- United States

- /

- Medical Equipment

- /

- NasdaqGM:STIM

Market Cool On Neuronetics, Inc.'s (NASDAQ:STIM) Revenues Pushing Shares 36% Lower

Neuronetics, Inc. (NASDAQ:STIM) shareholders won't be pleased to see that the share price has had a very rough month, dropping 36% and undoing the prior period's positive performance. Longer-term shareholders would now have taken a real hit with the stock declining 7.1% in the last year.

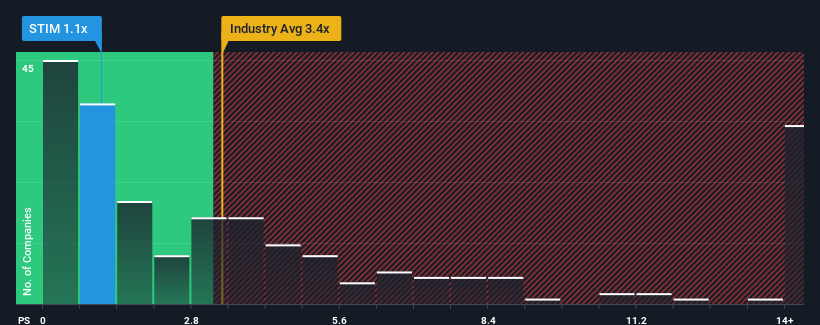

Since its price has dipped substantially, Neuronetics' price-to-sales (or "P/S") ratio of 1.1x might make it look like a strong buy right now compared to the wider Medical Equipment industry in the United States, where around half of the companies have P/S ratios above 3.4x and even P/S above 7x are quite common. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Neuronetics

How Has Neuronetics Performed Recently?

Neuronetics' revenue growth of late has been pretty similar to most other companies. It might be that many expect the mediocre revenue performance to degrade, which has repressed the P/S ratio. If not, then existing shareholders have reason to be optimistic about the future direction of the share price.

Keen to find out how analysts think Neuronetics' future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The Low P/S Ratio?

In order to justify its P/S ratio, Neuronetics would need to produce anemic growth that's substantially trailing the industry.

Retrospectively, the last year delivered a decent 9.4% gain to the company's revenues. Pleasingly, revenue has also lifted 45% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenues over that time.

Turning to the outlook, the next three years should generate growth of 13% per annum as estimated by the four analysts watching the company. Meanwhile, the rest of the industry is forecast to only expand by 10% each year, which is noticeably less attractive.

With this in consideration, we find it intriguing that Neuronetics' P/S sits behind most of its industry peers. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Final Word

Having almost fallen off a cliff, Neuronetics' share price has pulled its P/S way down as well. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

A look at Neuronetics' revenues reveals that, despite glowing future growth forecasts, its P/S is much lower than we'd expect. When we see strong growth forecasts like this, we can only assume potential risks are what might be placing significant pressure on the P/S ratio. It appears the market could be anticipating revenue instability, because these conditions should normally provide a boost to the share price.

Having said that, be aware Neuronetics is showing 5 warning signs in our investment analysis, you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

If you're looking to trade Neuronetics, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Neuronetics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:STIM

Neuronetics

A commercial stage medical technology company, designs, develops, and markets products for patients with neurohealth disorders in the United States and internationally.

Slight with mediocre balance sheet.