Advertisement

- United States

- /

- Medical Equipment

- /

- OTCPK:SDCC.Q

SmileDirectClub's (NASDAQ:SDC) Cash Burn Situation is Getting Better - But Not Good Enough for a Short-squeeze

It might be hard to believe at the moment, but SmileDirectClub ( NASDAQ: SDC ) was initially valued at over US$8b.

After a fiasco IPO debut that saw the price decline at over 50%, the stock just started to recover when the 2020 pandemic hit, sending it to a fresh new low.

Since then, the company has struggled through disappointing earnings and currently trades near the lows. As SDC remains unprofitable, this article will examine its cash burn situation.

Q2 Results and Downgrades

- Q2 GAAP EPS : -US$0.14 (miss by US$0.04)

- Revenue: US$ 174m (miss by US$24.52m)

- FY Guidance: US$750m-800m (consensus US$833.43m)

Disappointing results prompted analysts to issue another downgrade , as JP Morgan now sees it as Underweight. This is their second downgrade in less than 3 months, after already dropping to Neutral in May.

Meanwhile, the company has lost a bid for a patent on teledentistry technology. The U.S. Court of Appeals for the Federal Circuit affirmed Delaware's federal judge's decision to rule the patent invalid. Yet, the legal battle with the NYC-based competitor Candid Care Co. continues in regards to other patents.

Interestingly, this is not the first time the company has been in a legal skirmish, as it previously won the dispute against the former partner, and a current competitor, Align Technology (NASDAQ: ALGN)

A Short Squeeze Candidate?

3 catalysts make a perfect short-squeeze storm

- High % short of the float

- Unusual options activity – out-of-the-money (OTM) calls

- Positive News Catalyst

With all the negative catalysts, it doesn't surprise to see the stock heavily shorted, as high as 32.73% of the float.

However, the stock lacks a positive fundamental catalyst needed for such a turnaround, as the CEO unconvincingly stated that he wouldn't be buying any more shares. Furthermore, the stock is not ringing alarm bells on the popular unusual options activity trackers just yet.

Cash Burn Outlook

Given the risk, we thought we'd look at whether the shareholders should be worried about its cash burn.For this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow.We'll start by comparing its cash burn with its cash reserves to calculate its cash runway.

See our latest analysis for SmileDirectClub .

SmileDirectClub's Cash Runway

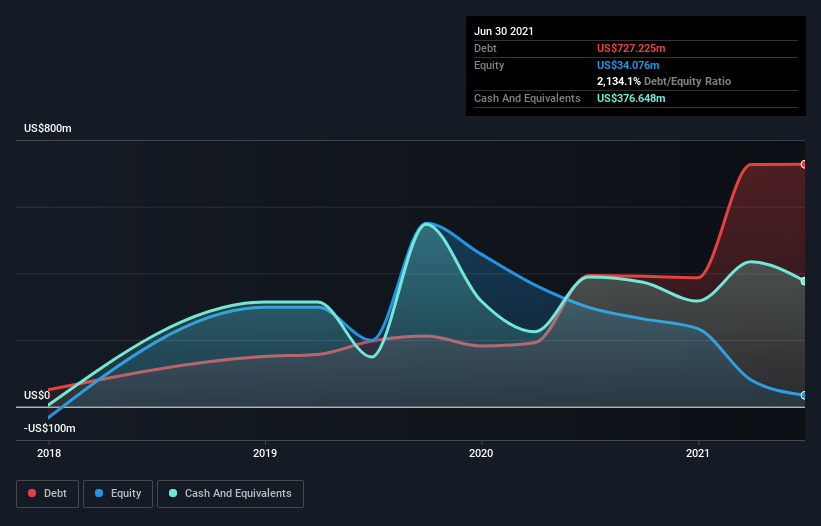

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate.As of June 2021, SmileDirectClub had cash of US$377m but also US$163.50m in short-term liabilities.In the last year, its cash burn was US$152m.

Importantly, analysts think that SmileDirectClub will reach cash flow breakeven in 4 years.

Essentially, that means the company will either reduce its cash burn or else require more cash.You can see how its cash balance has changed over time in the image below.

How Well Is SmileDirectClub Growing?

SmileDirectClub is moving in the right direction regarding its cash burn, which is down 65% over the last year.And it could also show revenue growth of 7.8% in the same period.

Clearly, however, the crucial factor is whether the company will grow its business in the future. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company .

How Hard Would It Be For SmileDirectClub To Raise More Cash For Growth?

Generally speaking, a listed business can raise new cash through issuing shares or taking on debt.Commonly, a business will sell new shares in itself to raise cash and drive growth.We can compare a company's cash burn to its market capitalization to see how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalization of US$2.1b, SmileDirectClub's US$152m in cash burn equates to about 7.3% of its market value.Given that it is a rather small percentage, it would probably be effortless for the company to fund another year's growth by issuing some new shares to investors or even taking out a loan.

Conclusion

There are two sides to the coin. First of all, the cash burn has been getting better, and the company has been growing its revenues.

However, the balance sheet shows a substantial amount of debt , and shareholders will likely face dilution at some point down the road. Dilution at this valuation would be disastrous. Therefore we can conclude that this is the time for management to step up and deliver a positive fundamental catalyst. Something that will lift the price and release the pressure of the shorts.

Who knows, if the teeth align, SDC just might become the next retail speculator darling.

Readers need to have a sound understanding of business risks before investing in a stock, and we've spotted 2 warning signs for SmileDirectClub that potential shareholders should take into account before putting money into a stock.

Of course, SmileDirectClub may not be the best stock to buy . So you may wish to see this free collection of companies boasting high return on equity or this list of stocks that insiders are buying .

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About OTCPK:SDCC.Q

SmileDirectClub

SmileDirectClub, Inc., an oral care company, offers clear aligner therapy treatment.

Fair value with concerning outlook.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor