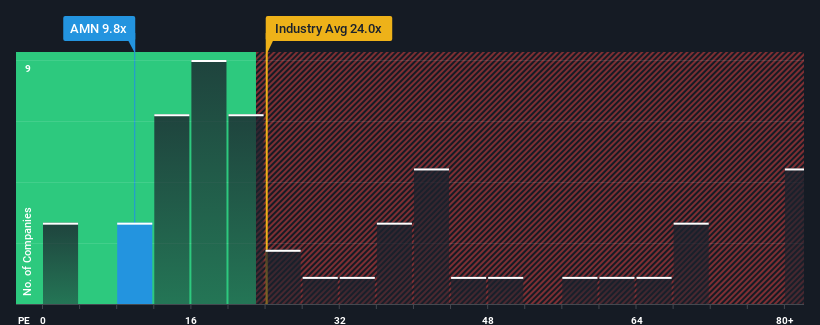

Although its price has dipped substantially, AMN Healthcare Services may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 9.8x, since almost half of all companies in the United States have P/E ratios greater than 17x and even P/E's higher than 32x are not unusual. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Recent times haven't been advantageous for AMN Healthcare Services as its earnings have been falling quicker than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

View our latest analysis for AMN Healthcare Services

How Is AMN Healthcare Services' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as low as AMN Healthcare Services' is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered a frustrating 46% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 274% overall rise in EPS, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to slump, contracting by 15% per annum during the coming three years according to the nine analysts following the company. That's not great when the rest of the market is expected to grow by 10% per year.

With this information, we are not surprised that AMN Healthcare Services is trading at a P/E lower than the market. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Key Takeaway

AMN Healthcare Services' recently weak share price has pulled its P/E below most other companies. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of AMN Healthcare Services' analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with AMN Healthcare Services, and understanding them should be part of your investment process.

Of course, you might also be able to find a better stock than AMN Healthcare Services. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

If you're looking to trade AMN Healthcare Services, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:AMN

AMN Healthcare Services

Provides healthcare workforce solutions and staffing services to acute and sub-acute care hospitals and other healthcare facilities in the United States.

Undervalued with imperfect balance sheet.