Advertisement

- United States

- /

- Healthcare Services

- /

- NasdaqGS:OPCH

We Think The Compensation For Option Care Health, Inc.'s (NASDAQ:OPCH) CEO Looks About Right

Key Insights

- Option Care Health's Annual General Meeting to take place on 14th of May

- Total pay for CEO John Rademacher includes US$1.00m salary

- The overall pay is comparable to the industry average

- Option Care Health's EPS grew by 11% over the past three years while total shareholder return over the past three years was 26%

CEO John Rademacher has done a decent job of delivering relatively good performance at Option Care Health, Inc. (NASDAQ:OPCH) recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 14th of May. Here is our take on why we think the CEO compensation looks appropriate.

Check out our latest analysis for Option Care Health

How Does Total Compensation For John Rademacher Compare With Other Companies In The Industry?

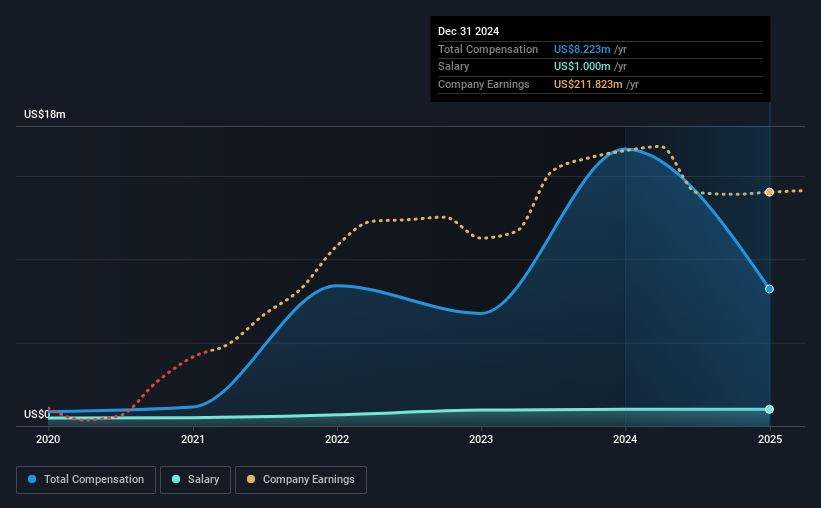

According to our data, Option Care Health, Inc. has a market capitalization of US$5.4b, and paid its CEO total annual compensation worth US$8.2m over the year to December 2024. Notably, that's a decrease of 51% over the year before. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$1.0m.

On comparing similar companies from the American Healthcare industry with market caps ranging from US$4.0b to US$12b, we found that the median CEO total compensation was US$11m. So it looks like Option Care Health compensates John Rademacher in line with the median for the industry. What's more, John Rademacher holds US$11m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | US$1.0m | US$1.0m | 12% |

| Other | US$7.2m | US$16m | 88% |

| Total Compensation | US$8.2m | US$17m | 100% |

On an industry level, around 15% of total compensation represents salary and 85% is other remuneration. It's interesting to note that Option Care Health allocates a smaller portion of compensation to salary in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Option Care Health, Inc.'s Growth

Option Care Health, Inc.'s earnings per share (EPS) grew 11% per year over the last three years. In the last year, its revenue is up 17%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Option Care Health, Inc. Been A Good Investment?

Option Care Health, Inc. has generated a total shareholder return of 26% over three years, so most shareholders would be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

In Summary...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We did our research and spotted 3 warning signs for Option Care Health that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:OPCH

Option Care Health

Offers home and alternate site infusion services in the United States.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor